US energy consumption is rising faster than ever before. Driven by factors including artificial intelligence (AI) data centers and domestic manufacturing, electricity demand is projected to increase 35–50% by 2040, an extraordinary surge that creates both opportunity and pressure for clean energy developers and manufacturers.

To capitalize on this growth, developers and sponsors must secure the right type of financing at each stage of a project. With fluctuating interest rates, tighter credit standards, and fragmented capital access, a solid financing strategy is critical.

This guide covers renewable energy project finance throughout the project lifecycle — walking through each stage, exploring today’s investment climate, and sharing tips to secure capital and bring projects to life.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

The clean energy sector is entering a historic period of growth. In the US, $276 billion was invested in clean energy manufacturing and deployment across H2 2024 and H1 2025, an 8% increase from the previous year. This upward investment trend is expected to continue as electricity demand rises.

Amid this growth, navigating clean energy finance requires careful planning and flexibility. Not only does each project require multiple types of capital at different stages, but investor appetite can vary widely depending on project size, technology, risk profile, and track record of the parties involved. There is no one-size-fits-all finance solution; each deal is a bespoke, high-effort process.

Our research shows how uneven access to funding can be. Fewer than one in three developers report that traditional tax equity is generally available for their projects, underscoring how deals frequently struggle to secure financing. In many cases, deals are dependent on existing relationships, limiting developers’ access to qualified and competitive lenders. Establishing new connections is often a long, manual process.

Without access to a broader, more diversified, and more competitive market, developers may struggle to secure the type or amount of funding needed, when it’s needed. This can slow or even stall a project. In some cases, developers can be forced to accept less favorable terms to avoid costly delays.

Each lifecycle stage calls for different sources of capital. Understanding how they work together is essential to building a bankable project. The main types include:

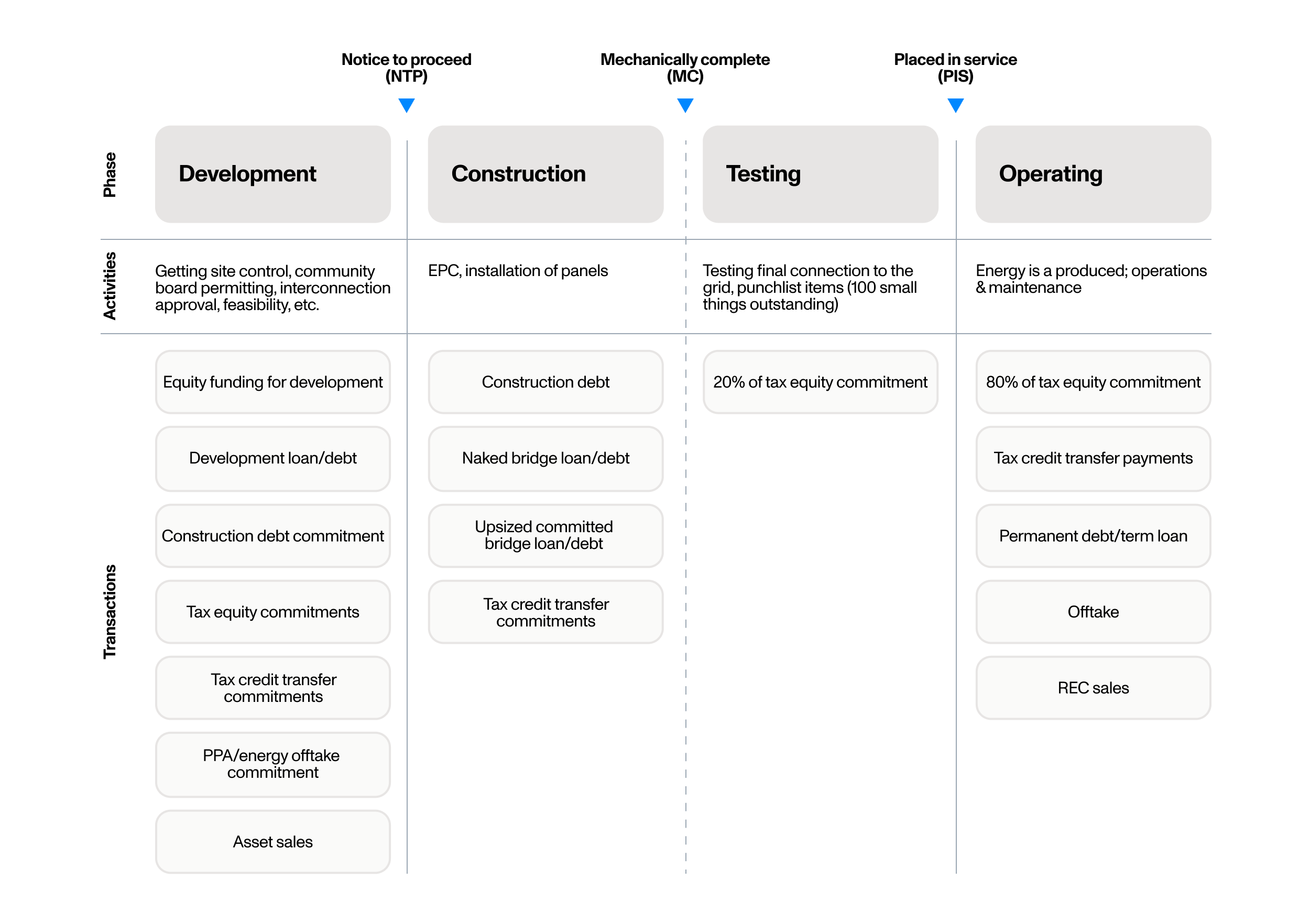

Together, these form a layered capital stack for a project. Debt provides upfront liquidity and is repaid over time using project revenues. Tax equity and credit transfers monetize tax benefits, reducing the need for more expensive capital. While debt is used throughout construction and operations, tax equity typically commits during the construction phase — tax credit eligibility requires investors to join before the project hits its commercial operation date (COD). Transferable tax credits are generally executed post-COD as a one-time sale.

Knowing what type of financing is needed at each stage helps teams plan ahead and approach lenders with greater clarity. The core stages are:

Stages of the project finance lifecycle

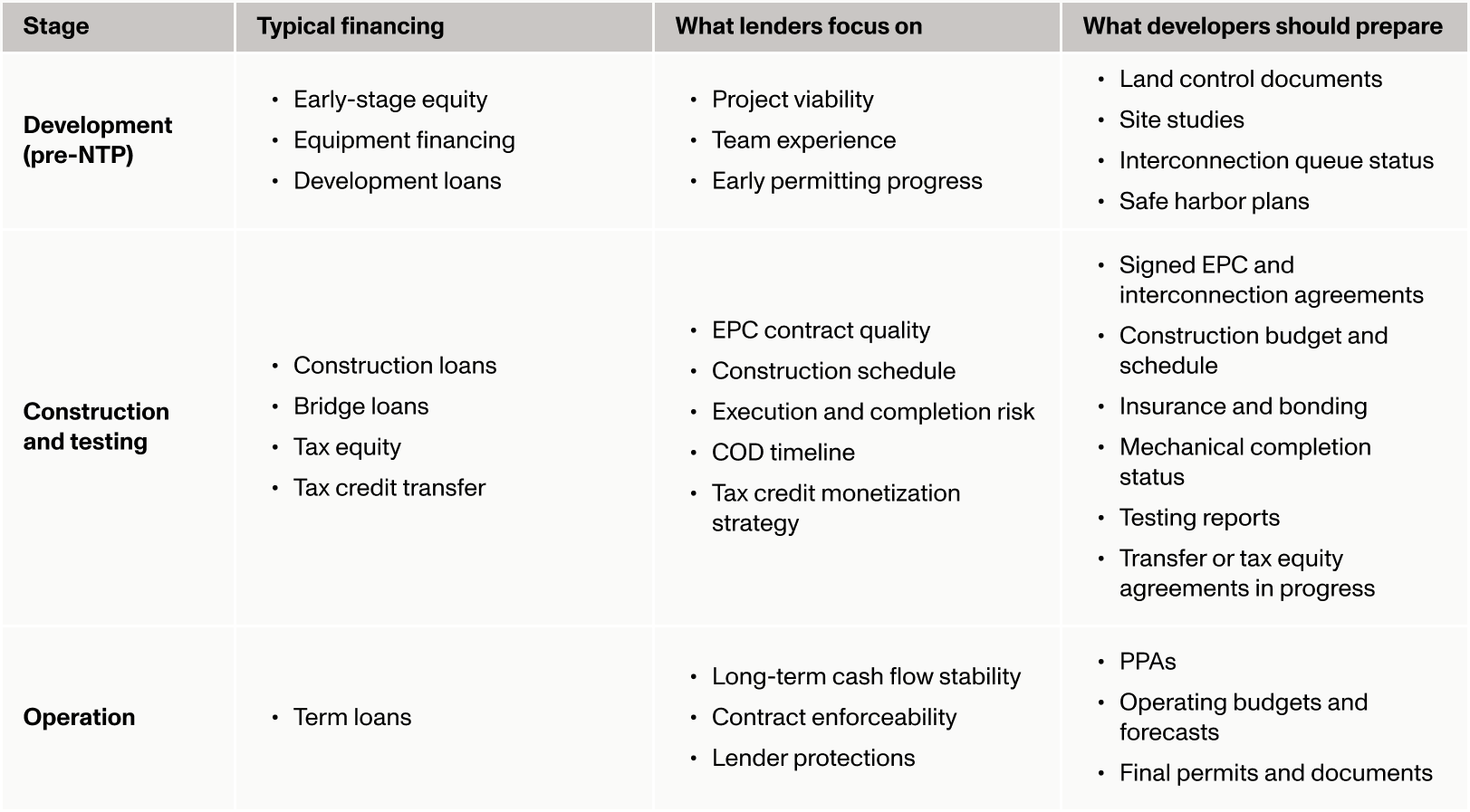

Before notice to proceed (NTP), developers raise early capital to advance the project and make it financeable. This often includes securing land, permits, interconnection, and equipment — frequently before revenue or creditworthiness is established.

In light of recent legislative changes, equipment financing has become a crucial component of early-stage development funding. For solar and wind projects in particular, using debt financing to purchase qualified equipment and begin physical work helps developers meet Internal Revenue Service (IRS) requirements and preserve eligibility to monetize their clean energy tax credits.

Once a project reaches NTP, construction can begin. Capital needs grow as teams procure equipment and labor. Financial scrutiny also increases as lenders assess risk, so it is important to demonstrate the ability to deliver on time and on budget.

Construction loans are the primary financing tool at this stage. These loans typically cover the majority of construction costs and are structured around interconnection, revenue contracts, permitting, and detailed engineering, procurement, and construction (EPC) contracts. Tax equity is also raised during the construction stage, as the tax equity partner must own an interest in the project prior to COD in order to qualify for tax credit benefits.

As construction nears mechanical completion — the point at which all major equipment is installed and the project is physically built — testing begins. This includes final inspections, grid connection, and ensuring the system is ready for operation. Because this stage often involves ongoing costs while developers await tax credit payments or finalize long-term financing, bridge loans are typically raised in tandem with construction financing and close alongside construction loans. Short-term bridge loans are secured against expected tax credit proceeds and help cover expenses during the transition to commercial operations.

Once a project reaches COD, it begins generating revenue and enters the operational phase. At this stage, construction loans typically convert to long-term debt, which helps reduce financing costs. These loans are repaid using project cash flows from contracted power sales, renewable energy certificates (RECs), or other sources such as capacity payments or storage incentives.

At this point, ongoing monitoring becomes essential. Developers must track performance output, ensure compliance with offtake agreements, and manage operational risks to maintain lender confidence. Strong performance data and reliable operations support debt repayment and position the project for future optimization or asset sales.

Debt is the backbone of the capital stack — and the most susceptible to changing market conditions. Today, developers face a more cautious lending environment shaped by higher rates, tighter credit standards, and growing segmentation among borrowers.

Overall, clean energy lenders are pricing more selectively due to ongoing inflationary pressures and rising interest rate expectations. Base rates remain elevated and spreads have widened, particularly for non-rated sponsors or projects involving newer technologies. As a result, financing costs have increased and lenders are applying greater scrutiny to deal fundamentals, including developer track record, project readiness, and technology maturity.

These conditions mean that not all developers are accessing capital on equal terms. Borrowers with proven experience and standardized documentation are better positioned to secure competitive debt, while those who are less prepared will face higher costs and more limited options. That’s why clear deal preparation and strategic lender alignment are critical.

In today’s selective, cost-sensitive market, developers must think strategically about how to raise capital amid rising rates and shifting lender priorities:

Come prepared with a clear, consistent story about a project’s risk, revenue model, and readiness. That can include building lender-ready data rooms with standardized templates, credible offtake agreements, detailed project timelines, and clear explanations of safe harbor status or tax credit eligibility.

Track current pricing trends, advance rates, and required terms to anticipate how lenders will underwrite projects. Tools that surface real-time market data and lender-specific requirements can provide the transparency developers need to refine deal structures and avoid surprises.

Lenders assess clean energy projects through the lens of risk and repayment. Their primary concern is whether a project will generate steady, predictable cash flows that can reliably service debt over time.

They typically focus on the following areas:

Financing is easier with a strong buyer under a long-term power purchase agreement (PPA). Lenders review offtaker quality, contract tenor, and pricing terms to confirm stable revenue.

Beyond the offtake, lenders look for other sources of contracted cash flow, such as storage incentives, capacity payments, or RECs. High levels of contracted revenue reduce reliance on short-term energy markets and provide more predictable returns.

Lenders want to know if the sponsor has successfully completed similar projects in the past. A strong track record helps establish credibility and lowers perceived execution risk, especially in tougher financing conditions.

Proven, commercially deployed technologies (e.g., utility-scale solar or lithium-ion storage) are more likely to meet lender risk thresholds than newer, less validated solutions. Emerging technologies can still attract capital, but usually require equity backing or risk mitigation strategies such as guarantees or performance insurance.

Project readiness includes having land rights secured, interconnection agreements in place, necessary permits obtained, and key project documentation prepared. The more complete and organized a project is, the more likely lenders are to engage seriously.

Lender priorities throughout the project finance lifecycle

Want more insights on lender sentiment and market trends? Download our 2025 mid-year market intelligence report for updated benchmarks and insights from across the clean energy debt market.

Timelines vary by project size, existing lender relationships, risk profile, technology, and lifecycle stage. Larger or first-of-a-kind projects generally require more diligence and longer execution periods.

Equipment financing via safe harbor allows developers to start construction sooner and de-risk a project’s eligibility for tax credits. Under Treasury Notice 2025‑42, solar projects larger than 1.5 MW and all wind projects must begin physical work by July 4, 2026, to qualify for tax credits. Solar projects smaller than 1.5 MW can still use the 5% cost method until that date. While most clean energy technologies aren’t affected, these changes raise the bar for solar and wind projects, making early planning and documentation even more critical to securing tax credit financing.

Smaller-scale clean energy projects often face more limited finance options because traditional capital providers tend to prioritize larger deals. However, these developers can still access funding through community banks, mission-driven lenders, green banks, or specialized funds focused on distributed energy.

Transferable tax credits have also opened up new opportunities for smaller projects to monetize incentives by selling credits directly to third-party buyers.

Each lender varies in terms of how they determine a project's viability. That said, common metrics include:

Lenders evaluate construction and completion risk by reviewing the credibility of the developer, contractors, and suppliers, along with project contracts and timelines. They often hire independent engineers to assess technical details such as equipment specs, interconnection feasibility, and energy yield projections. This helps ensure the project can be delivered on time, on budget, and at expected performance levels.

Historically, the project finance process has been long and fragmented. Without centralized data or pricing benchmarks, much of the process relies on one-off outreach and manual coordination that can involve months-long email chains and reliance on spreadsheets.

Top challenges include:

Crux brings greater structure, visibility, and liquidity to renewable energy finance by centralizing the full capital stack in one platform. Instead of navigating a fragmented process with different providers at each stage, developers can manage and access all their finance needs in one place. With a vetted network of 120+ capital providers, standardized documentation, lender-specific requirements, and real-time pricing signals, Crux makes the financing process faster and more scalable.

Crux helps developers:

Looking to dig deeper on market dynamics? Download our whitepaper for more insights on how the clean energy finance landscape is evolving.