Shortly after the passage of the One Big Beautiful Bill (OBBB), the White House issued Executive Order 14315, which directed the US Departments of the Treasury and Interior to issue new rules strictly enforcing the termination of the solar and wind credits. Pursuant to the executive order, on August 15, Treasury issued guidance further clarifying what it means to “begin construction.”

Here’s what the updates entail and how they impact developers looking to safe harbor their clean energy projects.

Connect with the Crux team to learn about safe harbor strategies.

Safe harboring is the process of establishing that a project has begun construction such that it secures eligibility for a specific year’s tax credit value under the §48E investment tax credit (ITC) or §45Y production tax credit (PTC) as long as the project is placed in service within four years (exclusive of specific events outside of the developer’s control — more below). Safe harboring allows developers to:

The Internal Revenue Service (IRS) has historically recognized two primary methods for establishing that construction has begun on a qualified energy project:

These methods are intended to determine the applicable credit rate and compliance period under §45Y and §48E. The IRS has provided guidance on these methods in Notice 2013-29 and Notice 2018-59, along with other notices that clarify, modify, and update these notices.

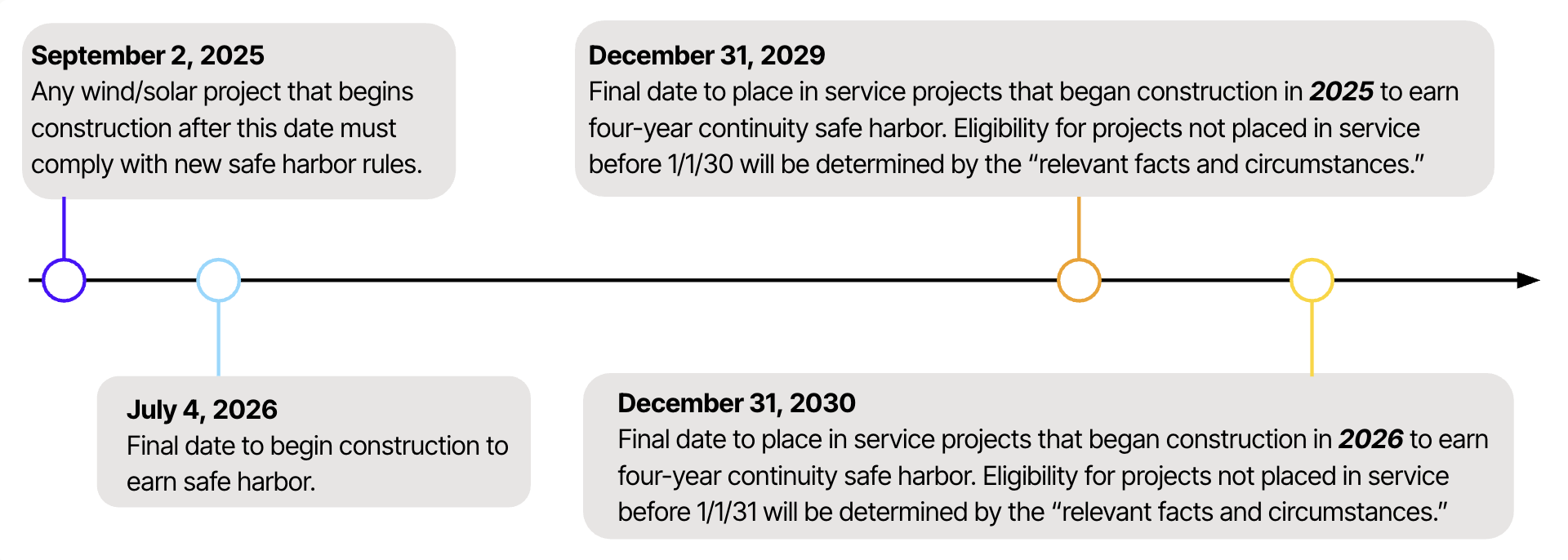

Under the OBBB, wind or solar projects that begin construction by July 4, 2026 are conferred a safe harbor to earn the full technology-neutral credits under §45Y and §48E, provided they meet begun-construction requirements (more below).

If solar and wind projects do not begin construction by July 4, 2026, they must be placed in service by December 31, 2027 to be eligible for the credit.

Projects that begin construction after December 31, 2025 will not be eligible for tax credits if they do not comply with the revised Foreign Entity of Concern rules, for which implementing guidance is forthcoming (as of August 27, 2025).

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

On August 15, the Treasury Department released comprehensive guidance (Notice 2025-42) regarding the beginning of construction of wind and solar projects for the purposes of tax credit eligibility. The new rules go into effect on September 2, 2025 and apply only to projects that begin construction on or after that date.

The guidance eliminates the 5% safe harbor test for solar facilities larger than 1.5 MWac and all wind facilities. Solar facilities that are 1.5 MW and smaller may still use the 5% safe harbor test to qualify for tax credits.

New wind/solar safe harbor timeline

To utilize the begin-construction safe harbor, developers need to understand how to establish the beginning-of-construction status for projects under §45Y, §48E, and related provisions of the Internal Revenue Code (IRC).

Under the physical work test, construction is considered as having begun when “physical work of a significant nature” starts. Such work may be performed by a third party under a binding written contract and can include either:

Preliminary activities including planning, securing financing, routine site clearing, and grading do not qualify under the physical work test.

Under new guidance, the physical work test is now the sole method to establish that construction has begun for solar projects larger than 1.5 MW and all wind projects.

Under this method, construction is considered to have begun once the taxpayer incurs at least 5% of total eligible project costs. Qualified costs can include tangible personal property integral to the project, such as:

As a general rule, costs are deemed incurred with respect to property upon delivery. However, if payment is made prior to delivery, the costs may be deemed incurred at the time of payment, provided the property is reasonably expected to be delivered within 3.5 months of the payment date.

Only solar projects that are 1.5 MW and smaller can qualify for safe harbor under the 5% test.

Once construction begins, the developer must demonstrate that work has continued without significant interruption. The IRS evaluates continuity based on facts and circumstances, although projects are deemed to meet the requirement if they are placed in service by the end of the fourth calendar year after the calendar year in which construction began.

New guidance from the Treasury Department retains this four-year “continuity safe harbor.” Excusable disruptions, such as delays in permits and interconnection, natural disasters, supply shortages, and financing, will not disqualify a project from meeting the continuous construction requirement.

Developers must maintain their safe harbor qualification through contemporaneous records, including:

Yes. Establishing safe harbor locks in the credit eligibility. The credit itself can still be sold or transferred under the 6418 transferability rules, assuming all other requirements are met.

Crux works with clean energy developers every day to unlock financing opportunities, especially in the critical early stages of a project when safe harboring strategies are most valuable. Here’s how we can support you:

Our extensive lender network includes capital providers who understand safe harbor rules and are ready to finance 5% test or physical work expenses. Our debt platform allows developers to find the right financing partner for their project timeline and tax credit strategy, and our expert team and platform guide both parties through the transaction.

Crux’s network of original equipment manufacturer (OEM) partners helps developers source equipment procurement opportunities, which can be used as part of safe harbor strategy. Our OEM partners are accustomed to participating in safe harbor transactions and can cooperate with developers related to documentation requirements and other compliance strategies.

Crux’s expert team and authoritative market intelligence guide developers through complex transactions. We also connect you with leading law firms that specialize in IRS-compliant safe harbor strategies, including advice related to documentation, binding contracts, and audit defensibility. Crux helps developers prepare for future credit transfers or sales by aligning safe harbor strategy with long-term financing goals.

To discuss safe harbor strategies for your projects, get in touch with us.

This post is for informational purposes only and should not be construed as tax, legal, or accounting advice. Crux does not provide tax or legal advice. You should consult with your own tax, legal, and accounting advisors before engaging in any transaction or strategy discussed herein, including safe harboring or any related financing or credit monetization activities.