With the rise of tax credit transferability, financing structures for clean energy developers and manufacturers have evolved rapidly. Among the most prominent structures are tax credit bridge loans. In 2024, one in five transactions included a forward commitment to purchase tax credits, and Crux research found that more than 90% of those forward investment tax credits (ITCs) were used to obtain a bridge loan.

This guide walks through the mechanics of tax credit bridge loans, from structure and pricing to lender expectations and repayment dynamics. It’s designed to help developers and manufacturers understand when bridge financing makes sense and how to position projects for successful execution.

Tax credit bridge loans are short-term financing tools that provide upfront capital based on future tax credit generation and monetization. They bridge the timing gap between when capital is needed and when proceeds from the sale of tax credits are received. In most cases, these loans are raised during construction alongside the construction loan. For example, a project expecting to generate $20 million in future credits could receive an advance of roughly $16 million at an 80% rate. Importantly, tax credit bridge loans are not priced at 100 cents on the dollar.

There are several variations of bridge loan structures depending on the financing approach and investor type:

These variations allow developers flexibility in structuring capital to fit the desired risk profile and investor appetite. Because it is repaid directly from tax credit transfer proceeds, the tax credit bridge loan structure allows sponsors to reduce the amount of equity needed to fund construction, creating a more efficient capital stack.

Comparison of bridge loan structures

Bridge financing depends entirely on how a project monetizes its tax credits. If a project is transferring its credits rather than raising tax equity, it uses a tax credit bridge loan to advance capital ahead of the transfer payment. These loans are most helpful when credits make up a large share of project value and when there is a long timing gap between capital needs and when transfer proceeds are received.

A tax equity bridge loan, on the other hand, is only used when a project raises traditional tax equity and needs to bridge committed investor funding. Because the tax equity investor is already committed, the bridge relies not on securing an investor but on the sponsor’s ability to complete construction, the investor’s creditworthiness, and meeting the funding conditions in the tax equity agreement.

In practice, the choice between the two is determined by the project’s tax credit monetization path: projects monetizing through transfer use tax credit bridge loans, while those raising tax equity use tax equity bridge loans.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

There are a few key drivers of pricing and financial terms for tax credit bridge loans that shape lender risk and market appetite. The most important factor is whether the bridge loan is raised on a committed or uncommitted basis, which drives repayment certainty and cost of capital. Other major factors include the sponsor’s experience, the maturity of the technology, and project-level risks such as construction status and permitting. Together, these elements determine how aggressively lenders can underwrite a bridge loan and how competitively a project can secure capital.

In a committed structure, the developer has reached an agreement with a buyer who will purchase the tax credits before securing the loan. This certainty allows lenders to offer higher advance rates and lower costs of capital.

Uncommitted structures, on the other hand, involve securing financing before identifying a tax credit buyer. Because of the uncertainty involved, uncommitted loans tend to have higher pricing, lower advance rates, and a narrower lender market.

Cost of capital for committed and uncommitted tax credit bridge loans

Pricing and lender appetite also vary by technology type. Solar and battery energy storage projects represent the most established segment, with competitive pricing and the highest certainty of close. Advanced manufacturing projects exhibit wider pricing ranges, reflecting a newer market, higher perceived risk, and general market opacity. For context, advanced manufacturing construction loans price significantly wider than traditional energy projects — typically SOFR + 400–1000 bps — reflecting the same underlying risk factors that often influence tax credit bridge loan underwriting.

These technology distinctions are important when comparing tax equity bridge loans and tax credit bridge loans. Because a tax equity bridge loan is only available once tax equity has been committed, it naturally applies only to projects and technologies that meet tax equity investors’ underwriting standards. In practice, this limits these loans to mature, proven sectors such as solar and wind, where investors have long track records and established underwriting frameworks. Tax credit bridge loans extend to a broader set of technologies — including advanced manufacturing, nuclear projects, and clean fuels — but typically carry higher pricing to account for greater perceived risk and more limited lender experience in these sectors.

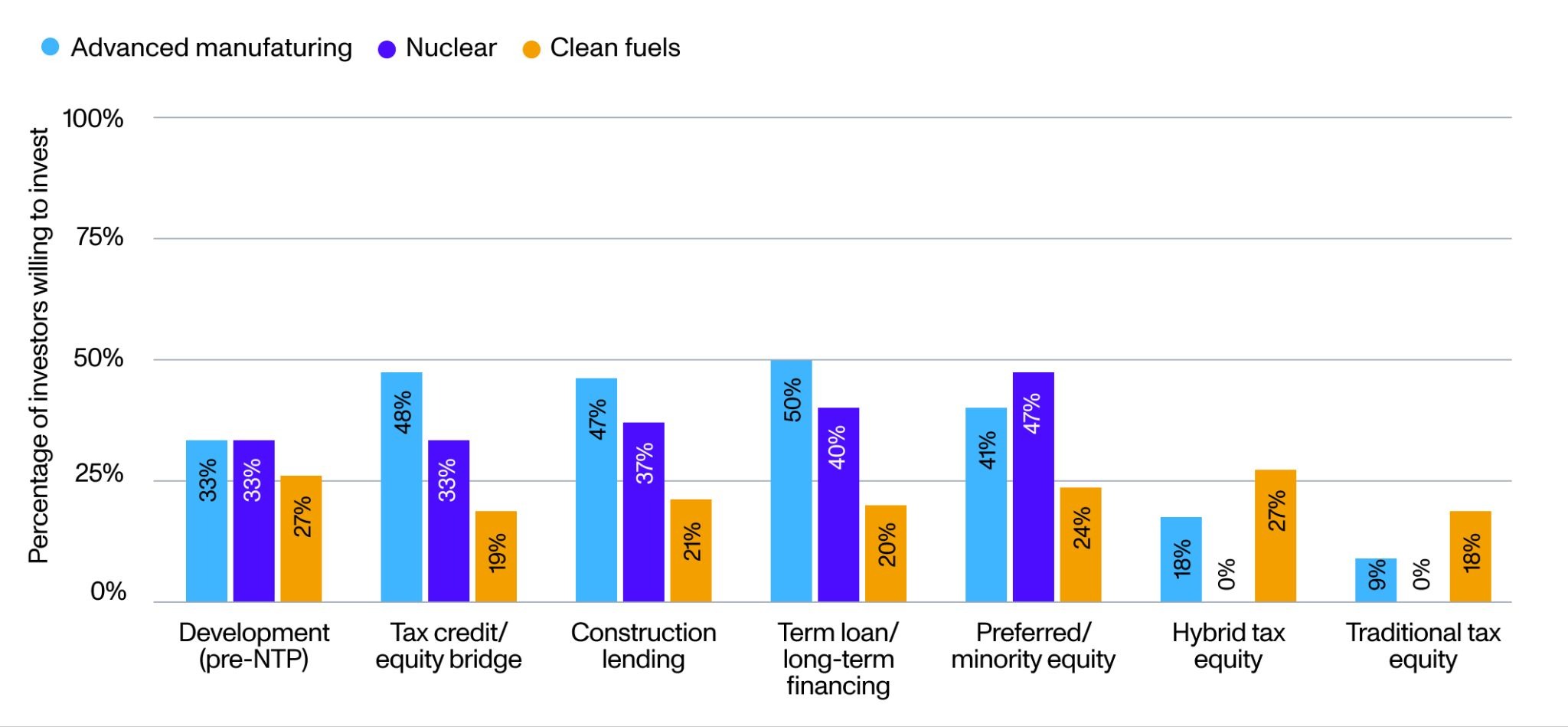

While emerging technologies command higher premiums, they are expected to see gradual improvement as lenders gain more experience. Notably, for tax credit and equity bridge loans, 48% of investors are willing to participate in advanced manufacturing deals, 33% in nuclear projects, and 19% in clean fuels.

Availability of investment for less-established technologies

In a committed bridge loan, once the project reaches PIS or manufactures qualifying products, the pre-agreed buyer purchases the tax credits and the sale proceeds are used to repay the bridge.

In uncommitted structures, the borrower can find a buyer both before or after the credits generate, negotiate a sale, and then repay the loan from the proceeds. Payment timing varies by credit type. Production-based credits are typically paid quarterly in arrears, leading to staggered repayment. ITCs are generally paid once at PIS, unless multiple projects reach PIS at different times, in which case payments may occur on a rolling or quarterly basis.

Lenders evaluate a range of risk factors when underwriting tax credit bridge loans. On the project side, they assess whether credits will be generated as projected, the stability of the regulatory and policy environment, the historical performance of the underlying technology, and the likelihood of project completion. On the sponsor side, lenders focus on development experience, track record, financial strength, and prior success monetizing credits.

According to Norton Rose Fullbright and Stafford, to help manage the higher risk associated with uncommitted structures, lenders are increasingly using insurance products or credit guarantees that backstop the buyer’s payment obligation — particularly when the buyer is not investment-grade. This added protection has given lenders greater confidence in financing naked deals, helping to expand participation in the uncommitted bridge loan market.

Another key consideration when structuring tax credit bridge loans backed by ITCs is the potential for recapture. Under Internal Revenue Service (IRS) rules, ITCs vest over a five-year period rather than being granted all at once. If a project changes ownership or faces foreclosure during that time, the unvested portion of the credits can be recaptured —– meaning the IRS takes them back.

To avoid this, Latham & Watkins shares that many deals are structured through partnership or affiliate holding entities, which allow lenders to foreclose on equity interests without triggering recapture. In other cases, the risk is mitigated through interparty or forbearance agreements, under which the lender agrees not to foreclose during the five-year vesting period. These measures help protect the value of the ITC while still enabling lenders to provide short-term bridge financing safely.

Lenders evaluating a tax credit bridge loan require two broad categories of information: (1) upfront documentation to underwrite the transaction and (2) collateral and reporting requirements to monitor the loan. Lenders expect developers looking for a tax credit bridge loan to provide a well-defined legal and tax structure along with a clear tax credit monetization plan, whether the strategy is committed or uncommitted. Adequate insurance coverage — including builder’s risk, liability, and property insurance — is essential.

Ongoing reporting typically includes monthly financial statements, tax credit–generation tracking, and construction milestone updates. If applicable, safe harbor compliance documentation is also required. Typical collateral packages include tax credit entitlements as the primary collateral, project assets and equipment as secondary collateral, sponsor guarantees as supporting collateral, and operational cash flow as additional support.

To successfully pursue a tax credit bridge loan, developers should begin by confirming project eligibility and timing — ensure the project qualifies for transferable credits and understand when those credits will be generated. From there, articulate a clear monetization strategy, including whether to pursue a committed or uncommitted structure, and identify potential credit buyers early in the process.

Once the project has secured key milestones, and demonstrates clear transaction readiness, engage with lenders to discuss project details, structure preferences, and current market appetite. Crux can help facilitate these conversations by connecting developers with active lenders and streamlining the financing process. Finally, prepare key documentation such as financial statements, construction milestones, insurance coverage, and credit-generation details to support lender underwriting.

As the clean energy market continues to mature, tax credit bridge loans are becoming a core part of project finance. By unlocking earlier access to capital and reducing equity requirements, these loans enable more developers to move faster and scale more efficiently.

Crux’s tech-enabled debt marketplace, expert team, and broad lender network make it easy to connect with the right counterparties for tax credit bridge loans. Get in touch to learn more about our debt capital markets offering and to connect with the Crux team.