Since January 1, 2025, clean energy and manufacturing projects have been eligible for the new, technology-neutral §45Y production tax credit (PTC) and §48E investment tax credit (ITC). With a finite supply of legacy §45 PTCs and §48 ITCs available, these technology-neutral credits are going to make up a larger share of the transferable tax credit market moving forward. It’s critical for buyers to understand the changes.

See how Crux supports corporate tax teams

Legacy tax credits refer to the established §45 PTC and §48 ITC that have provided the backbone of renewable energy tax credits since 1992 and 2005, respectively. These credits are technology-specific, with distinct qualification criteria, rates, and structures for each qualifying technology (e.g., wind, solar, clean fuels, and advanced manufacturing).

The new, technology-neutral tax credits are not based on specific technology types. Instead, any new projects that generate electricity with no greenhouse gas (GHG) emissions automatically qualify for the Internal Revenue Service’s (IRS) determination of eligible facilities.

The regulations for the technology-neutral tax credits categorize electric-generating projects into two major categories:

A C&G facility is one which, according to the IRS, “produces electricity through combustion or uses an input energy source to produce electricity.” Most familiar clean energy projects — solar, wind, battery energy storage, geothermal, and nuclear — are deemed by the IRS to be non-C&G facilities.

The shift in regimes reflects a desire to create a more expansive market for clean energy technologies. Rather than requiring new legislation for each emerging technology, the tech-neutral framework allows new, zero-emission technologies an easier path to qualifying for tax credit eligibility. Like legacy tax credits, the technology-neutral tax credits are transferable. For tax credit buyers, this transition creates both opportunities and complexities.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

Projects that began construction before January 1, 2025 can claim the legacy tax credits. Per IRS Notice 2013-29, a developer must typically demonstrate that they incurred at least 5% of the facility’s project costs or began physical work before the expiration of the legacy ITC or PTC. They must also demonstrate that they have worked toward the project’s completion continuously since beginning construction.

Projects that begin construction after December 31, 2024 are eligible for the tech-neutral §45Y and §48E credits.

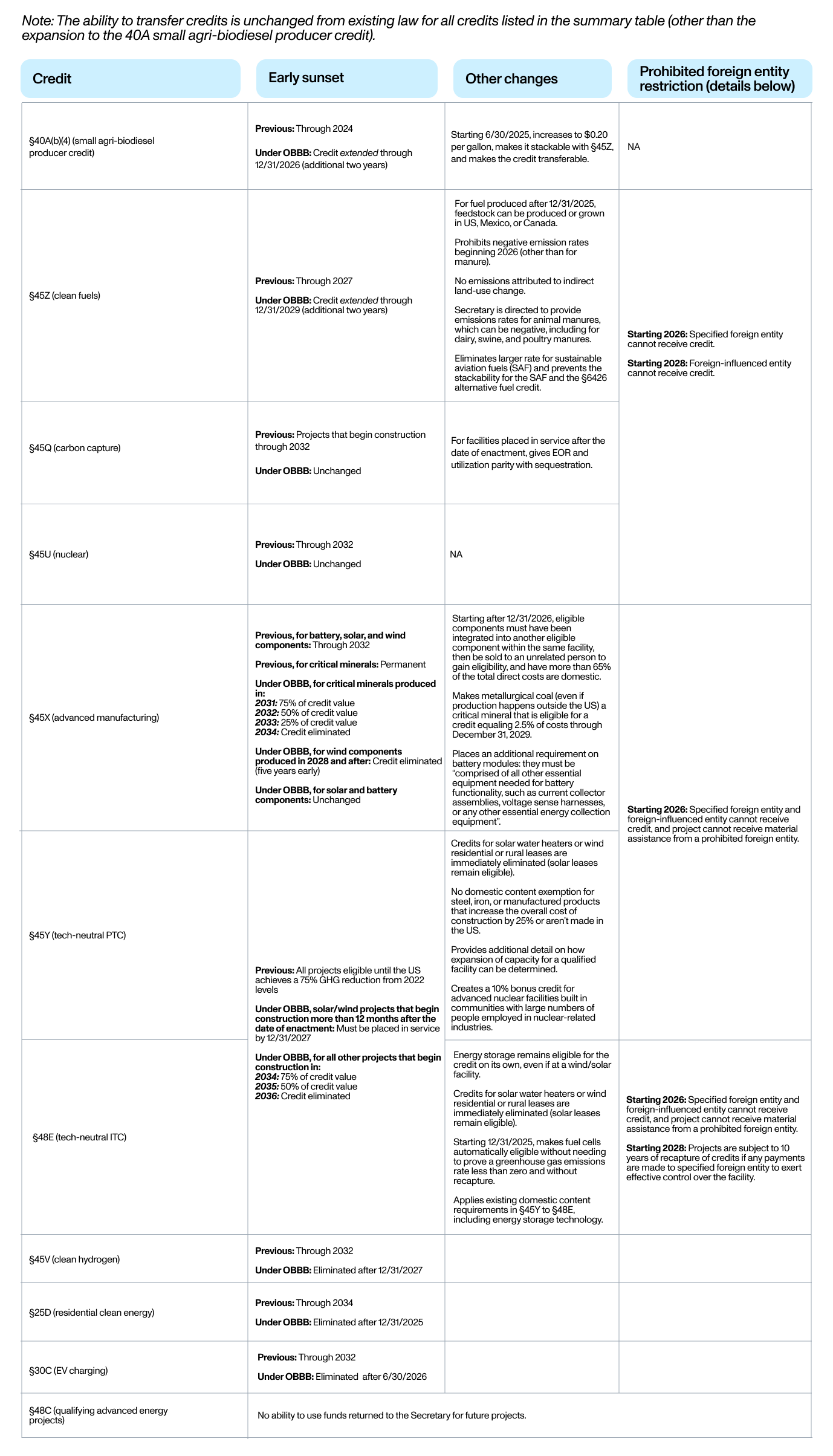

The One Big Beautiful Bill (OBBB) passed on July 4, 2025 accelerates the expiration date of several tax credits, including the technology-neutral tax credits.

Changes to specific energy and manufacturing tax credits under the OBBB

These changes are not retroactive; tech-neutral projects that began construction before July 4, 2025 or facilities that are eligible for the legacy §48 or §45 tax credits are not impacted.

The biggest changes affect solar and wind projects claiming the tech-neutral §45Y and §48E credits. To be eligible to claim the tax credit, solar and wind projects must be placed in service by December 31, 2027 to be eligible; however projects that begin construction by July 4, 2026 are not subject to the 2027 placed-in-service requirement.

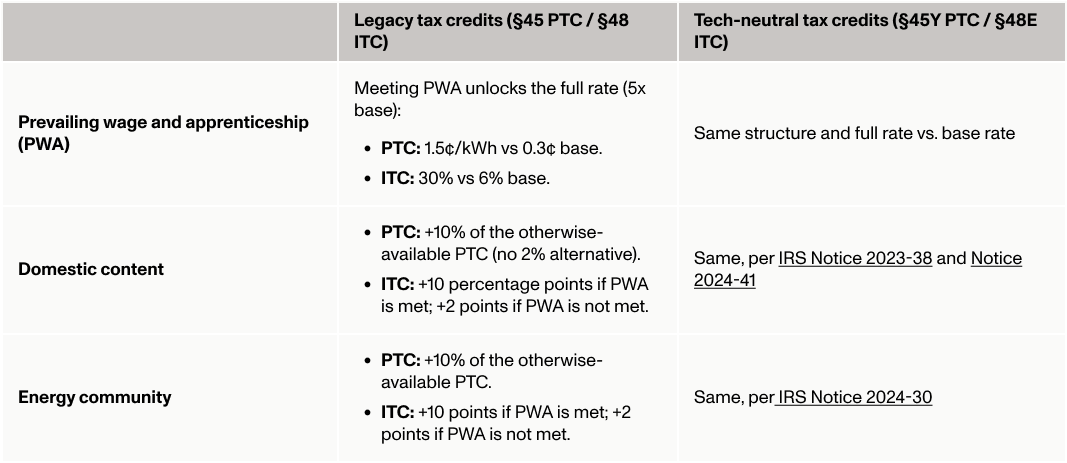

Both the legacy and tech-neutral regimes offer substantial bonuses for facilities that qualify for adders based on prevailing wage and apprenticeship (PWA), energy communities, or domestic content.

Bonus adders under the legacy and tech-neutral tax credit regimes

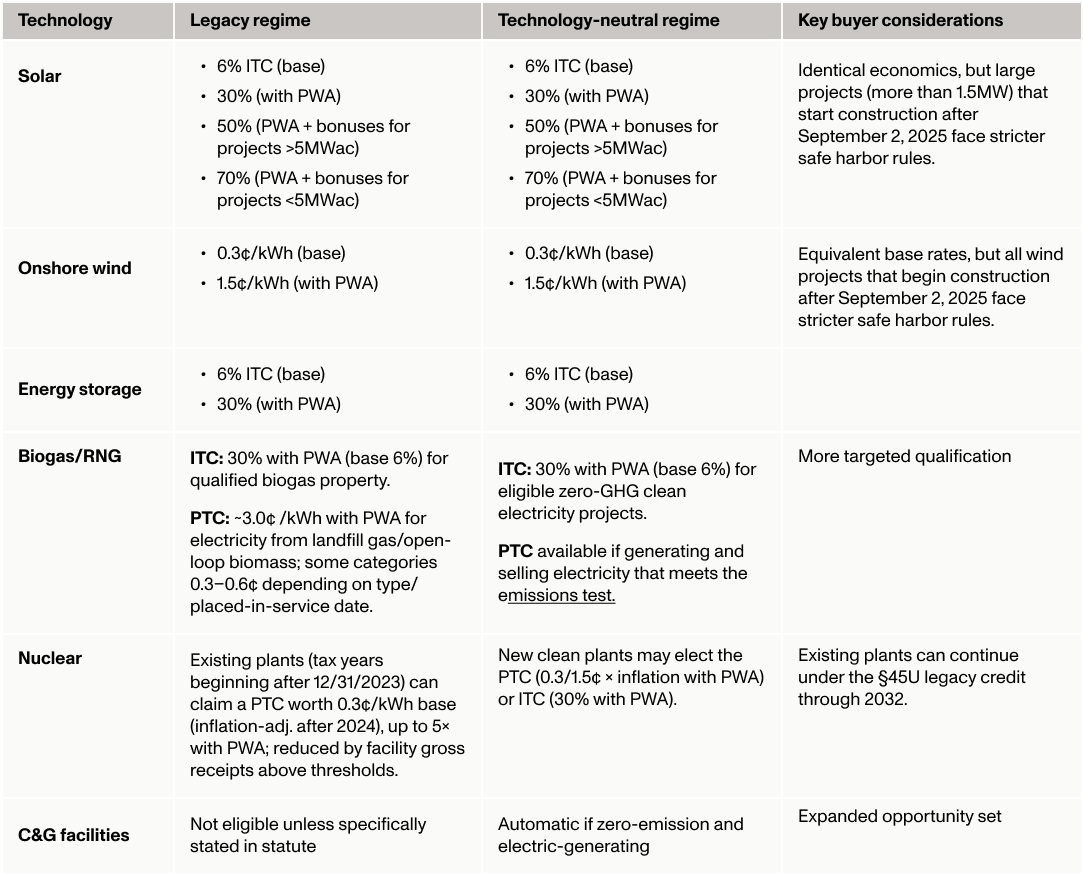

While tax credit values under the two regimes are similar, there are some key differences.

Credit value comparison

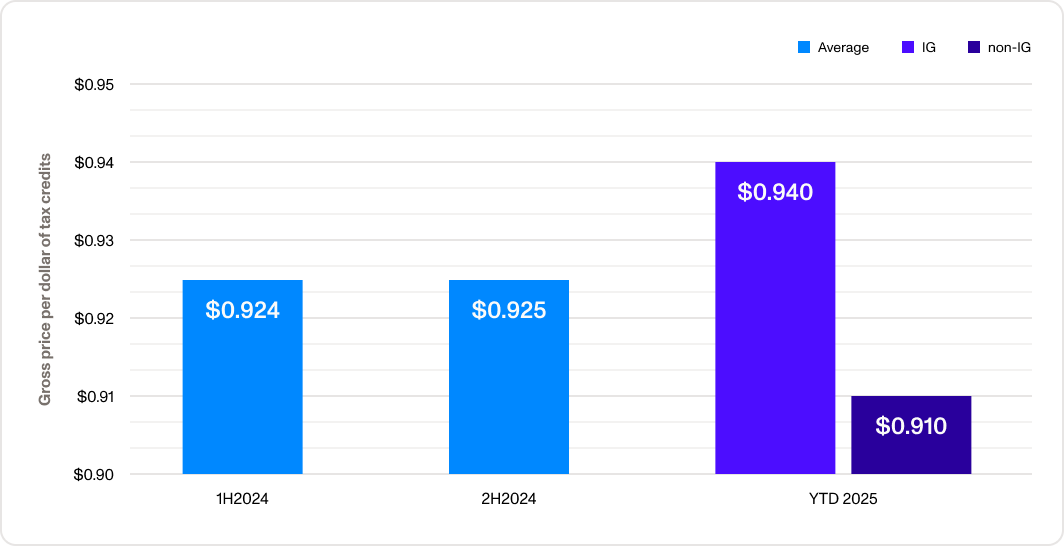

Crux has not observed a pricing differential between legacy and tech-neutral tax credits. As noted in our 2025 mid-year market intelligence report, the bigger difference in 1H2025 has been between investment-grade (IG) and non-IG sellers. We’ve historically seen that IG-rated sellers earn a price premium and that premium deals tend to move earlier in the market. Both of these themes were exaggerated in the first half of 2025.

That divergence is especially true for investment tax credits. For 2025, ITCs sold by IG sponsors transacted at an average premium of $0.03.

Average pricing, 2025 ITCs

Because buyers are typically indemnified by sellers for transfer risks, a seller’s ability to offer an IG indemnity is a premium product. Buyers prefer to transact with counterparties whose balance sheets can fully stand behind their tax credit transactions. Non-IG sellers typically obtain tax credit insurance, especially for ITC deals.

Due diligence is a key part of any tax credit transaction. Because buyers typically don’t purchase tax credits before the tax credits are generated, due diligence can occur upfront, before the tax credits are purchased.

Many elements of the diligence process will remain the same. For instance, buyers already request proper IRS registrations and transfer election statements, fair market value appraisals, and verification of PWA requirements and bonus adders.

Key considerations unique to technology-neutral credits include:

While legacy tax credits consider projects for specific types of technologies, the tech-neutral tax credits consider whether facilities generate electricity without producing GHG emissions. In implementing final tech-neutral guidance, the IRS affirmed that a category of electric-generating technologies is non-emitting by default. These technologies include:

Other technology types, such as clean fuels, may require different analytical frameworks for eligibility determination.

Ensuring that wind and solar projects meet new begin-construction requirements for the tax credit safe harbor will be critical. Buyers should ask sellers to furnish evidence showing their beginning-of-construction strategy and timing as part of the diligence process.

The OBBB added new Foreign Entity of Concern (FEOC) requirements, including new requirements related to “prohibited foreign entities”, “specified foreign entities”, and “foreign-influenced entities”. Starting in 2026, credits may be disallowed if the taxpayer is a specified foreign entity or foreign-influenced entity, if a certain percentage of payments related to the credited activity goes to a prohibited foreign entity (PFE), or if any taxpayer has contracts with a specified foreign entity that gives the entity “effective control” over the facility in question.

Go deeper: Download Crux’s prohibited foreign entity definitions explainer

While the US Department of the Treasury is expected to issue further guidance on FEOC, many of the requirements already exist in the statute. Norton Rose Fulbright breaks FEOC compliance into three steps:

Material assistance cost ratio: As noted in an excerpt from the New York University Tax Law Center in our mid-year market intelligence report, clean energy developers beginning construction on qualified facilities/energy storage technology after 2025 and selling eligible components in the taxable year after enactment will need to ensure that no more than a particular percentage (the “cost ratio”) of their project is sourced from producers that are not PFEs.

The non-PFE content requirement increases each year depending on type of facility or eligible component.

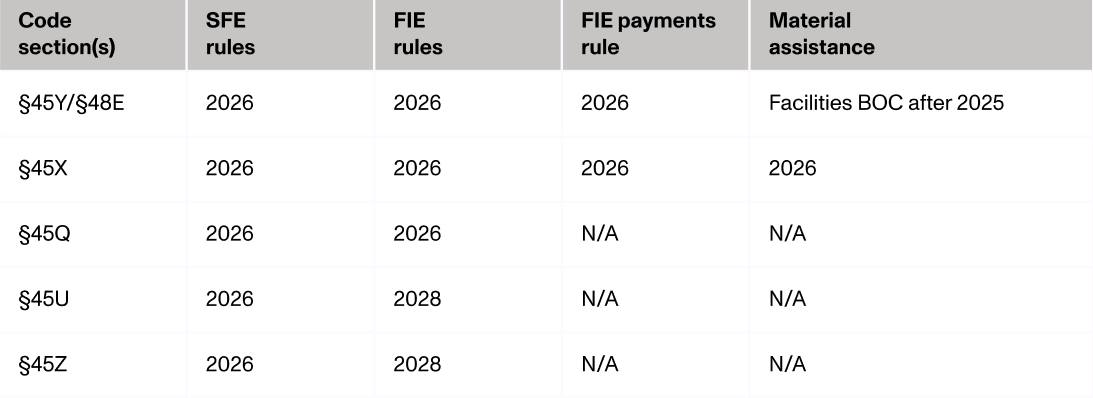

Key phase-in dates for PFE rules applying to §§ 45Y, 48E, 45X, 45Q, 45U, and 45Z

FEOC restrictions at the taxpayer level: Starting in 2026, developers who are deemed a specified foreign entity (SFE) or foreign-influenced entity (FIE) will not be eligible to claim tax credits for tax years beginning after July 4, 2025.

Effective control: Developers must ensure that they do not have contracts or technology licenses with any SFE that would give the SFE “effective control” over the facility or eligible component production. Problematic contract provisions include, among other items, rights to dictate production levels, control facility output, or any licensing arrangements with respect to the facility or production of eligible components entered into after July 4, 2025.

It’s not clear currently whether these rules apply to contracts that were issued or signed before the passage of the OBBB on July 4, 2025. It is important to note that developers claiming credits under §§ 45Y, 48E, and 45X will be subject to the effective control rules beginning in taxable years 2026 regardless of when they commenced construction and regardless of whether they are in the middle of their credit period.

Further guidance from Treasury is expected to clarify what constitutes a contract with effective control. Norton Rose Fulbright provides a list of provisions developers should avoid in contracts with counterparties that could be SFEs in the meantime.

In short, no. Both the legacy and tech-neutral tax credit regimes utilize Section 6418 transfer provisions, creating a consistent process regardless of credit regime.

Under Section 6418, enacted in 2022, eligible taxpayers can transfer specified tax credits — including both legacy PTCs/ITCs and tech-neutral tax credits — to unrelated parties in exchange for cash consideration. The transfer process requires the seller to register with the IRS, involves a one-time transfer election that must be made by the seller’s tax return due date, and allows credits to be utilized dollar-for-dollar as general business credits (Form 3800) against the buyer’s federal tax liability.

The fundamental transfer mechanics — including registration requirements, transfer documentation, timing rules, and buyer eligibility standards — remain substantially the same between regimes. However, buyers should anticipate enhanced due diligence requirements for tech-neutral tax credits related to technology qualification and emissions verification, where that is relevant, as well as potentially different insurance and risk assessment as new regulatory requirements such as FEOC and the new IRS beginning-of-construction rules come into effect.

Read Crux’s guide to essential tax credit transfer steps

Recapture occurs when all or a portion of a facility that has claimed investment tax credits is removed from service. In this case, the original claimant must “pay back” a portion of the credits to the IRS. This typically happens due to operational failures, ownership changes, or compliance violations during the recapture period or, in fewer instances, weather-related events. While recapture is extremely rare — according to Crux’s research, recapture has historically occurred in fewer than 0.5% of tax equity or tax credit transactions — it’s important to understand the risk.

For both legacy and tech-neutral credits, the recapture period generally extends for five years from the project’s placed-in-service date, during which time the project must continue to meet all applicable requirements to avoid triggering recapture obligations.

While both regimes maintain similar recapture timing and calculation structures, tech-neutral credits introduce a new circumstance for recapture on C&G facilities. If a C&G facility that initially qualified based on zero emissions subsequently fails to maintain that performance standard, recapture could occur. As with all recapture scenarios, recapture is borne by the seller, not the tax credit buyer, though buyers typically receives protection for recaptures from the seller through the indemnity.

These rules generally won’t come to bear on non-C&G facilities, such as solar, wind, and energy storage. IRS guidance has stated that these facilities are presumed to be zero-emission facilities. C&G facilities, such as landfill gas generators, will likely need to maintain documentation regarding fuel intake and emissions.

Basic insurance requirements remain similar between the two regimes. However, tech-neutral credits introduce ongoing performance and compliance considerations for C&G facilities through the credit period. Buyers may want to consider insuring against new risks, such as:

Insurance carriers are still developing specific policy language to address tech-neutral risks, including FEOC, so buyers should expect some variation in coverage terms and exclusions as the market matures. They could also see premium variations based on technology maturity and market experience.

A large volume of clean energy and manufacturing projects are safe harbored into the legacy §45 / §48 structure, and they will constitute a large portion of tax credits on the market into the foreseeable future. Today, 60% of the credits transacting on Crux’s platform are legacy tax credits. Over time, however, new facilities — especially storage facilities — claiming the tech-neutral tax credit will constitute a rising portion of the market.

The switch to the technology-neutral tax credit regime opens the doors for a larger, more diverse supply of credits for tax credit buyers to choose from, increasing liquidity in the market. Buyers who understand the two regimes will be in the best position to capitalize on both the established legacy credit market and the expanding tech-neutral opportunity set.

To help corporate tax teams navigate the rapidly evolving tax landscape, Crux has significantly expanded our product offerings to provide full-service transactional support across transferable tax credits, tax equity, and other tax-advantaged investment strategies. With support across platform tax credit transactions, full-service execution, and syndicated tax credit deals, Crux helps tax credit buyers identify the right opportunities, manage the due diligence process, and complete efficient transactions.

Get in touch to learn more about how Crux can help.

Disclaimer

This post is for informational purposes only and should not be construed as tax, legal, policy, or accounting advice. Crux does not provide tax, legal, or policy advice. You should consult with your own tax, legal, policy, and accounting advisors before engaging in any transaction or strategy discussed herein.