Update on tax legislation: Key takeaways from proposed legislation

May 12, 2025

This is an evolving situation. Find our latest analysis of the bill here.

Today, the House Committee on Ways and Means — which holds jurisdiction over tax policy — introduced legislation that significantly amends the Inflation Reduction Act’s (IRA) clean energy and manufacturing tax credits. The draft legislation repeals credits related to electric vehicles (EVs), home efficiency, and hydrogen beginning January 1, 2026. The proposal also makes adjustments to the duration and transferability of other credits. This is the starting point and we anticipate that the final bill will take a more favorable stance on transferability and tax credits.

In light of this development, we wanted to provide an update and share a few observations on the process.

This is the first of many steps. While the Committee’s proposal makes significant changes to the duration and scope of the credits — including repealing transferability on projects initiated after two years from the enactment date or, in some cases, for credits produced after December 31, 2027 — we remain months away from a resolution to the tax bill process. Each subsequent stage of the bill-writing process is likely to serve as a moderating force for the credits, particularly the Senate, which has historically taken a more favorable view of these incentives on a bipartisan basis.

No retroactive change in law. The Committee bill — which serves as the House Republicans’ opening salvo in a process that will ultimately moderate changes to the credits, per above — sunsets the credits on an accelerated timeline but does not impact them retroactively or for the next 2.5 years, providing confidence for transacting 2025, 2026, and 2027 credits in the near term. Roughly $5B of bids have been placed on Crux since the beginning of the quarter, suggesting ongoing market confidence even in precedence of this text.

Congressional Republicans support the credits. Twenty-one House Republicans — none of whom are members of the tax-writing committee — and four Senate Republicans recently voiced their opposition to drastic changes to the IRA, citing the legislation’s economic benefits to their districts and its impact on keeping electricity prices affordable. (The letters also specifically cite “transferability” and the “direct passthrough benefits” of the credits.) Given their narrow margins, both Speaker of the House Mike Johnson and Senate Majority Leader John Thune will need these blocs’ votes to pass legislation on the House and Senate floors, respectively.

Stakeholder support for the credits — and transferability — is broad and diverse. Transferability disproportionately benefits newly eligible technologies that enjoy strong bases of Republican support, including advanced manufacturing, critical minerals, and nuclear power. There is significant industry support for transferability and the broader credits, and we anticipate increased advocacy throughout the remainder of the process.

The Senate will likely take up its version of the tax bill later this summer, with the August “X date” deadline to raise the debt limit serving as the key deadline for action. Consider that, since its inception in 1992, Congress has extended the wind production tax credit (PTC) 12 times, including under the Trump administration and a Republican Senate in 2019. The solar investment tax credit — originally enacted in 2005 — has similarly been extended five times.

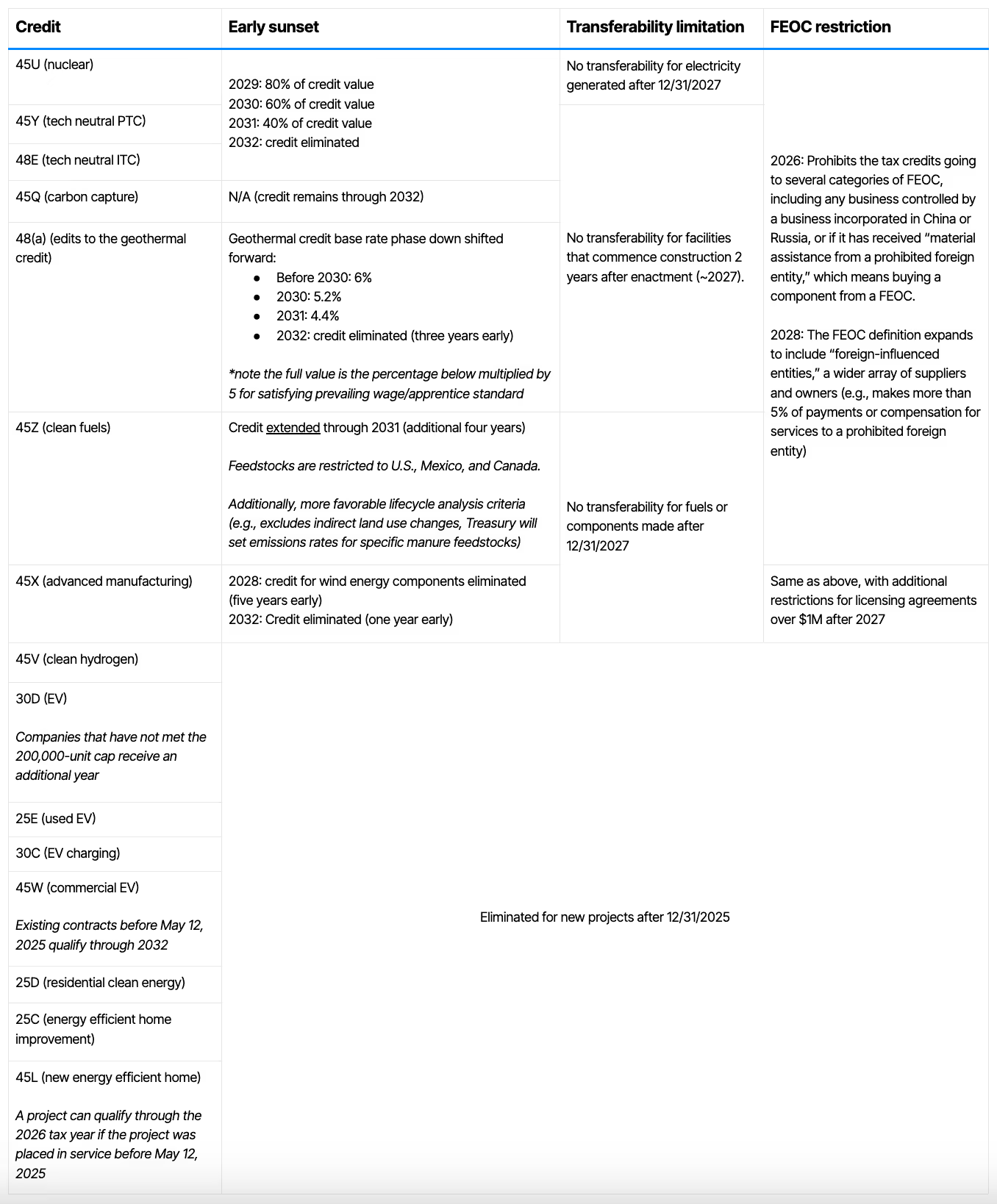

Below, find a summary of the key proposed changes to energy and manufacturing credits.

Proposed changes to specific energy and manufacturing credits

Credit: Pioneer Public Affairs

New Foreign Entity of Concern (FEOC) limitation

The proposal significantly expands the existing statutory definition of FEOC, including new definitions of a "prohibited foreign entity," a "specified foreign entity," and a "foreign-influenced entity." The FEOC requirements are more extensive than many had anticipated and will likely be a focus of the industry in the coming months.

Starting in January 2027, credits may be disallowed if the taxpayer is a specified foreign entity or if a certain percentage (generally more than 5–15% in aggregate) of payments related to the credited activity (e.g., production of electricity, storage, carbon sequestration, production of eligible components) go to a prohibited foreign entity.

Some credits also restrict property where construction includes material assistance from a prohibited foreign entity, including §48E energy storage construction and production beginning one year after enactment as well as §45X-eligible components in taxable years beginning two years after enactment.

What’s at stake

Transferability keeps electricity affordable and projects on track. Transferability ensures affordable electricity for American families and provides certainty for developers, enabling projects in nuclear, manufacturing, biofuels, and critical minerals to move forward. Repealing it would undermine existing investments and stall momentum across the energy and manufacturing sectors.

Transferability is a national security asset in the race against China. Transferability is vital to supporting the "America First" agenda, building a domestic supply chain, and ensuring we stay competitive with China. It also underpins the affordable electricity and critical mineral production needed to win the artificial intelligence (AI) arms race.

Transferability empowers small businesses and broadens market access. By enabling simple, peer-to-peer tax credit transactions, transferability allows small and mid-sized companies — traditionally excluded from complex tax equity markets — to compete, innovate, and grow alongside large incumbents.

Transferability is driving job growth and a manufacturing resurgence. Transferability has helped trigger a 3x increase in US manufacturing and mineral project development over the past year. Eliminating it could put an estimated 250,000 American manufacturing jobs at risk and derail onshoring momentum.

Transferability is a proven tool for resilience in uncertain markets. A bipartisan innovation, transferability helps insulate energy financing from economic downturns — unlike the fragile tax equity markets exposed during the 2008–2009 crisis. It enables stable, private-sector investment during volatility, supporting long-term industrial strength.

Stay tuned for more

We will continue to keep our partners informed throughout the remainder of the process, including through regular client memos and webinars. If you are interested in gaining access, get in touch to join the Crux platform.