The market for transferable tax credits has taken off, catalyzing billions of dollars of investment into domestic energy and manufacturing projects. Prior to transferability, the only way for developers to monetize their tax credits was through complex tax equity partnerships with large financial institutions. Transferability has made the market more accessible to a wider range of developers and manufacturers, especially for smaller developers and newly eligible technology types.

Transferability has also widened the pool of taxpayers that can purchase tax credits. While tax equity partnerships are typically offered by a small group of large banks, transferability expands the market of potential tax credit buyers to any corporate taxpayers.

A wider market — on both the sell side and the buy side — means increased competition. Sellers must find ways to make their tax credits stand out.

This guide explores best practices that project developers and manufacturers can utilize to make their credits more appealing, ultimately generating more bids and maximizing the value of the credits.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

The Inflation Reduction Act, passed in 2022, permits certain federal clean energy and manufacturing tax credits to be sold for cash, creating a more efficient way to deploy and recycle capital. Buyers earn a discount on the credits, reducing their tax liability and making participation in clean energy finance more appealing.

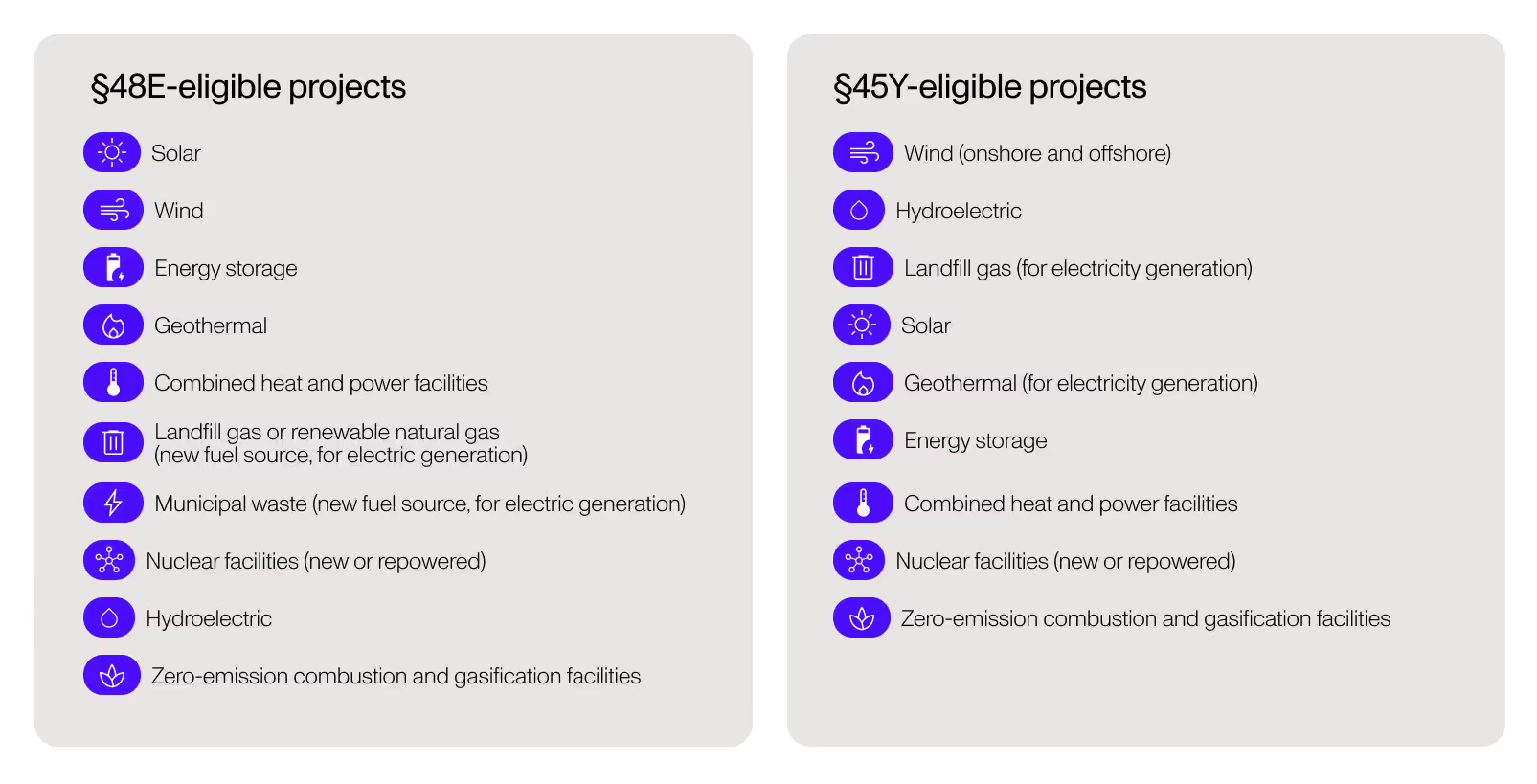

For projects that start construction after 2024, these tax credits come in the form of the §48E clean electricity investment tax credit (ITC) and the §45Y clean electricity production tax credit (PTC), which have replaced the traditional ITC and PTC framework. The §48E and §45Y credits are also referred to as the tech-neutral tax credits.

ITCs are one-time credits based on a percentage of capital investment in a project, while PTCs are per-unit credits based on the amount of energy produced by a renewable energy project or the number of components manufactured over a specific period.

Projects that qualify for the tech-neutral tax credits include:

Selling tax credits offers numerous advantages to tax credit sellers. From the seller’s perspective, participating in this market can:

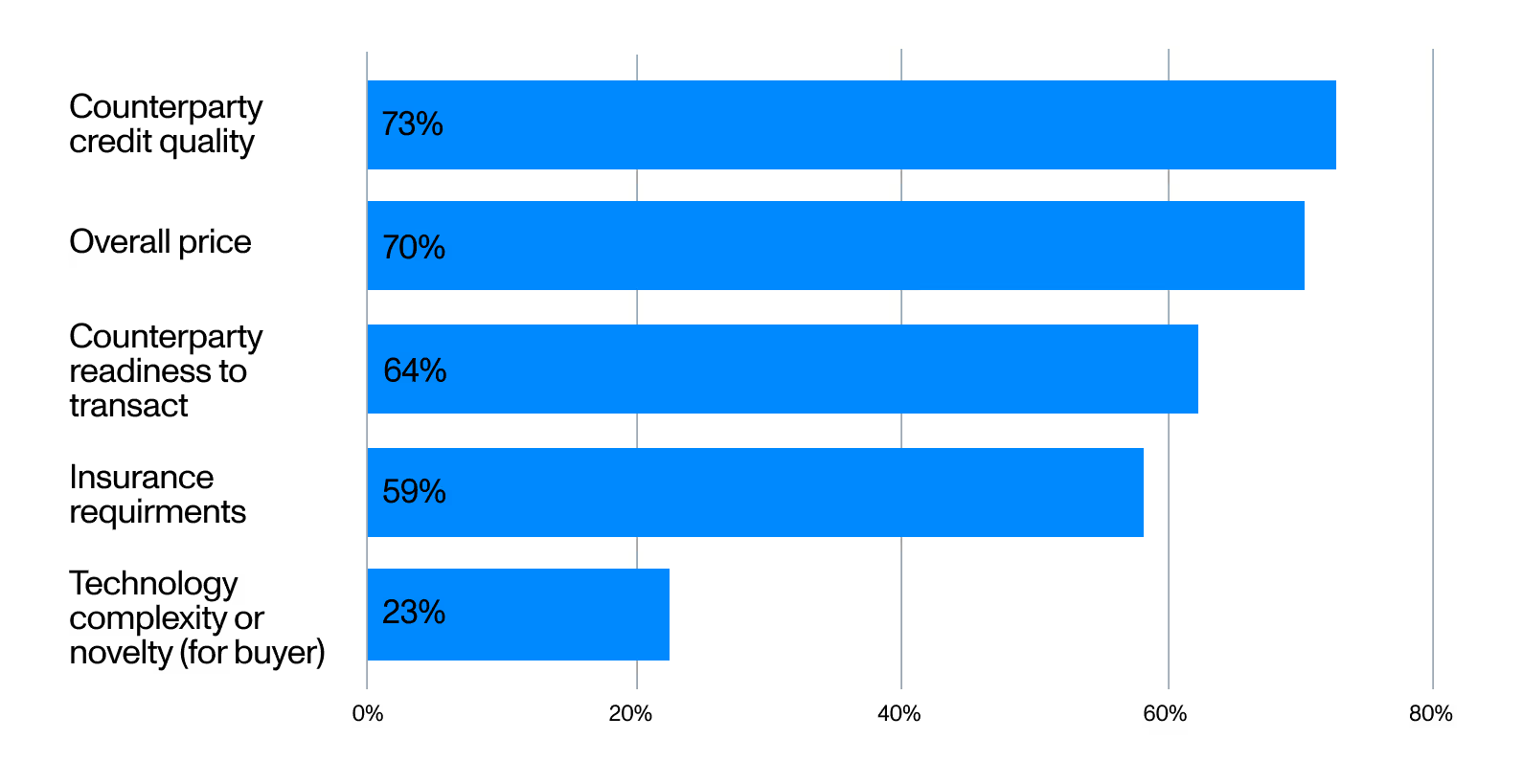

A range of factors can affect deal pricing for transferable tax credits, including:

Crux’s data shows that tax credit buyers are increasingly looking for experienced sellers that are ready to transact. The following best practices can help developers and manufacturers stand out as good transaction partners.

According to Crux’s data, 73% of tax credit buyers and advisors prioritize counterparty credit quality when selecting credits to bid on. Understanding what buyers are looking for is critical to effectively marketing yourself as a seller.

Factors that buyers and advisors consider when evaluating tax credits

Providing comprehensive information about credit quality upfront can increase competitiveness and ensure that a newly listed project gets circulated to the widest audience of buyers via Crux’s automated alerts. Fill out as much detail as possible for a given project to ensure that buyers have a full picture of the credit and underlying project.

When listing on Crux’s transferable tax credit marketplace, sellers can upload details about their track record and high-level financial metrics. On average, sellers on Crux with more robust profiles are more likely to receive bids. The most successful sellers fill out all or most of the fields on their seller profile, including information on:

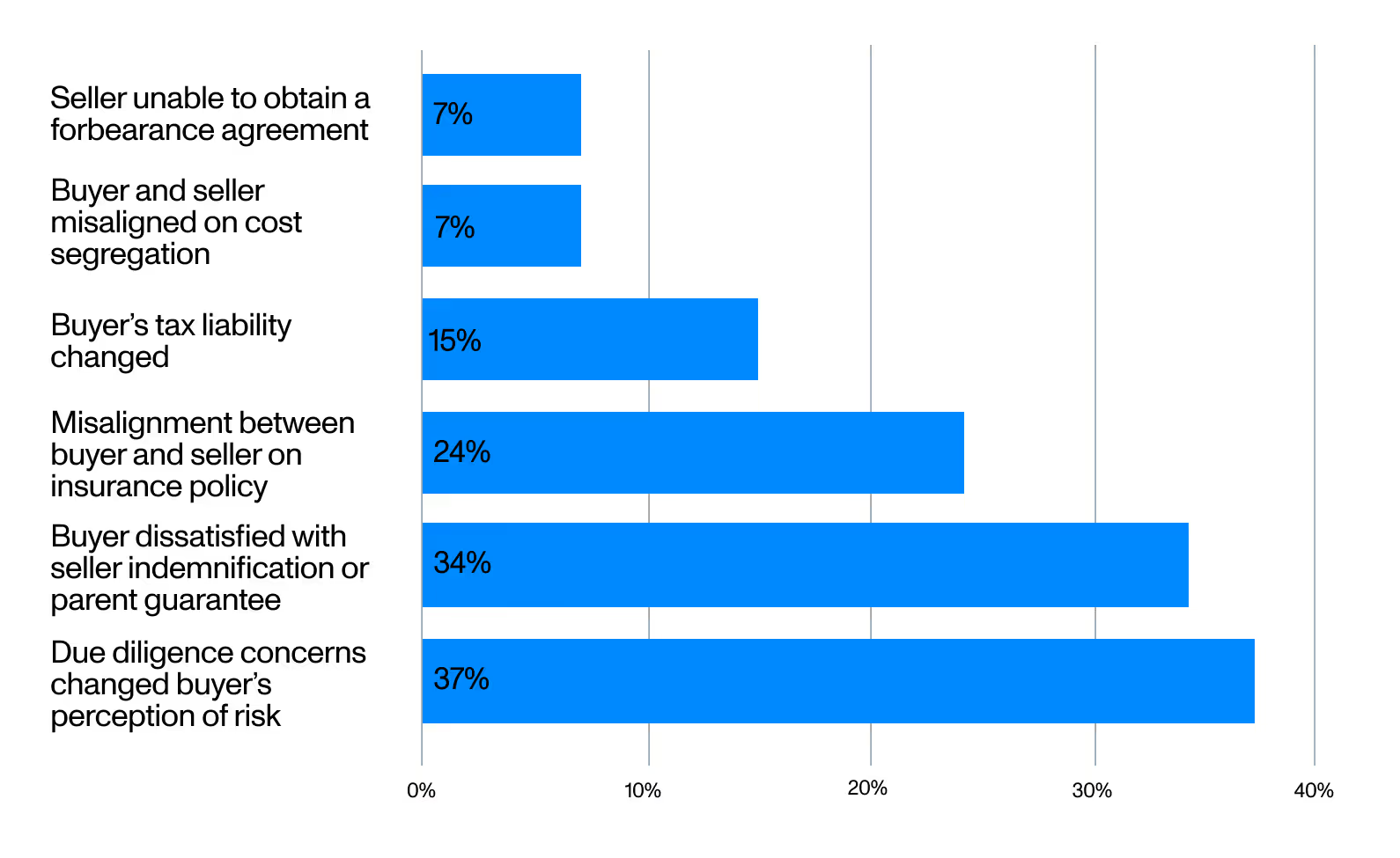

Developers and manufacturers should keep in mind that, to buyers, tax credit purchases are primarily economic transactions. Buyers prioritize managing their tax liabilities and mitigating risk throughout the transaction process. Readiness to transact is one of the most important factors they consider, cited by 64% of buyers.

Crux research has identified several reasons for transaction delays when selling tax credits:

Most common causes of delay or derailment for a tax credit transaction

Because due diligence and risk mitigation are the most common causes of transaction delays, Crux recommends that tax credit sellers prepare the due diligence items that our data indicate are most likely to streamline a deal. Compile documentation across the following categories:

Crux surveyed 35 of the leading law firms, insurers, tax advisors, and financial institutions in the market to identify the essential due diligence items for a transferable tax credit transaction. Learn more in our risk mitigation and due diligence whitepaper.

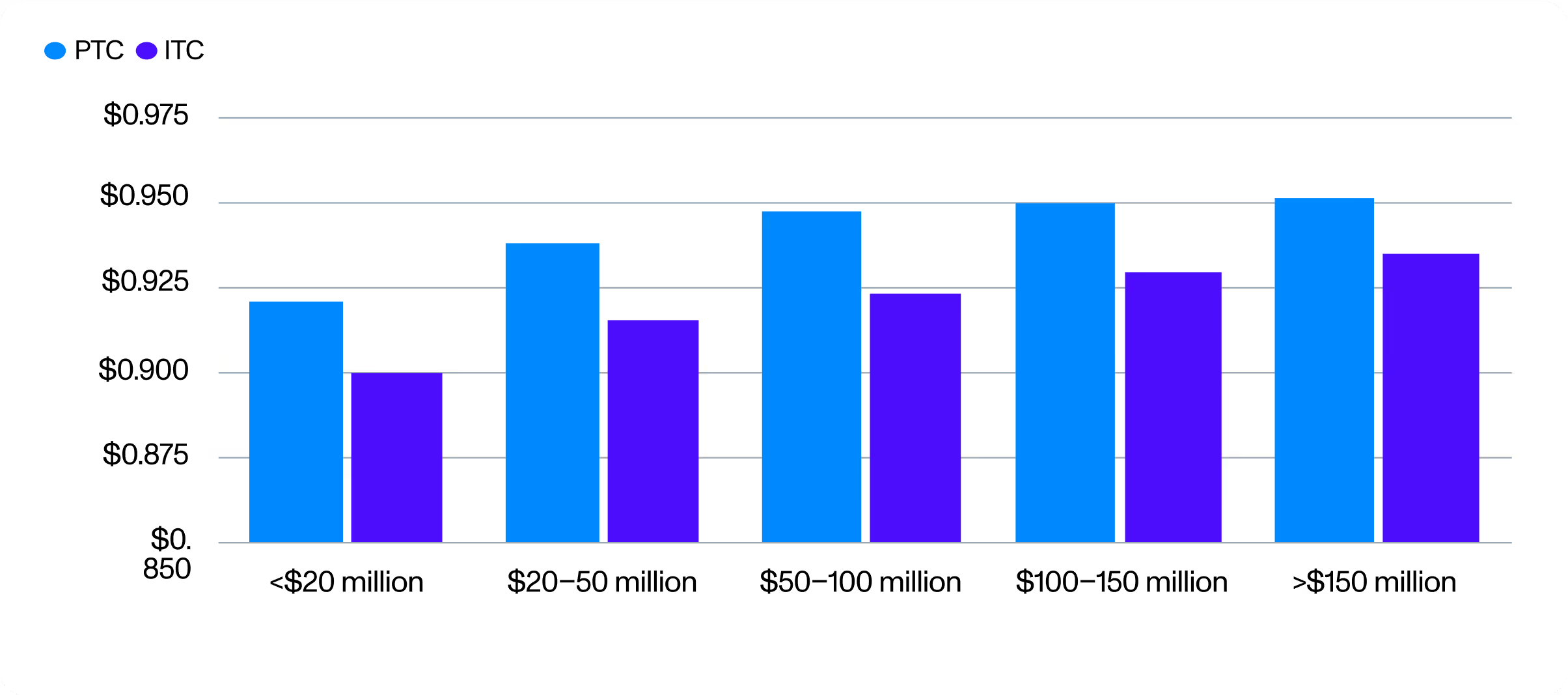

Competitive pricing benefits both buyers and sellers. Buyers seek competitively priced credits to manage their tax liability and maximize return on investment. Seventy percent of buyers and advisors say they optimize for price when selecting which credits to bid on. Sellers have a higher chance of transacting when the deal is competitive.

Average price by deal size tranche, PTC and ITC, 2024

As discussed above, deal size is an important driver of pricing for both ITCs and PTCs. Pricing tends to vary most across small deals, as recapture and basis risk, relevant mainly to ITCs, has an outsized role in small credit pricing in a market segment where insurance is difficult or not economically viable to procure.

Crux uses various pricing factors to support a transparent market price estimate, including taking in feedback from sellers. Crux equips all sides of the market with regularly updated price estimates, called the Cruxtimate, for each credit based on data from more than $30 billion in tax credit transactions.

These estimates allow buyers and sellers to align on realistic pricing expectations and drive both parties toward a deal efficiently. Running a wide, transparent process allows sellers to optimize their tax credit transfers across price, timing, and other negotiated terms.

Ready to optimize your tax credit transactions? With more than 600 counterparties in Crux’s network, developers and manufacturers can plug into a large, liquid marketplace. For more information on how to make your tax credit transaction more efficient and competitive, get in touch with us.