Since the passage of the One Big Beautiful Bill (OBBB), the corporate tax landscape has undergone several structural changes that continue to shape the transferable tax credit market.

Analysis by the Joint Committee on Taxation (JCT) prior to passage projected that the OBBB would reduce corporate tax payments by roughly $100 billion in 2025. Crux’s internal analysis suggests that corporate tax liabilities will be 20–30% lower in 2025. Other estimates place the figure higher, such as a Zion Research Group report that projects $148 billion in aggregate tax savings for the S&P 500 alone.

This decline in tax liability is already influencing market sentiment. In Crux’s mid-year market intelligence survey, 73% of buyers said they expect their 2025 tax liability to be influenced by the OBBB, and 60% indicated this would affect the volume of credits they intend to purchase this year.

Influence of policy on tax liabilities and tax credit purchases

The shift in tax exposure has led to a measurable cooling of tax credit market activity. In Q3, many large corporate buyers paused new 2025 purchases to reassess their tax capacity given the changes. The result was a broad slowdown, particularly in demand for 2025-vintage credits. Some smaller and newer buyers continued to participate, but this meant reduced depth of demand and competition overall.

On the supply side, some sellers of 2025 credits faced timing pressure tied to project financing contingencies where tax credit sales are needed to unlock other sources of capital, amplifying the impact of delayed buyer activity for these sellers.

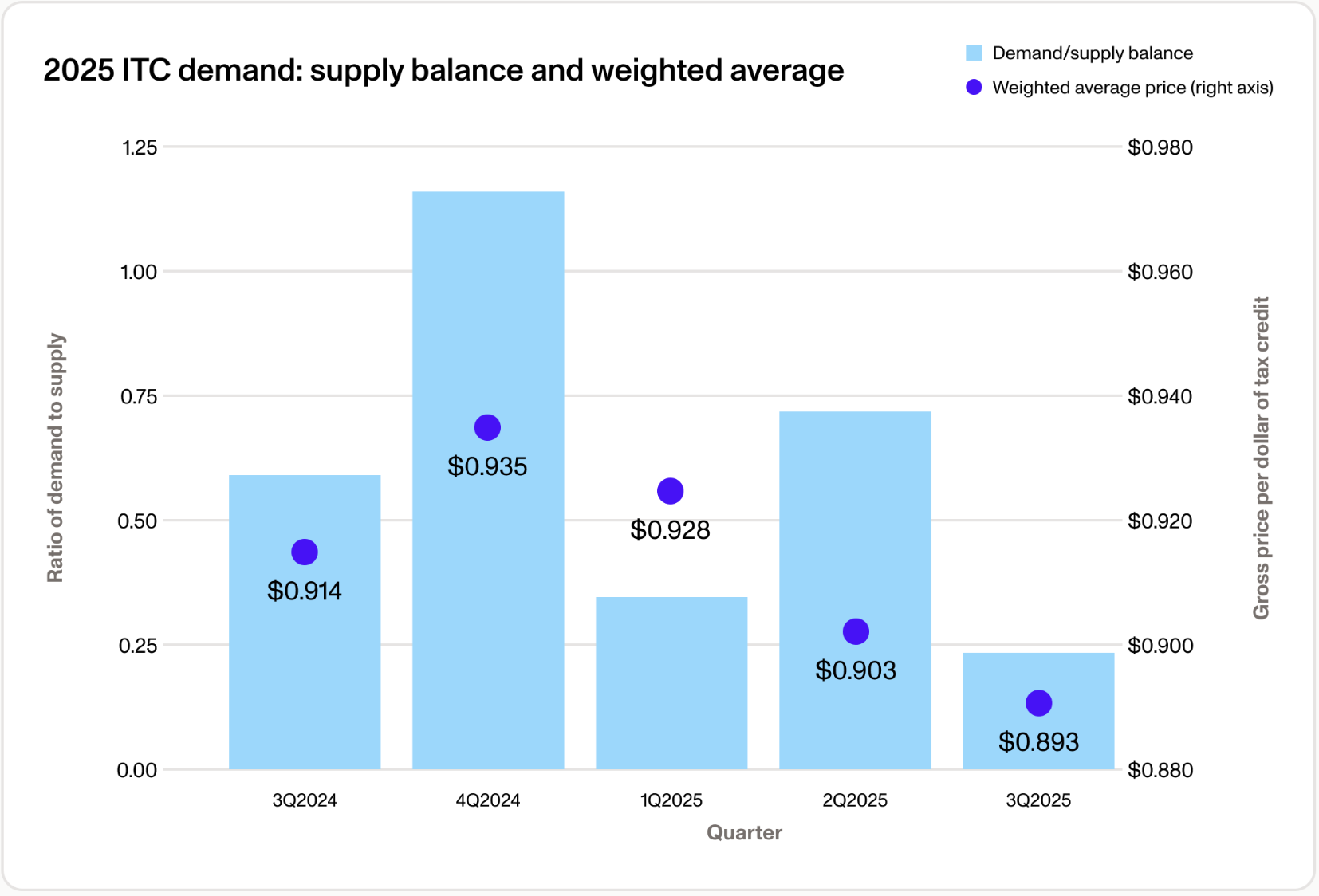

Weaker buyer activity led to less competition for available tax credits, which depressed 2025 pricing in Q3. Prices for 2025 investment tax credits (ITCs) fell 1.1%, landing at $0.893 in the third quarter, down $0.035 from the first quarter of the year. Buyer demand weakened significantly due to sluggish market activity. Crux estimates roughly $0.25 of demand per $1.00 of available supply, the lowest ratio in more than a year.

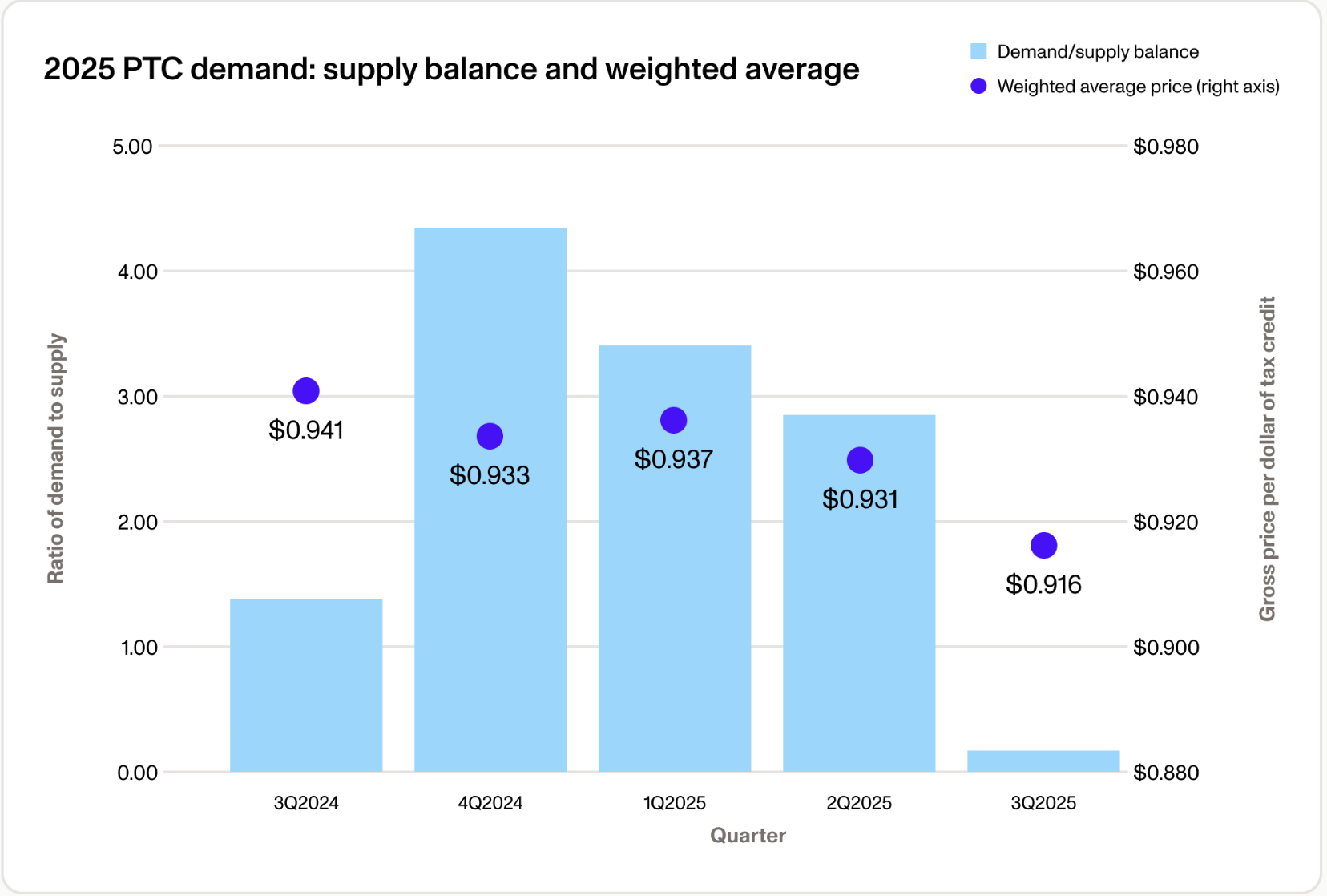

The production tax credit (PTC) market saw increased volume in the third quarter of the year, with more §45X and §45Z spot PTCs entering circulation. However, demand softened at the same time as large corporate buyers reassessed tax exposure.

Prices declined 1.6% in Q3, from $0.931 to $0.916. PTCs continued to price slightly above ITCs, which is a reflection of their predictable generation profiles, lower perceived risk, greater buyer familiarity, and standardized deal structures.

While spot activity softened, forward PTC transactions provided a bright spot in Q3, averaging $0.930 — up from $0.926 in Q2 and almost $0.020 above spot PTCs. Some buyers shifted their focus toward high-quality, long-term PTC strips, showing a flight to quality amid a quieter near-term market.

Forward ITC demand, by contrast, has not yet meaningfully materialized, though pricing has remained relatively stable quarter over quarter. Encouragingly, early Q4 data suggests renewed buyer engagement — bid activity in October already trended higher than Q3.

In light of the pricing shifts in the third quarter, Crux adjusted the Cruxtimate, our proprietary benchmark for indicative market pricing. The adjustment reflects an effort to realign expectations between buyers and sellers. As liquidity tightened and fewer competitive bids entered the market, maintaining a realistic pricing range that reflects current transaction levels and balancing competitive pricing with the need to keep bid activity healthy became critical to sustaining participation.

This ensures that the Cruxtimate remains an effective signal for market participants, anchoring expectations in a period of short-term uncertainty.

So far, fourth-quarter buyer interest has shown a modest uptick from its very depressed levels in Q3. That said, it is still significantly lower relative to 4Q2024 — interest in ITCs is about 20% what it was in the fourth quarter last year. Crux has seen prices holding steady at historically low levels for both ITCs and PTCs. Market participants should expect payment to be delayed to 2026.

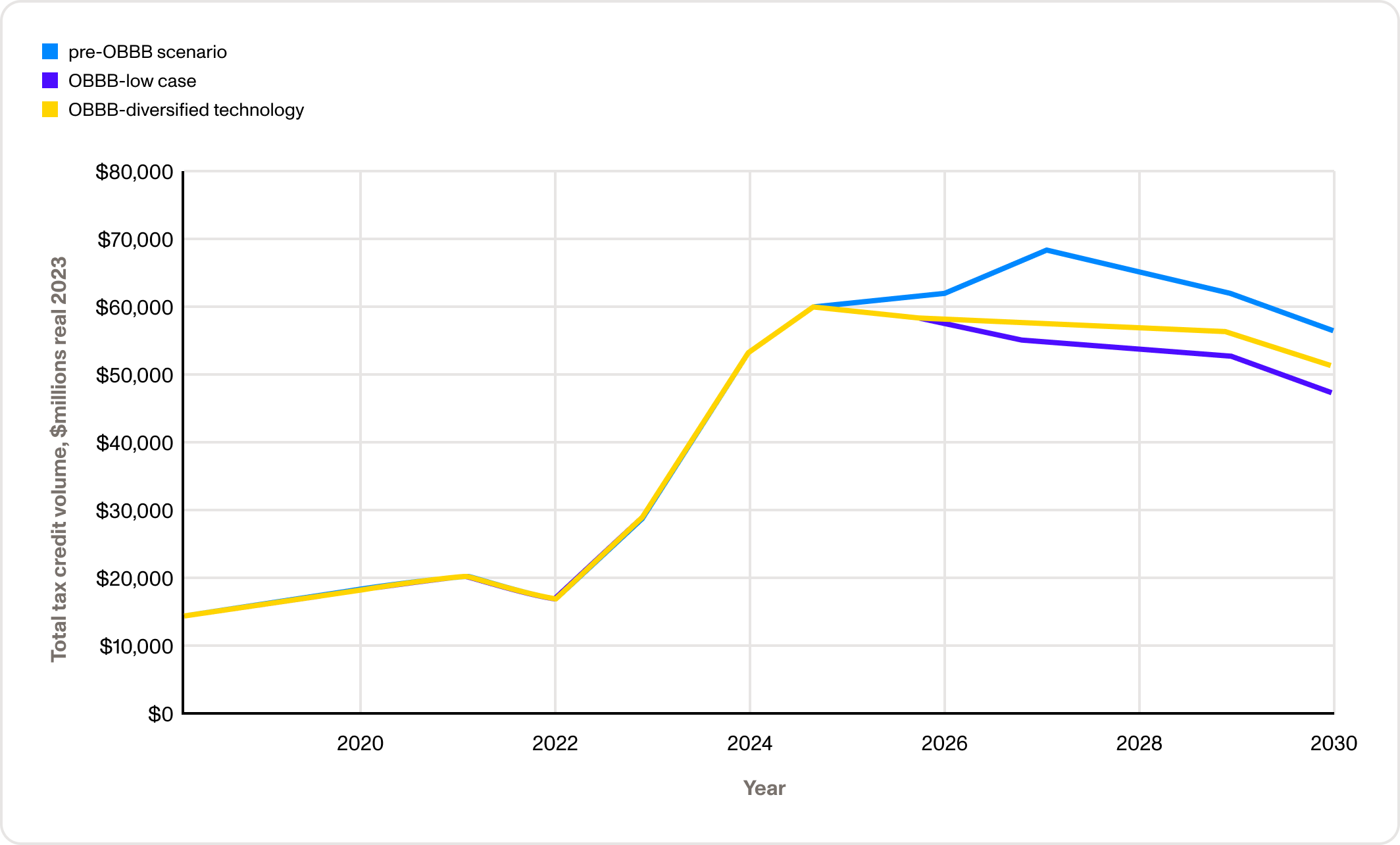

Looking further ahead, the overall size of the transferable tax credit market is expected to moderate slightly relative to pre-OBBB projections, but remain well above pre-IRA levels. Crux modeled three potential market paths through 2030 — a pre-OBBB baseline, a low-tax-credit case, and diversified technologies case.

Outlook for total tax credit generation, multiple scenarios

Even with reduced tax liabilities and the most conservative assumptions, the market is expected to generate more $50 billion in annual credits through the second half of the decade, settling around $45 billion by 2030. Under the diversified technologies scenario, new project deployment, particularly in battery energy storage and advanced manufacturing, supports sustained generation around $55 billion annually before tapering later in the decade.

While a few major buyers may sit out the rest of 2025 as they clarify their tax liabilities, an influx of new buyers is expected. These buyers may have different needs — smaller credit tranches, for instance, or different technology types. In that kind of environment, liquidity is key to ensure that buyers can find the tax credits that best fit their needs.

Given depressed demand and pricing, Crux estimates that supply-to-demand ratios for tax credits are at their lowest in more than a year. For tax credit buyers, that could mean the opportunity to take advantage of deep pricing discounts. With relatively low competition in the current market, buyers can also ensure that they get the tax credits — both size and type — that they want to satisfy their tax liabilities.

Crux provides a large, liquid tax credit marketplace, giving corporate tax teams and their advisors access to the largest network of high-quality, well-vetted tax credits at competitive prices. Our expert team provides full transaction support, from sourcing tax credits through execution.

Get in touch to learn more about how Crux can support your tax credit transactions.