Battery storage is an increasingly important part of the US power system. According to the US Energy Information Administration (EIA), 10.3 gigawatts of utility-scale battery energy storage systems (BESS) were installed in 2024. Nearly six gigawatts of utility-scale BESS were added in the first six months of 2025, and the EIA forecasts that more than 18 gigawatts will be built by the end of the year — about 80% more than 2024.

Utility-scale BESS also constitutes a growing share of the tax credit market. In the first half of 2025, standalone BESS and hybrid solar+storage systems accounted for about 26% of all tax credits sold. This was an increase of 11% over 2024.

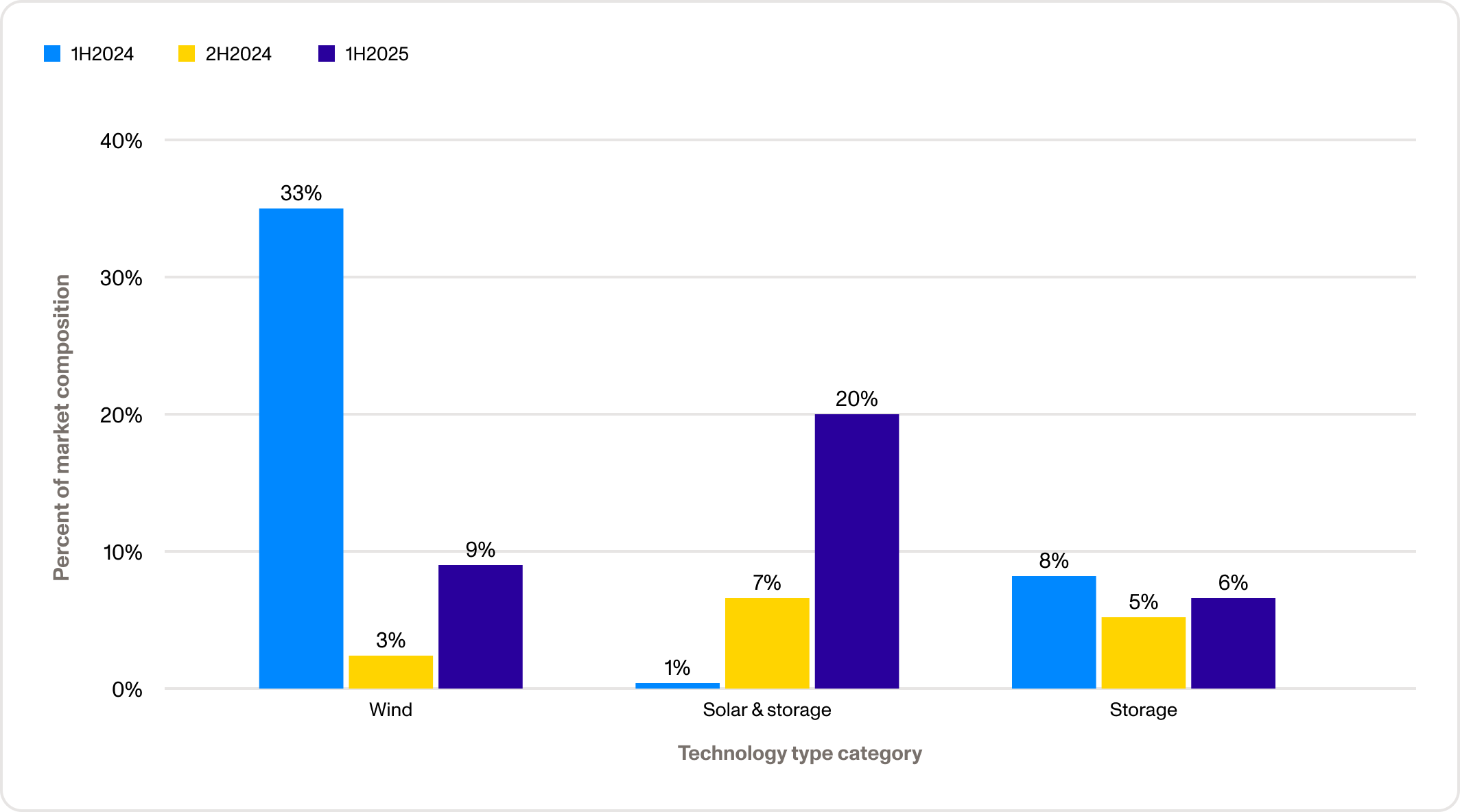

Market composition by technology type

Multiple drivers are contributing to the growth of BESS. Steadily declining costs over the past decade have made BESS economically competitive with other forms of generation. Storage is also needed more than ever before — to decrease curtailments of solar power, reduce interconnection constraints, and support intraday and seasonal variations in power supply and demand.

BESS is also supported by policy certainty. Under the One Big Beautiful Bill (OBBB), incentives for wind and solar are restricted to projects that commence construction by July 4, 2026 — one year after the bill was signed into law — or enter service by December 31, 2027. OBBB provisions provide BESS projects access to tax credits through 2034 before phasing them out in 2036.

According to our 2025 mid-year market intelligence report, investment tax credit (ITC) pricing for standalone and hybrid BESS ranged between $0.915 and $0.945 in the first half of 2025.

Larger transactions generally attracted higher prices. The credit rating of sellers was also a primary factor in pricing, though this was less true of BESS projects than for other ITC-eligible technologies. Our transaction dataset showed that investment-grade (IG) sellers received, on average, a $0.03 premium on transfer deals. In the first half of 2025, the average ITC from an IG-rated sponsor transacted at $0.94, with some reaching $0.96. This was as good or better than the pricing that was observed in 2024. For non-IG sellers, pricing averaged $0.91, moderately below 2024.

BESS project revenue models also impacted pricing. Partial contracts and merchant revenue models are common with BESS projects. In a merchant revenue model, a BESS owner earns revenue by selling power and grid services in wholesale electricity markets. Investors overwhelmingly prefer the revenue certainty of long-term contracts. The absence of long-term contracts is reflected in lower pricing for BESS projects.

Sellers often purchase insurance to address the uncertainty associated with merchant and partial-contract revenue models. Approximately 80% of BESS deals carried insurance in the first half of 2025, including about half of all storage deals with investment-grade sponsors.

2025 storage ITC (including hybrid) ITC pricing

%20ITC%20pricing.png)

According to our research, transferability provides BESS projects multiple routes to market. Standalone storage deal structures in the first half of 2025 were split nearly evenly between tax equity (49.5%) and direct transfer deals (46.5%). Another 3.8% of deals included preferred equity. By comparison, utility-scale solar deals were 72% tax equity, 16% direct transfer, and 12% preferred equity.

Solar-plus-storage deal structures were 64% tax equity, 28% direct transfer, and 8% preferred equity.

Seller structure for storage (inclusive of hybrid) ITC deals

%20ITC%20deals.png)

Multiple options for tax credit monetization — whether tax equity, direct transfers, or other investment structures — ensure that projects can optimize for the revenue model in the context of financing. That’s important for BESS, where contractedness looks different than for other power-generating projects.

Data from the EIA shows that an increasingly large share of BESS projects are deployed with arbitrage as the principle use case and frequency support as the second most common use case. Contracts for arbitrage may be attractive for projects but relatively unfamiliar to traditional tax equity investors.

Tax equity investors typically will not consider merchant uncontracted projects, preferring those with predictable cash flows. However, long-term, fixed-price contracts for energy arbitrage are hard to secure because energy prices are volatile, and revenues from ancillary services are not standardized across markets. Consequently, around one-third of standalone BESS projects are merchant. Partial contracts are also common, utilized in about 16% of standalone BESS projects and 43% of solar+storage projects. Lenders also tighten terms for loans to merchant projects, which can increase the overall cost of capital and extend the timeline of projects.

The high percentage of merchant projects helps explain why BESS projects rely more on direct transfers to monetize tax credits. This is significant because direct transfer deals forgo the basis step-up achievable with tax equity partnerships. The credit value is tied to cost basis rather than a fair market value basis. The absence of a basis step-up can reduce the total possible credit monetization by roughly 25% compared to a stepped-up structure. This impacts overall project returns and pricing power.

Hybrid solar+storage often enjoys greater access to tax equity than standalone BESS because contracted solar revenues provide long-term certainty more attractive to tax equity investors.

The accessibility of tax credits under the OBBB also matters. Because credits for solar ramp down sooner than those for standalone BESS, development could gradually shift toward standalone BESS projects. We could also see the timing of tax credit accessibility encourage more solar facilities to incorporate BESS to retain access to incentives for a portion of the shared infrastructure. Over the long term, we forecast that the durability of the standalone BESS tax credit will lead to a more balanced portfolio of hybrid and standalone projects.

Many of the factors driving BESS growth will remain impactful, even amid ongoing policy noise and lower corporate tax liabilities. Curtailment relief, peak management, and the need for system flexibility remain powerful factors propelling BESS deployments. Between 2027 and 2030, the share of BESS credit monetization and new builds could expand even more as solar incentives phase down.

The key questions impacting storage deployments include how financing structures will evolve to support continued project development, as well as regulatory considerations that uniquely affect BESS projects. For example, supply chain policies — including Foreign Entity of Concern (FEOC) provisions and material assistance rules — will shape eligible equipment pathways and deal timelines for BESS projects.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

Market maturity could also impact pricing. As diligence, insurance, and documentation standardize, pricing could improve and spreads could narrow. This is particularly likely for IG sponsors and large sellers.

The first half of 2025 brought rapid change. Based on what we’re seeing in the market, BESS developers should consider the following:

Looking to make smarter transaction decisions? Crux clients have access to our full library of reports, based on our industry-leading dataset of $40 billion in transactions, as well as market intelligence embedded directly in the Crux platform. Contact us to learn more about transacting on Crux.