This is an evolving situation. Find our latest analysis of the bill here.

Following an intense week of negotiations among Republicans, the House of Representatives passed the One Big Beautiful Bill Act this morning on a party-line vote of 215-214-1. The legislation passed with several last-minute modifications, including tighter restrictions on certain clean energy and manufacturing credits.

The Senate is now poised to act to craft their own version of the legislation, and we anticipate they will take a significantly different approach. More on that below.

While the updated House bill significantly narrows the scope of several credits — particularly for non-nuclear participants in the tech-neutral electricity incentive — transferability was treated more favorably in the new proposal. Transferability was fully restored for both the tech-neutral and nuclear credits for the duration the credits are available. In the draft from the Ways & Means Committee, transferability was proposed to be repealed for projects that did not begin construction within two years of enactment. Advanced manufacturing production (§45X), clean fuels (§45Z), and carbon sequestration (§45Q) are still subject to limitation on transferability after 2027 in the draft legislation.

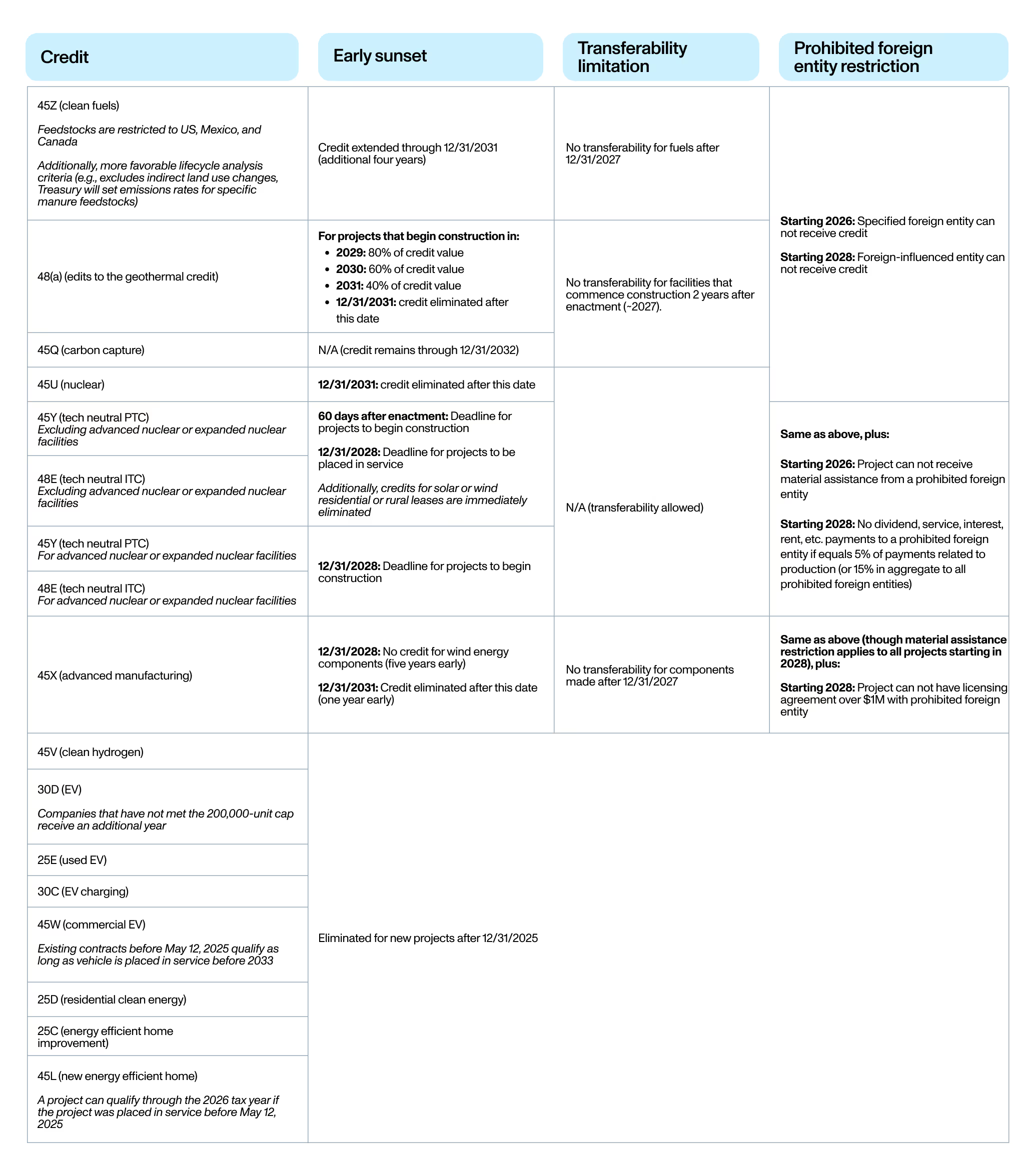

A summary of the key changes:

Read more: Sam Kamyans of Kirkland & Ellis on the House budget bill

Senate Republicans are expected to return from Memorial Day recess during the week of June 2 and begin writing their own version of the legislation. Given the legislation includes a debt limit increase, the Senate is compelled to act ahead of the “X” date, which the Treasury Department currently projects the US will hit by mid-August. Beyond the energy provisions discussed here, the Senate will also need to grapple with cuts to Medicaid and a much higher cap on State and Local Tax (SALT) deductions. Neither set of provisions is popular in the chamber.

Importantly, multiple Senate Republicans have continued to voice their concern with making major changes to the energy and manufacturing tax credits. Following last week’s release of the Ways and Means Committee text (which provided more favorable treatment to a number of credits than the modified text passed today), numerous Republican Senators — representing both the moderate and conservative wings of their party — said significant revisions must be made to secure their support, including:

It is worth noting that, historically, the House version of a reconciliation bill represents the biggest change to law, with the Senate playing the role of narrowing the approach. A good recent example was the initial House-passed version of what eventually became the Inflation Reduction Act (IRA). The House version — initially dubbed Build Back Better — cost nearly $2 trillion and made sweeping investments in social programs, healthcare, education, and housing in addition to clean energy and manufacturing. The Senate passed a much smaller package, where moderates raised concerns about inflationary effects, cost, and the scope of the programs. It was later reworked into the IRA, which passed in August 2022 with a narrower focus on climate, healthcare, and deficit reduction.

As the House was moving toward passage of legislation estimated to add roughly $3 trillion to the national debt, yesterday's spike in the treasury yields — and resulting reaction by the equity markets — underscored policymaking does not occur in a vacuum and could create further pressure on the Senate to significantly limit the scope of the bill.

Given these factors, our view remains unchanged that the Senate will act as a significant moderating force for many of the energy and manufacturing credits, and their changes will be much lighter in touch. Moreover, support for transferability remains strong and we believe that it will emerge largely in place in any potential enacted law.

Please note, this is a fluid situation and any analysis is subject to change. We will continue to monitor developments and provide timely updates as the legislative process unfolds.

Correction: An earlier version of this summary reported that the residential solar leases were eliminated retroactively, starting Jan 1, 2025. That has since been corrected. The legislation eliminates the credit for leased residential solar installations for any taxable year beginning after enactment.