Since 2023, transferability has enabled clean energy developers and manufacturers to sell their tax credits to third parties for cash, jumpstarting a wave of investment in clean energy infrastructure. Corporate taxpayers, in particular, have benefitted from transferability by purchasing tax credits at a discount to satisfy a portion of their tax liability. The One Big Beautiful Bill (OBBB), signed into law on July 4, 2025, preserved transferability but made many other changes that could affect corporate tax liability. Since then, the question for many market participants has been: how will that impact demand for transferable tax credits?

To answer that question, Crux engaged experts at major accounting firms, including EY and KPMG, as well as survey responses from our 2025 mid-year market intelligence report.

Key takeaways: Changes to cash flow and tax liability are reshaping demand patterns for transferable tax credits in the near term. Crux expects demand to slow in Q3 2025 but start to recover toward the end of the year.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

A number of tax credit buyers were awaiting final legislation before entering the market in 2025, anticipating adjustments to their federal tax liability. The final bill did make several changes that impact corporates:

The base erosion and anti-abuse tax (BEAT) adds an extra layer that magnifies the reduction in tax credit appetite for large multinationals. Companies subject to the BEAT may see more deductions that push their regular tax liability down closer to the BEAT floor, shrinking the “cushion” available for tax credit purchases. Because only 20% of general business credits reduce BEAT liability, additional credits can actually accelerate hitting the BEAT, further limiting tax capacity.

These changes are expected to boost short-term cash flow and simplify capital investment planning, leading to an overall decrease in federal tax liability.

Many corporate taxpayers are still digesting the changes and determining the impact on their tax liabilities. Running tax scenarios is a complicated process that takes time, and most buyers are running multiple scenarios. EY estimates that most Fortune 500 companies will probably have a clearer view by the end of Q4 2025.

Analysis by the Joint Committee on Taxation (JCT) prior to the OBBB’s passage indicates that it would reduce corporate tax payments by $100 billion in 2025, including:

Crux’s analysis of the OBBB’s impact suggests that corporate tax liabilities will be 20–30% lower in 2025. Third-party analysis suggests the impact could be greater. A recent report by Zion Research Group projected an aggregate savings of $148 billion for the S&P 500 alone.

Some changes are already visible. Buyers in Crux’s mid-year survey acknowledged that their tax capacity has been impacted heavily by policy changes; 73% say that policy has influenced their 2025 tax liabilities, and 60% say that it has influenced the amount of tax credits they intend to purchase.

Influence of policy and tax liabilities and tax credit purchases

Different industries will likely see different magnitudes of changes to federal tax liability. Very capital-intensive, R&E-heavy industries could see larger decreases, for instance. The JCT analysis suggests that R&E-heavy industries such as tech, pharma, biotech, and advanced manufacturing could see taxable income in 2025 drop by nearly 50% compared to the pre-OBBB baseline.

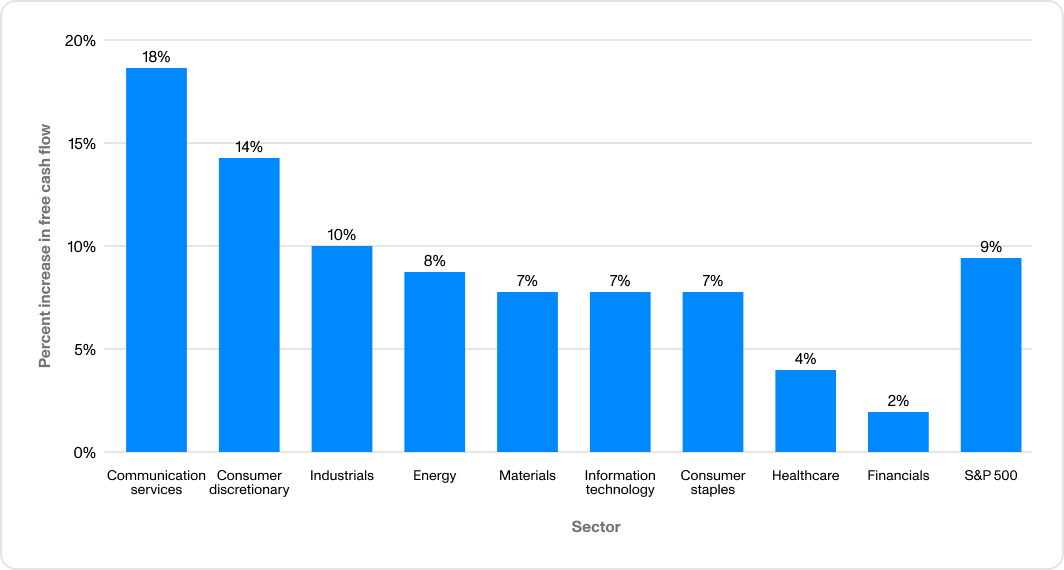

Zion Research Group estimated the impact to free cash flow by sector, finding that communications services — a sector that includes most major tech companies and telecom companies — and consumer discretionary firms are likely to see the biggest boost to free cash flow from a reduction in tax liabilities. Greater impact to free cash flow corresponds to a bigger reduction in tax capacity.

Projected increase in free cash flow from changes to tax liabilities, by sector

Liquidity is down as some bigger, mainstay buyers sit on the sidelines for 2025, which has an immediate impact on near-term demand.

Prices for tax credits are also down. Changes in demand can have an outsized effect on market pricing, at least in the short term. Tax credit sellers generally have already considered the monetization of their tax credits in their capital structure. But tax credit buyers are not required to purchase tax credits — they can alternatively pay their tax bill as planned. Buyers also typically time their tax credit purchases with quarterly or annual tax payments to maximize their value.

In the current environment, tax credit sellers may offer steeper discounts to attract buyers. Tax credit pricing remains below year-ago levels for several reasons:

Overall corporate tax liabilities will still substantially exceed the total volume of tax credits generated in 2025. While Crux expects demand for tax credits to be lower in Q3 2025, we anticipate that demand will likely begin recovering in Q4.

While demand is expected to recover, the composition of the buyside may differ materially from 2024. Bigger, mainstay tax credit buyers may sit on the sidelines for the remainder of the year, resulting in more buyers with less experience and/or less capacity.

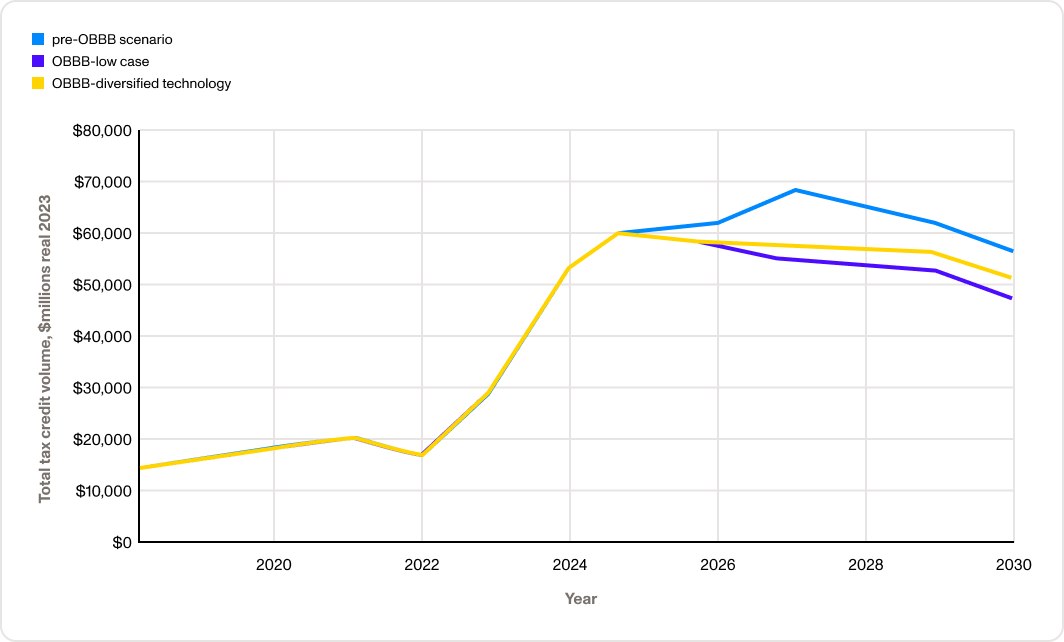

In the medium term, we anticipate a dynamic and resilient transferable tax credit market. We modeled three scenarios through the end of 2030: a pre-OBBB baseline, a low tax credit case, and a diversified technology case. Even in the low case, the market is projected to generate more than $50 billion in tax credits annually, declining to around $45 billion in 2030.

Under the diversified technologies case, new project deployment and more storage investment support sustained tax credit generation around $55 billion through much of the decade before settling around $500 billion in 2030.

Outlook for total tax credit generation, multiple scenarios

In 2024, total tax credit monetization was $52 billion. Crux projects that total tax credit monetization in 2025 will total $55–60 billion. Prior to the passage of the OBBB, 2025 corporate tax liabilities likely exceeded $530 billion. Even with reduced liabilities, that still leaves a large potential appetite for tax credits.

Even assuming a few major buyers sit out the rest of 2025 as they clarify their tax liabilities, an influx of new buyers is expected. These buyers may have different needs — smaller credit tranches, for instance, or different technology types. In that kind of environment, liquidity is key to ensure that buyers can find the tax credits that best fit their needs.

Crux provides a large, liquid tax credit marketplace, giving corporate tax teams and their advisors access to the largest network of top-tier developers and manufacturers. Buyers and their advisors use the Crux platform to source, diligence, and execute transactions, leveraging our deal standards, form documents, and market intelligence to make informed decisions efficiently.

Contact us to learn more and request a platform demo.