Tax credit transferability has made it easier than ever for developers and manufacturers to turn clean energy incentives into cash by selling investment tax credits (ITCs) and production tax credits (PTCs) directly to third-party buyers. As the market matures, so too does standardization around how to manage transaction risks.

Risk mitigation is critical in a new market in which many buyers, from regional banks to corporate tax departments, may not be willing to proceed without added protection. Tax credit insurance has emerged as a key vehicle to manage risk. Crux’s data shows that 60–70% of ITC deals included insurance in the first half of 2025.

This article breaks down what tax credit insurance covers, how it works, and what developers and manufacturers need to know to obtain a strong policy.

Go deeper: Download A Guide to the Tax Credit Insurance Market

Tax credit insurance is a third-party policy designed to protect buyers from financial loss if the Internal Revenue Service (IRS) disallows, reduces, or recaptures transferred clean energy tax credits. While buyers are the insured party, sellers typically procure and pay for the policy, often rolling the cost into the deal price.

Demand for insurance is growing quickly: some buyers seeking added certainty may want added protection from tax risk that insurance can offer, while sellers may rely on it to access a broader pool of counterparties and reduce their potential exposure under indemnities.

Clean energy tax credit transactions carry several types of risk that buyers expect sellers to address, especially when the seller does not have investment-grade credit. The vast majority of insured deals involve non-investment-grade sellers; insurance often acts as a substitute for credit quality to help boost buyer confidence.

Here are the main risks that policies typically address:

If a project fails to meet IRS criteria (e.g., placed-in-service requirements), the credit can be disallowed.

For ITCs, if the tax basis is overstated (often because the project was valued above its actual cost via appraisal), the IRS may reduce the credit amount. This can also lead to excessive credit transfer, where more credit is sold than was actually earned, potentially triggering clawbacks for the buyer.

If, within five years after it is placed in service, an ITC project is sold, taken offline, or damaged without being rebuilt, the IRS can take back, or recapture, the credit. However, this is very rare: Crux research shows that recapture has occurred in just 0.5% of deals, and 80% of advisors have never seen it happen.

Recapture risk only applies to ITCs; PTCs cannot be recaptured because the credit is only generated after the electricity or manufactured component is produced.

If a project fails to meet bonus credit criteria (e.g., prevailing wage and apprenticeship, domestic content, or energy community), the IRS may reduce the total credit amount.

If a project is not placed in service as planned, the buyer may not receive the credits in the expected timeframe or full amount.

Missteps such as circular cash flows, incorrect entity structuring, or payment documentation errors can invalidate an otherwise valid transfer.

Each of these risks can delay a transaction, trigger buyer pushback, or lead to post-closing disputes if not properly addressed. That’s why buyers expect sellers to stand behind their credits through strong representations and indemnities, and why they increasingly seek added protection through insurance.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

While policies are tailored to each deal, the covered risks often differ slightly between ITC and PTC transactions:

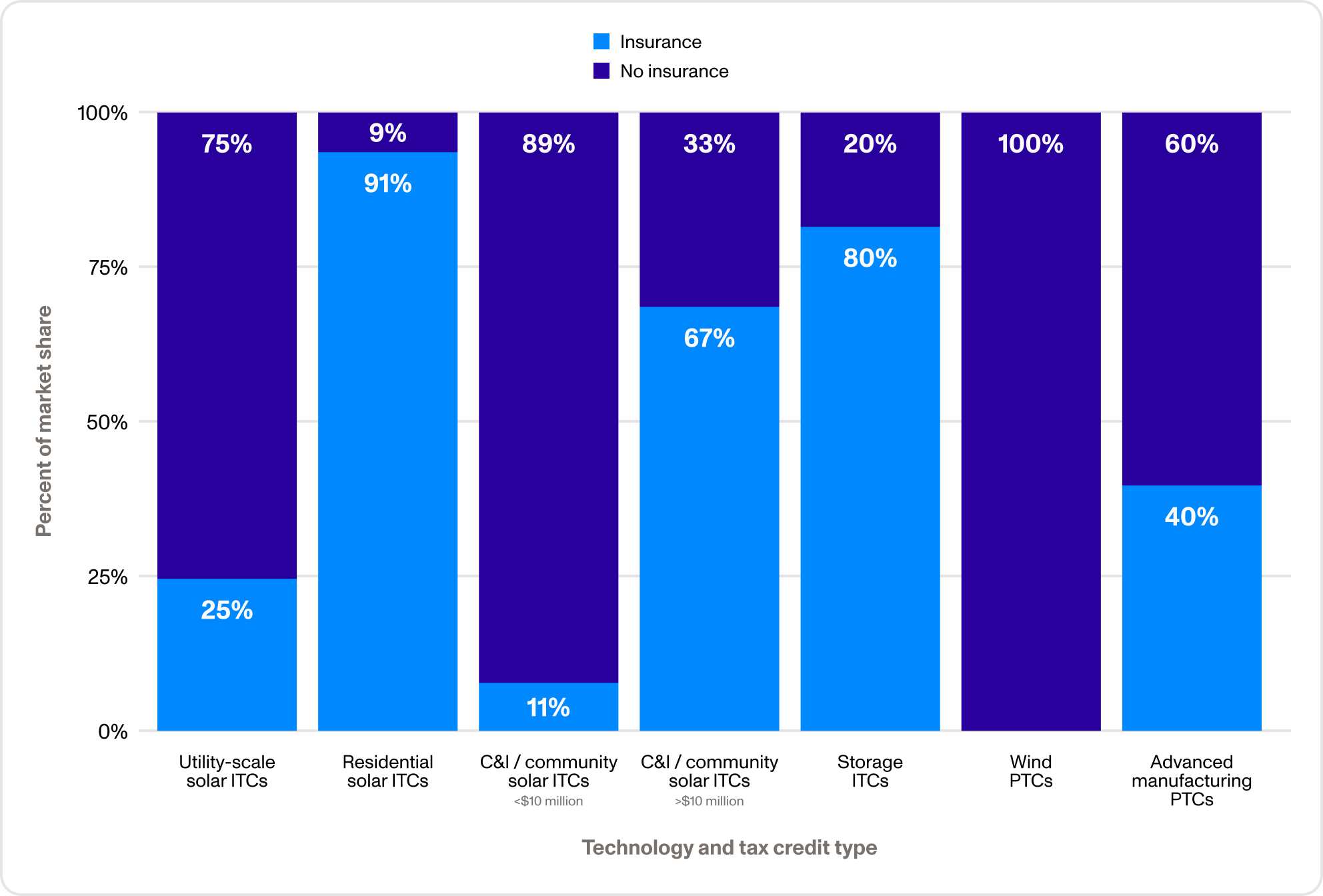

Crux data reveals a significant variation in insurance adoption depending on the project profile and credit type. In 1H2025, about 80% of storage ITC deals were insured, reflecting higher risk and merchant exposure. Residential solar ITCs were also frequently insured due to ongoing market volatility.

By contrast, insurance was far less common in utility-scale solar ITC deals (25% of deals) because a larger portion of these deals came from investment-grade sellers. Only 11% of sub-$10 million commercial and industrial (C&I)/community solar deals included coverage because the cost of insurance makes it uneconomical, and policies can be hard to find for deals of this size. However, 67% of C&I deals over $10 million were insured due to factors such as stronger buyer requirements and more favorable insurance economics.

In terms of overall ITC deal size, mid-sized ITC transactions ($10–150 million) are most often insured, balancing cost and coverage efficiency. Smaller deals typically fall below insurer minimums, while very large deals (≥$300 million) are more likely to be generated by investment-grade entities where buyers don’t need to rely on insurance.

Compared to ITCs, PTC insurance rates are typically lower because of the credit’s longer-term structure, more predictable risk profile, and fewer buyer requirements. PTCs also avoid certain ITC-specific risks such as recapture and basis risk, contributing to lower coverage needs. For example, wind PTCs are rarely insured given the credit’s maturity and wind’s operational stability, which reduces the commercial need for coverage. For advanced manufacturing PTC deals, insurance rates have declined as the credit matures, stabilizing at around 40%.

Percentage of deals with insurance by technology and credit type in 1H2025

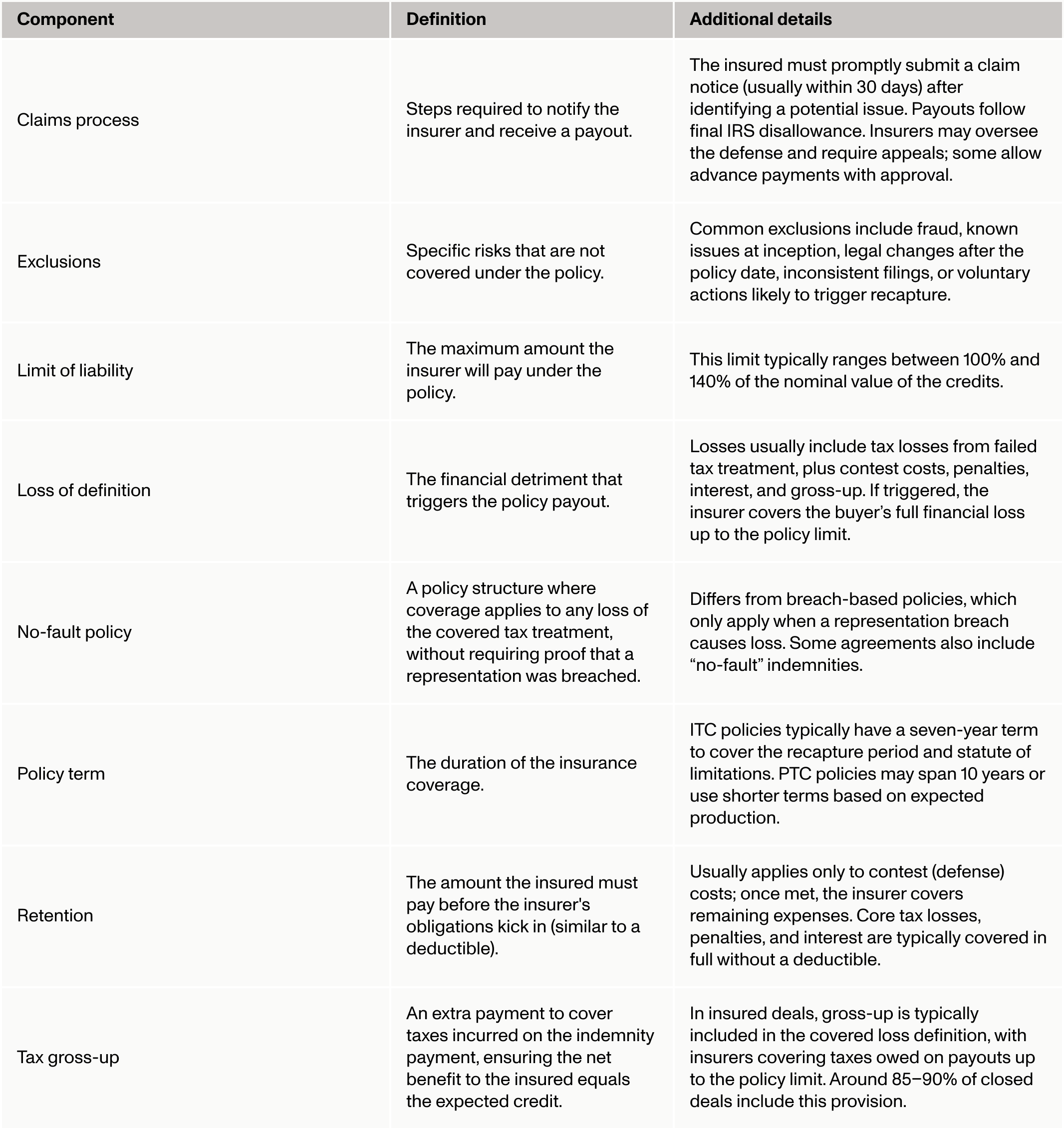

Tax credit insurance policies are built around a specific covered tax treatment — the tax position the insurer agrees to back. While each policy is bespoke, most include the following core components:

Looking for more clarification on policy language? See our tax credit insurance glossary for quick definitions of common terms.

Sellers are typically responsible for procuring tax credit insurance. Careful planning is vital to ensure the policy meets buyer expectations and minimizes costly surprises.

Here are four expert-sourced best practices for navigating the insurance procurement process:

Our survey of advisors shows that misalignment between the buyer and seller over the scope of the insurance policy is one of the top three causes of transaction delays or derailment. To avoid issues, confirm key coverage terms before or shortly after the term sheet stage. If you’re unsure where to begin, Crux’s partner network can connect you with experienced insurance brokers to help guide you through the process.

About 40% of advisors say due diligence misalignment negatively affects tax credit deals. Because insurers often request the same materials as buyers, any gaps can lead to narrower coverage, higher premiums, or binding delays, making it critical to align your diligence stack with insurer expectations. It’s also important to leave enough time for brokers and underwriters to complete their review — rushed timelines can stall closings or limit coverage.

If your project involves an ITC basis step-up, anticipate rigorous diligence by the insurer. Be prepared for the insurer to cap the value of the step-up it is willing to insure, potentially requiring you to retain some risk. This includes working with your partner early to ensure materials are defensible and aligned with market norms.

While buyer legal counsel may avoid relying on seller legal opinions, Crux has found that the majority of insurers/insurance brokers (60%) will review seller counsel legal opinions and memos in depth. Ensure these documents are high quality and ready to expedite the underwriting process.

Tax credit insurance has become a standard part of transferable credit deals, especially for non-investment-grade sellers aiming to reach a broader buyer pool. When structured thoughtfully, insurance helps de-risk transactions, accelerate closings, and support scalable credit sales.

For deeper insights and data on tax credit insurance, download A Guide to the Tax Credit Insurance Market.