Many factors influence capital cost and availability for a given clean energy project. Investors are diverse, as are the types of projects they’re willing to invest in, the risk factors they consider, and their expectations regarding returns.

To better understand the current state of capital availability, Crux conducted a survey of project finance lenders and investors in March and April of 2025. We received responses representing more than $225 billion in total capital allocation to energy and manufacturing projects across the project lifecycle.

Go deeper: Read the full report on lending and investments

Crux collected data about various stages of the project development lifecycle, including:

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

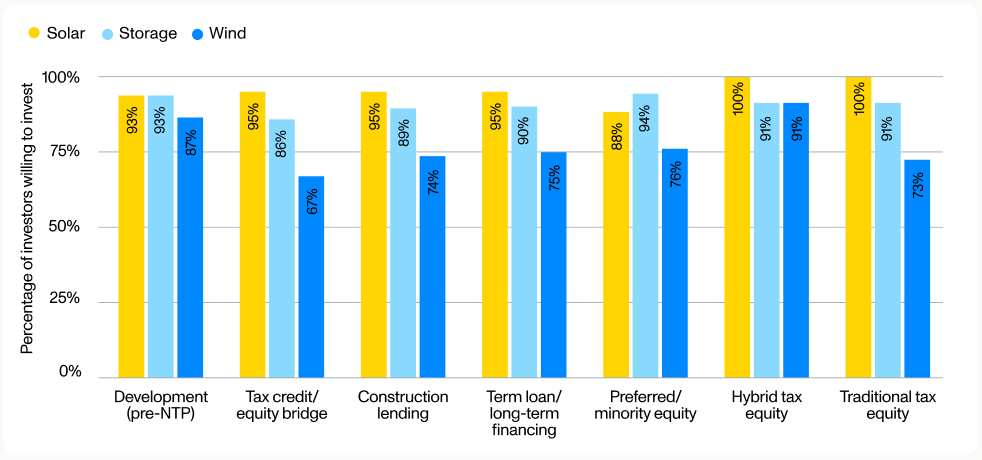

Capital is generally the most available and affordable for solar (including solar + storage) and wind energy projects with investment-grade (IG) sponsors. Solar energy projects benefit from the widest availability of capital across the entire project finance lifecycle, with, in aggregate, more than 90% of survey respondents indicating that they are willing to invest in solar projects from the pre-NTP stage to term loan/long-term financing.

Storage projects have similarly strong capital access, while onshore wind projects generally saw less robust capital access across the development cycle.

Availability of capital for established energy technologies

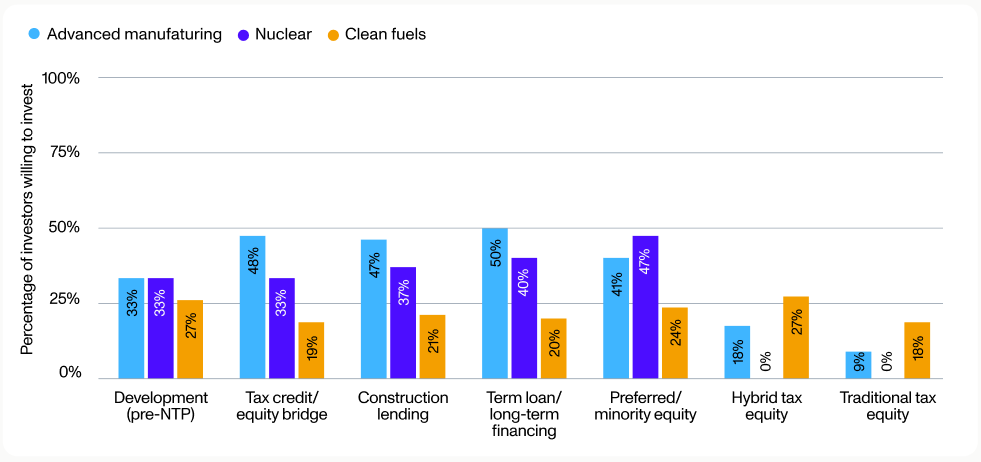

Solar, storage, and wind projects are just one part of the large and diverse energy complex. The universe of projects that fall into the less-established category is wide, ranging from clean fuels and carbon capture projects to nuclear plants, geothermal, critical minerals production, advanced manufacturing facilities, and more.

The tax credits for these technologies have important differences relative to the conventional electricity credits, which can make securing financing for new infrastructure more complex. However, a rising share of investors is starting to look at new technologies — in particular at advanced manufacturing projects. Between 30 and 50% of the investors surveyed indicated that they were open to investing in new manufacturing infrastructure through the development lifecycle.

Availability of investment for less-established technologies

Market transparency is key for continued investment and support for these less-established technologies. Both developers for less-established technologies and smaller developers of solar, storage, and wind projects benefit from a wider and more liquid market for capital.

Crux’s debt marketplace aims to bring transparency and liquidity to the energy market and manufacturing industry. Our network of more than 100 lenders provides capital at all stages of the project finance lifecycle, and our leading platform ensures that lenders and developers are able to make the best matches for their financing strategy. Learn more.