The US House-enacted reforms to the tax code — the One Big Beautiful Bill (OBBB) Act — includes an international tax policy provision that is getting attention from many quarters: new Section 899. Though nestled within the broader context of international tax policy and US corporate tax competitiveness, Section 899, if enacted, would have specific implications for energy project developers and financiers. In particular it could substantially increase taxes on payments made to and investments made by foreign-domiciled investors located in jurisdictions with taxes deemed to be “unfair” under the law.

The revised Section 899 is positioned as a remedy against what the US government deems "unfair foreign taxes." At a glance, the changes expand the scope of tax liabilities, redefine thresholds of applicability under BEAT (Base Erosion and Anti-Abuse Tax), and provide the Treasury with broad discretionary power to act against discriminatory tax practices abroad. Below, we break down what these changes entail, and what they could mean for investment in energy projects.

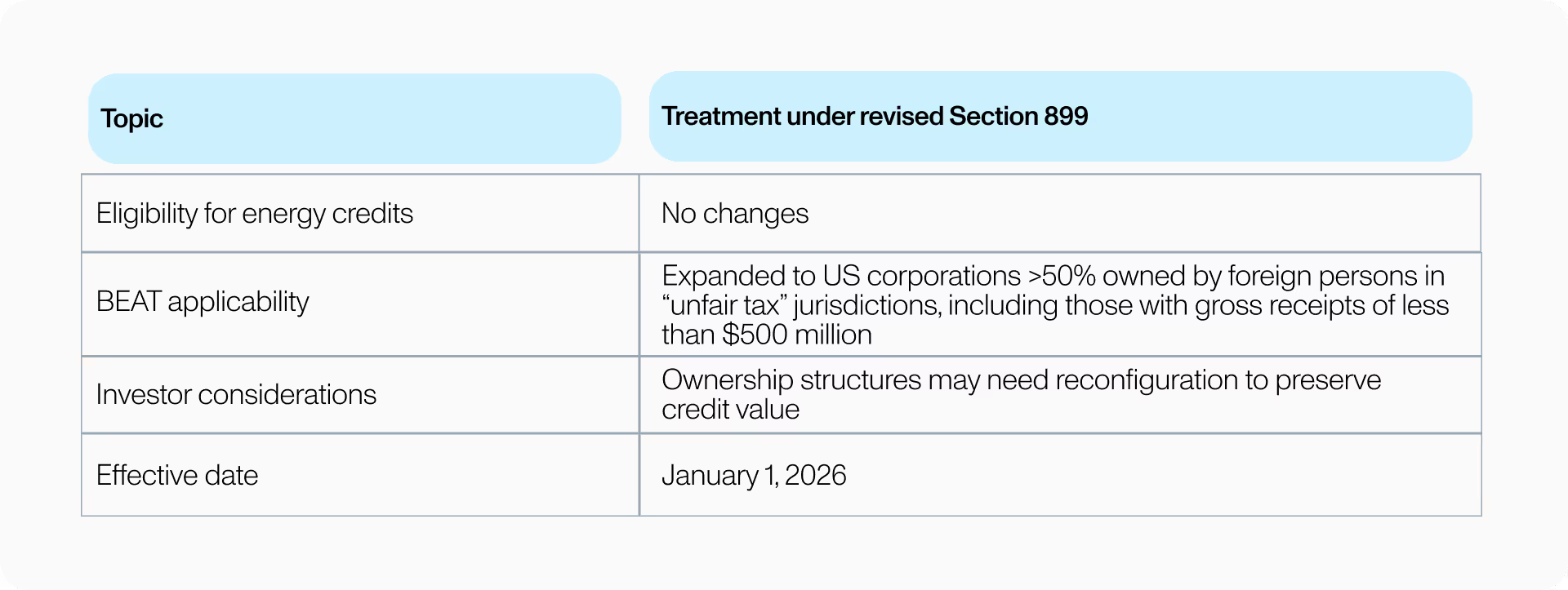

The proposed revisions to Section 899 under the OBBB Act do not explicitly eliminate or disallow energy tax credits (such as §45Q, §45X, or ITC/PTC) for taxpayers located in “unfair tax jurisdictions,” but they do create significant new hurdles that may diminish the practical benefit of those credits for US corporations with more than 50% foreign ownership from such jurisdictions.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

The provision would treat all countries that have implemented the enforcement rule of the Organisation for Co-operation and Economic Development’s (OECD) Pillar Two global minimum tax regime, digital services taxes, or diverted profits taxes, by making portfolio and direct investment in the US for investors from those jurisdictions onerous and expensive. In so doing, countries would face pressure to rescind the three taxes Section 899 specifies as being unfair, as well as any other taxes the administration deems unfair in the future under the authority granted to it by Section 899. In the House’s version of the bill, however, higher BEAT penalties kick in around January 1, 2026 — likely much too quickly for most countries to react and repeal the three specified “unfair” taxes.

Here’s how investments in projects relying on energy and manufacturing tax credits could be impacted under the new framework:

The revised Section 899 modifies BEAT rules to effectively ensure they apply to almost all US corporations that are more than 50% owned by foreign persons resident in countries with an "unfair foreign tax." These companies will be designated as “applicable taxpayers,” triggering a more stringent BEAT regime that includes:

If these enhanced BEAT rules are ultimately enacted, they could significantly reduce the appeal of energy tax credits — either by increasing the taxpayer’s base erosion minimum tax liability or by interfering with the monetization structures commonly used in tax equity deals.

Historically, 80% of the investment tax credit (ITC) or production tax credit (PTC) were exempt from taxation for entities subject to BEAT. Changes to the BEAT application and the treatment of tax credits would generally eliminate this preferential status.

Foreign investors in US renewable energy projects, both lenders and tax equity investors, may experience disruptions relating to their investment. If an equity investor is resident in a jurisdiction deemed “unfair” (e.g., one with an undertaxed profits rule), their ability to benefit from US energy tax credits could be diluted due to:

Separately, for project sponsors, the effects might include:

The earliest implementation date for these rules, under the House version of the OBBB, is January 1, 2026. While the Senate or the Treasury Department could extend the deadline at their discretion, the current timeline is so short that it can upend investment decisions in the very near term.

Summary of provisions as drafted by the House

Section 899 doesn’t directly eliminate access to energy credits for foreign-backed developers, but it makes using them riskier and more complicated for entities or structures where ownership ties back to jurisdictions flagged as having tax regimes deemed “unfair” under 899. The current text is subject to change in the Senate, and can also be amended or interpreted by the Treasury Department. Nonetheless, the brief implementation period for the proposed changes and their expansive scope raise near-term hurdles for companies raising capital to finance their projects from foreign investors from certain countries.