Transferability has made it easier for developers of all sizes to monetize their tax credits. For developers on the smaller end of the market who wouldn’t typically be able to access tax equity partnerships, selling tax credits makes it possible to recycle capital faster.

In our 2024 Transferable Tax Credit Market Intelligence Report, based on $25 billion in transaction data, Crux found that smaller tax credits — generally considered anything less than $10 million — receive two to three bids per listed credit, in line with larger deals. This is due in part to a more competitive market across all credit sizes.

Given increased competition, developers who are prepared to transact can set themselves up for a more successful, streamlined process. This article covers four elements that developers should consider as they prepare for their first transaction.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

While tax credit transfers are much simpler transactions than tax equity partnerships, they still require advisors and negotiation with buyers. Developers will need to align with buyers on key deal terms in the term sheet and tax credit transfer agreement (TCTA), for instance.

Having a transaction team in place — potentially including legal counsel, insurance brokers, and accountants — early can help streamline the transaction process. Crux’s referral network makes it easy for developers to connect with the right providers. Developers can also bring advisors and consultants into Crux’s data room, keeping everything in one location.

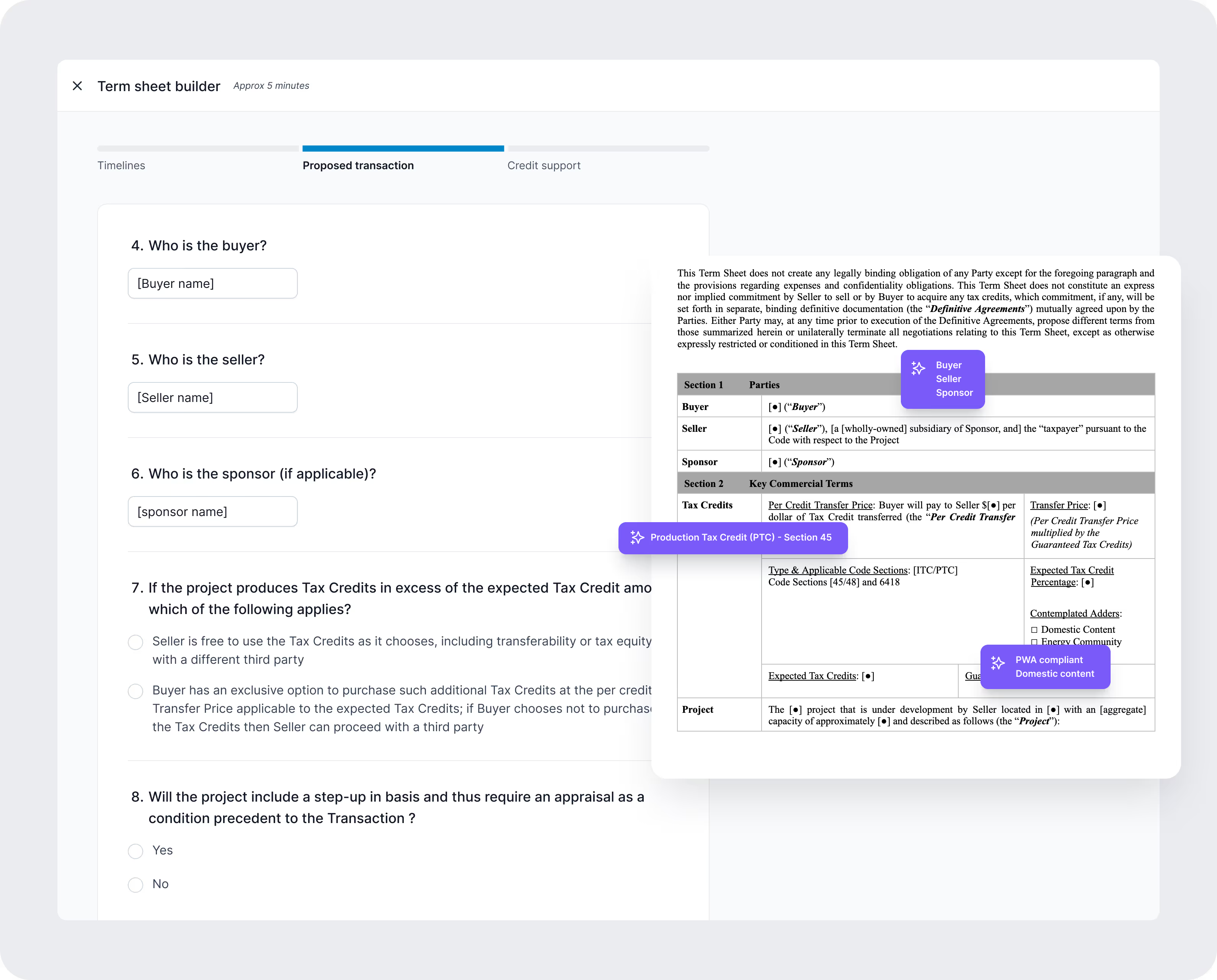

Market-standard documents such as Crux’s diligence checklist and Term Sheet Builder help developers understand what terms and diligence items buyers are looking for from the beginning of the transaction, reducing time and legal expenses. These tools are based on Crux’s market-leading data and input from leading law firms.

Crux’s Term Sheet Builder simplifies the process of aligning on key terms

For smaller credit deal sizes, insurance may be a negotiated point. Buyers and sellers will often negotiate not to include insurance on smaller credits, instead opting for other types of credit support, such as parent guarantees. Across all transaction sizes in 2024, more than half (55.3%) used a parent indemnity rather than full or partial insurance. Developers should be aware that credits with insurance often transact at higher prices, while credits without may be further discounted.

Pricing for insurance varies with the size of the credit and the specific project details. Credits above $10 million often see insurance premiums in the range of 1.5–3.0% of the deal total, while smaller credits see premiums in the range of 2.0–5.0%.

For a more detailed understanding of insurance pricing, developers should talk to an insurance provider. Crux can help provide referrals.

Cost-segregation reports are a standard part of diligencing investment tax credits (ITCs) to ensure the total eligible project costs. These reports evaluate a project’s ITC-eligible expenditures and the applicable depreciation periods for each asset or piece of property. Buyers view the cost-segregation report as a way to mitigate risk, reduce exposure to recapture, and substantiate the value of the credit.

Buyers will typically require a cost-segregation report to be prepared by a third party, such as an accounting firm familiar with Internal Revenue Service (IRS) guidance regarding eligible costs. Credits less than $1 million may be able to use an internally prepared cost segregation.

Cost-segregation reports are a big part of increasing transaction readiness — according to Crux data, 85% of buyer advisors said they review cost-segregation reports in depth. Having this report prepared early can have many positive knock-on effects for the transaction:

To obtain a cost-segregation report, developers should engage a third-party accounting firm and collect documentation such as engineering plans, lists of major equipment, a cost schedule and supporting documentation of those costs, and a project timeline to aid in preparation of the cost segregation.

The diligence process typically includes a legal memo covering the project’s eligibility for the credit. A buyer might require it, or it could be necessary to get an insurance policy. The memo will typically cover:

The memo will be an additional third-party cost. Through Crux Legal Select, developers can connect with law firms to assist with transaction materials such as legal memos.

By increasing their readiness to transact, developers with smaller credit sizes can take advantage of a competitive tax credit market. Crux’s market-standard documentation, tools, and expert team can help developers throughout the process. Get in touch to learn more about how Crux can support you.