This is an evolving situation. Find our latest analysis of the bill here.

On June 16, the Senate Committee on Finance released draft legislation covering the tax provisions of its version of the One Big Beautiful Bill Act (OBBBA). The Finance Committee text takes a more measured approach to amending the Inflation Reduction Act’s (IRA) energy and manufacturing tax credits compared to the House-passed version. However, if enacted as written, the energy and manufacturing tax credits would still undergo significant changes.

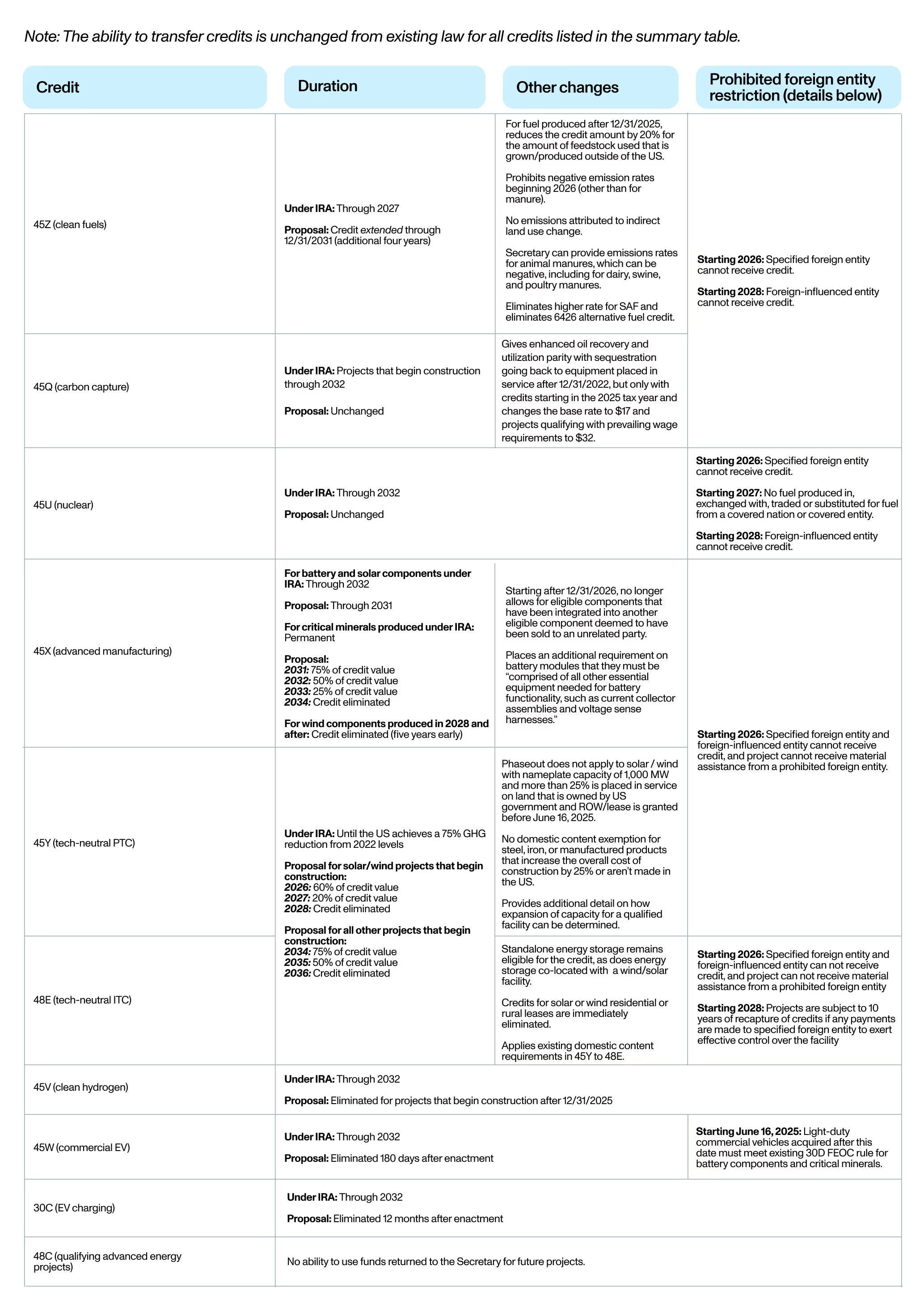

The Senate text restores transferability for the full life of all 12 applicable credits, diverging substantially from the House’s approach, which would have disallowed transferability for several credits — including §45Q, §45X, and §45Z — after 2027. However, the Senate bill imposes a Foreign Entity of Concern (FEOC) test on buyers of transferable tax credits.

The Finance Committee text extends the technology-neutral credits under §48E and §45Y through 2035 (including a three-year phasedown from 2033–2035) with full transferability, but extends different treatment to wind and solar credits. While the House-passed bill disqualified solar and wind projects from tech-neutral credits unless construction commenced within 60 days of enactment, the Senate version allows solar and wind projects to qualify at current credit rates if they begin construction by the end of 2025. The credits then phase down to 60% in 2026 and 20% in 2027, before being fully eliminated in 2028. Notably, the Senate replaces the House’s “placed-in-service” standard with a “commence construction” requirement, offering some relief to project developers.

Additionally, the Senate text does not materially alter the House’s restriction on the use of the §48 credit for residential solar leasing starting in 2026. Combined with the repeal of the §25D home energy tax credit, under the proposal, residential solar incentives availability would be significantly constricted beginning next year.

In contrast to its treatment of solar and wind, the Senate proposal not only retains the IRA’s original timeline for other qualifying power sources — such as nuclear, geothermal, hydropower, and energy storage, including batteries — under the tech-neutral credit regime but cements its availability through 2035 (with a phasedown in 2034–2035). The Senate also largely preserves the timelines for §45Q carbon sequestration and §45X advanced manufacturing credits — albeit with modifications — whereas the House version would sunset these credits after 2028.

In the case of the §45X credit, the Senate proposal imposes phases in FEOC restrictions governing component sourcing (more details below), eliminates the eligibility of wind components after 2027 (as did the House proposal), sunsets battery and solar eligibility one year early (January 1, 2032 rather than January 1, 2033), and sunsets critical mineral eligibility — which was previously permanent — by 2034.

Like the House bill, the §45Z clean fuels credit is extended through 2031.

The Senate bill takes a fundamentally different approach from the House on FEOC restrictions. It introduces a material assistance cost ratio framework — modeled off of the existing domestic content bonus structure — that creates a credit-specific framework for qualification based on the level of non-FEOC input sourcing across technology categories. In addition to meeting these thresholds, projects are still subject to complying with new prohibited foreign entity (PFE) tests related to specified foreign ownership and influence — novel concepts that were introduced in the House package and subsequently amended in the new Senate version (the IRA only imposed a FEOC requirement on the §30D clean vehicle credit).

Initial reactions to the Senate language largely see it as clearer and more workable than the House FEOC provision, but it still will introduce a material, novel compliance burden that could fundamentally constrict the number of qualifying projects across the credits, including for categories with broad bipartisan support such as the §45Q, §45X, and §45Z credits. This provision will face close scrutiny in the coming days, and we expect a range of industry analyses as stakeholders assess its sector-specific impacts.

A summary of the definitions and changes are available in our FEOC cheat sheet.

The Finance text makes numerous additional material changes to the tax code, including new 899 BEAT rules, disqualification of clean energy projects from the modified accelerated depreciation system (MACRS), and expensing (one-year accelerated depreciation) of certain manufacturing and R&D investments.

It remains uncertain whether either chamber has the votes needed to pass its version of the OBBBA. The Senate tax title includes a $10,000 cap on the state and local tax (SALT) deduction, drawing opposition from House Republicans who advocated for a $40,000 threshold (although this is expected to be negotiated further between the two chambers). Additionally, the Senate bill makes deeper-than-expected cuts to Medicaid — another contentious issue that has raised concerns from Republicans from states with significant reliance on the program.

As the energy and manufacturing sectors begin to absorb the implications of the proposed changes to IRA credits, further changes could be requested from supportive Republicans.

In short, Senate Majority Leader John Thune faces a narrow path to securing the votes required for passage — especially as two Republican senators have already voiced their opposition to the current text. House Speaker Mike Johnson likely faces an even steeper challenge, given his razor-thin majority and ongoing intraparty disputes over SALT, Medicaid, and the IRA. There are also growing signs of buyer’s remorse among some original House supporters of the OBBBA.

The White House will likely play a pivotal role in helping Congressional leadership line up the votes needed to pass this key plank of the President’s agenda. Yet numerous hurdles remain — including expected Democratic challenges to the Senate Parliamentarian — to ensure the bill complies with reconciliation rules.

Moreover, with the text now public, lobbying efforts will intensify as stakeholders push for last-minute changes to ease the burden on impacted constituencies — a dynamic lawmakers will likely seek to manage and mitigate as much as possible.

Historically, “trifecta” scenarios (when one party controls the White House and both chambers of Congress) often result in enacted legislation, including portions of the Affordable Care Act, the Tax Cuts and Jobs Act, and the IRA. Still, each has faced unique obstacles on the road to passage, and this round is shaping up to be no exception.

Changes to specific energy and manufacturing credits as of June 16, 2025

Please note, this is a fluid situation and any analysis is subject to change. We will continue to monitor developments and provide timely updates as the legislative process unfolds.