On March 26, the Environmental Protection Agency (EPA) released its final rule establishing renewable volume obligations (RVOs) under the renewable fuel standard (RFS) for 2026 and 2027, finalizing higher volumes than proposed in June 2025 despite rising consumer fuel prices stemming from the Iran war. The RFS program creates a critical source of demand for clean fuel producers by requiring refiners to either blend physical volumes of biofuel or purchase associated credits, called renewable identification numbers (RINs), based on a percentage of their gasoline and diesel throughput.

Crux views the EPA’s decision to increase the volumes as further evidence of the strong support for the clean fuel sector by the current administration and Republicans broadly, which should bode well for outstanding items such as final rules from the US Department of the Treasury on the §45Z production tax credit, upcoming updates to carbon intensity models and on-farm conservation rules for feedstocks, and E15 negotiations in Congress. This favorable RFS decision came shortly after the EPA waived summertime limits on E15 sales. Together, these actions signal that the administration views supportive biofuel policies as a solution to fuel price inflation, not a driver.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

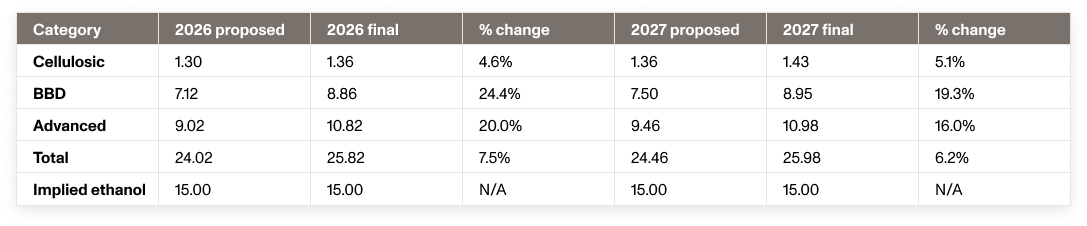

Compared to the proposed volumes, for 2026 and 2027, the final rule increased the cellulosic mandate (which includes renewable natural gas) by 4.6% and 5.1%, respectively, the bio-based diesel (BBD) mandate by 24.4% and 19.3%, and the advanced fuel category by 20.0% and 16.0% and kept the conventional ethanol category flat at 15 billion gallons. When accounting for the reallocated SREs (discussed further below), the mandate increases even further — by roughly 1 billion RINs for both 2026 and 2027, across all categories besides cellulosic.

Changes from proposed to final volumes, 2026–2027

The EPA also reallocated 70% of volumes exempted via small refinery exemptions (SREs) from 2023–2025 into the 2026–2027 into both the RVOs and the percentage standards, increasing blending obligations above the proposed rule's low-end case. Percentage standards determine how much biofuel refiners must blend or procure based on their throughput — calculated with the volumetric RVO quotas divided by projected gasoline and diesel consumption — meaning actual RIN demand fluctuates with overall fuel consumption.

In the June 2025 proposal, the EPA set a low-end standard assuming zero future SREs and a high-end standard assuming 18 billion gallons of exempted capacity. The September 2025 supplemental proposal updated both cases to account for 2.18 billion RINs worth of SREs projected for 2023–2025 and a revised consumption forecast for 2026–2027. Notably, rather than removing exempted gallons from the denominator, EPA updated the percentage standard calculation for 2026-2027 to add exempted gallons to the numerator.

The 70% reallocation is a meaningful win for clean fuel producers and a continuation of the policy originally established by the EPA in 2019 under Administrator Andrew Wheeler. Going forward, Crux expects the EPA to fold projected SREs directly into percentage standards — as it attempted to do in the June 2025 proposal — absent litigation or other policy developments requiring ad hoc adjustments.

Changes in 2026 percentage standards in final rule compared to proposed and supplemental rules

Changes in 2027 percentage standards in final rule compared to proposed and supplemental rules

On-demand webinar: Crux's experts break down financing for clean fuels projects in 2026 —>

Renewable diesel producers are the primary beneficiaries of the final volumes relative to the proposal. The final volumes exceed the ask from industry — the Clean Fuels Alliance requested at least 5.25 billion gallon mandate for BBD in 2026, which equates to 8.4 billion RINs on a 1.6 ethanol-gallon equivalency basis. Beyond the growth in the BBD mandate, RD gallons will be necessary to close the ~600 million gallon delta in the 15.0 billion-gallon D6 mandate and projected ~14.4 billion gallons of ethanol consumption in 2026 and 2027.

While the EPA took a more cautious approach to cellulosic fuel production growth — assuming a 9% annual growth rate from 2025–2027 compared to the 30% annual growth rate assumption in the 2023–2025 volumes — the final volumes are broadly supportive for the RNG industry. While the final volumes fall short of the ask from industry, which sought 1.50 billion gallons for 2026 and 1.86 billion gallons for 2027, the EPA took a more conservative approach given the need to waive the cellulosic mandate retroactively for 2025.

The final 2026–2027 RVO retains the 15 billion-gallon conventional fuel mandate for both years, holding implied demand for corn ethanol steady. The EPA projects ethanol consumption at approximately ~14.4 billion gallons, so the ~600 million-gallon delta in 2026 and 2027 must be closed by other D6-qualifying fuels such as renewable diesel or incremental ethanol blending. This creates an incentive for continued E15 adoption.

As discussed, the EPA proposed reallocating volumes lost to SREs back into the percentage standards, meaning blending obligations increase to offset gallons exempted from participating refineries. The proposal established a framework for projecting future SRE volumes into the standards prospectively rather than addressing shortfalls retroactively, providing more durable demand signals for producers across all fuel categories. In the final rule, the EPA reallocated 70% of the SREs granted for 2023–2025 into the 2026-2027 percentage standards. We expect a favorable approach to SREs to continue during the remainder of the Trump administration.

Beginning in 2026, the EPA proposed that imported renewable fuel and domestically produced fuel using foreign feedstocks generate only half the RINs of equivalent domestic production — a direct effort to redirect demand toward domestic supply chains. For renewable diesel and SAF producers, this effectively penalizes used cooking oil and tallow imported from abroad and creates a structural advantage for producers sourcing domestic soybean oil, animal fats, and corn ethanol feedstocks. In the final rule, the EPA dropped this provision but noted it would enter effect for 2028, a strong signal for future direction. That said, instituting this policy would require a new rulemaking process as part of the future RVO.

The EPA proposed removing renewable electricity entirely as a qualifying fuel under the RFS, concluding that electricity does not meet the statutory definition of renewable fuel under the Clean Air Act. eRINs were drafted in 2022 as a pathway for electricity generated from biogas to earn RFS credits but had never been implemented — meaning the removal eliminates a theoretical future pathway rather than disrupting any existing market, with no near-term impact on RNG, renewable diesel, SAF, or ethanol producers. In the final rule, the EPA retained the elimination of eRINs.

The EPA proposed standardizing renewable diesel and renewable jet fuel equivalence values at 1.6 RINs per gallon and renewable naphtha at 1.4, fixing values at the lower end of the existing facility-by-facility ranges to account for the fossil-derived hydrogen used in hydrotreating. The EPA also brought SAF to parity with RD at 1.6 RINs per gallon. This narrows the RIN-generation advantage that renewable diesel has historically held over biodiesel and ethanol, modestly improving the competitive economics of corn-based fuels relative to HEFA-derived products. In the final rule, EPA established lower equivalency values for RD and SAF at 1.5 while maintaining the 1.4 multiplier for naphtha and delayed the change until January 1, 2027.

In the proposal, the EPA solicited comments on establishing a general pathway for renewable jet fuel produced from corn ethanol, which would open a new SAF demand channel for ethanol producers and could significantly expand the addressable market for domestic ethanol. In the final rule, EPA did not finalize a new standard pathway for ethanol-to-jet despite pressure from the ethanol industry.

With the RFS volumes for 2026–2027 now finalized, attention should turn to four key outstanding policy developments expected later this year:

Given the administration's demonstrated commitment to domestic biofuel production, we expect each to be broadly favorable for producers. Taken together, progress on these items would meaningfully tighten the range of outcomes investors must underwrite — improving liquidity and pricing in the clean fuel tax credit transfer market and accelerating capital formation across the clean fuels sector.

The GREET model, which serves as the carbon intensity baseline for §45Z calculations, will be updated to include changes mandated by the One Big Beautiful Bill (OBBB). This includes removing the impact of indirect land use change for crop-based fuel emission rates and differentiating the carbon intensity of manure-based feedstocks for RNG.

Today's RFS decision suggests the administration will approach the GREET update with the same pro-domestic-feedstock orientation.

The USDA's feedstock guidance remains a critical missing piece for crop-based fuel producers and farmers seeking to benefit from on-farm conservation practices such as cover crops, reduced tillage, and advanced fertilizer under §45Z. Finalization will determine which conservation practices generate verifiable carbon-intensity reductions and how much additional tax credit value flows to the agricultural supply chain. We expect the USDA to move quickly and take a pro-industry approach on issues such as book-and-claim accounting for feedstock attributes given Secretary Brooke L. Rollins' prominent role in today's RVO announcement and the administration's emphasis on farm income support.

Treasury issued a proposed rule in February 2026 governing the §45Z credit, which had operated under interim guidance since January 2025. The proposal addressed key outstanding questions around the treatment of intermediary sales, providing safe harbors for determining the emissions rate for a fuel and substantiating that a qualified sale has occurred. We expect the final rule to track closely with these provisions.

Congress is considering legislation that would permanently authorize year-round E15 sales nationwide, removing the summertime blend wall that has historically constrained ethanol demand. While the EPA's recent waiver provides near-term relief, a statutory fix would offer more durable market access for ethanol producers. The legislative push received a significant boost on March 27, when President Donald Trump directly urged Congress to pass permanent E15 authorization at the White House Great American Agriculture Celebration — the same event at which today's RVO finalization was announced.

Crux will continue to follow all of these updates. To learn more about the regulatory and policy intelligence we provide our clients and partners, including through policy memos, briefings, and custom research, get in touch with us.