US power demand is rising for the first time in 20 years, and critical minerals are the foundation stones of much-needed new power generation. Today, however, the US depends largely on critical minerals extracted and processed in foreign countries, especially China.

Recognizing the economic and national security benefits of stronger supply chains for critical minerals, Congress made critical minerals eligible for the §45X advanced manufacturing production tax credit (PTC).

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

The Energy Act of 2020 directed the US Geological Service (USGS) to produce and update a list of critical minerals based on three criteria:

The USGS updated its list of critical minerals in 2022 and released an updated list of these critical minerals in November 2025. The new list covers 60 minerals, including many that are foundational in clean energy components. It's important to note that, although the USGS updated its list of critical minerals to include copper, uranium, phosphate, and others, the list of critical minerals eligible for the §45X tax credit is established in statute and is not subject to change based on USGS amendments to the critical mineral list.

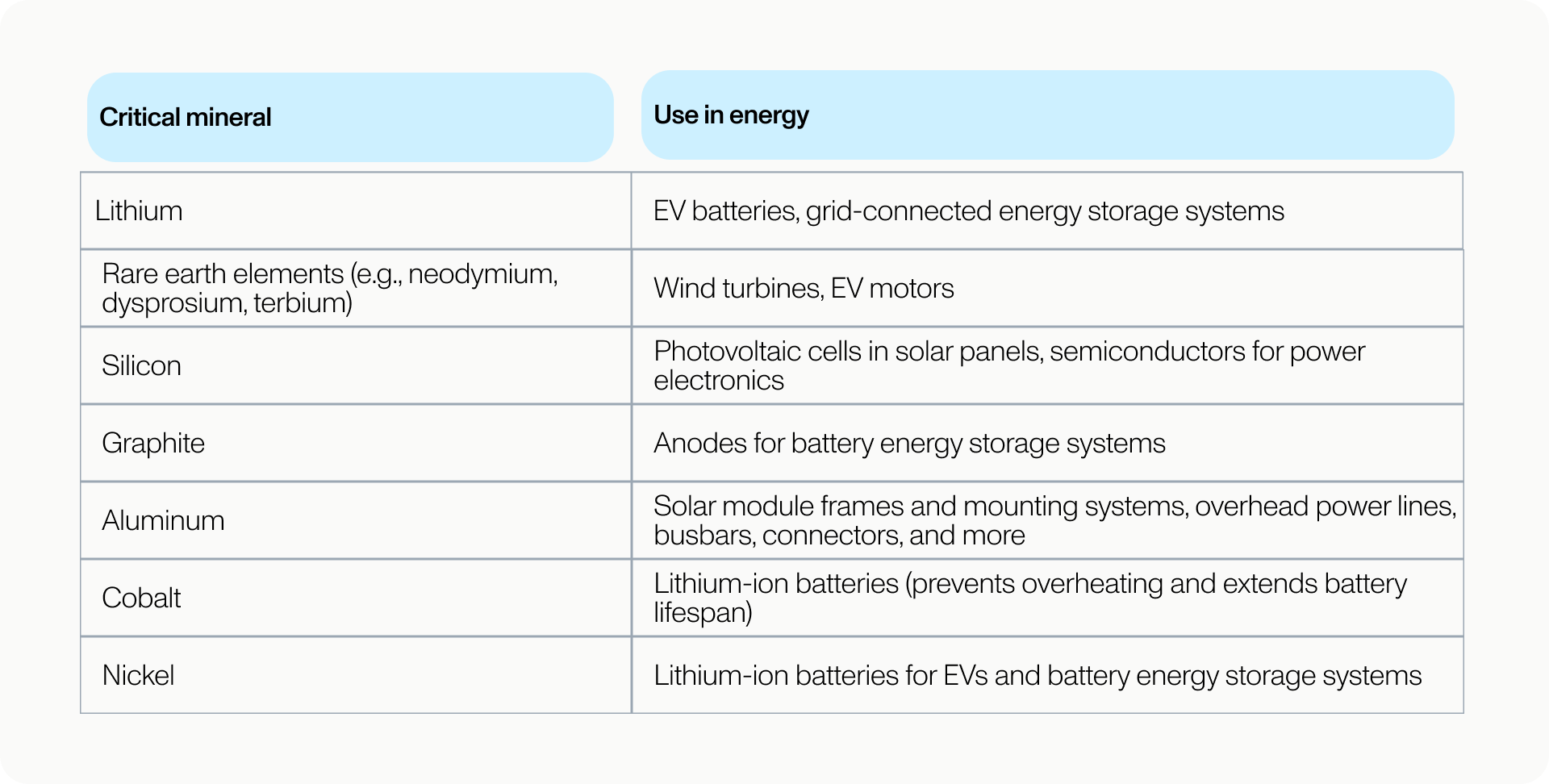

Select critical minerals and their use in energy

Critical minerals play a central role in clean energy manufacturing and in the production of many high-tech goods. In a report published in January 2025, the USGS noted that the US is 100% reliant on imports for 12 of the 50 critical minerals. China plays an outsized role in global supply and processing capacity for critical minerals. For rare earths, a subset of critical minerals that are specifically valuable for their conductive and magnetic properties, China controls 60% of global production and 90% of refining and processing capacity.

Reshoring supply chains and increasing domestic production of critical minerals is a core focus of the §45X tax credit.

The §45X advanced manufacturing PTC is a tool to accelerate necessary investments in extracting and processing America’s critical minerals. The credits are transferable, which allows smaller companies spearheading new mineral extraction and refining technologies to unlock needed capital for innovation and expansion by selling the credits to third parties.

To ensure critical minerals can be used in clean energy technologies, they must meet specific purity thresholds to be eligible for §45X tax credits, typically 99% by mass, and sometimes higher. For example, aluminum must achieve a minimum purity of 99.9% aluminum by mass. Those claiming the credit must produce a certificate of analysis confirming the mineral’s purity.

The statute sets the value of the critical minerals PTC as 10.0% (or 2.5% in the case of metallurgical coal) of the production cost of a domestically produced or processed critical mineral sold to a third party in the US. In addition to the direct costs of production, there are several important rules regarding how companies can assess the value of their tax credits.

In draft guidance published in November 2023, the Internal Revenue Service (IRS) prohibited including mineral acquisition costs in calculating the value of the §45X critical mineral tax credit. The final guidance released in October 2024 allows the inclusion of certain material costs, including extraction costs, for applicable critical minerals and electrode active materials. This change addresses concerns raised by stakeholders about the exclusion of material costs, acknowledging their contribution to value-added production.

The final IRS guidance permits companies to include indirect costs according to §263A in the calculation of the §45X credit value. Indirect business costs are company expenses not directly related to the extraction or processing of critical minerals. They include employee benefits and payroll costs, depreciation or amortization of equipment, and taxes and insurance related to production activities.

These credits are alternatively eligible for elective pay (often referred to as “direct pay”), where the project can receive the full value of its tax credits as a refund from the IRS. Payments from transfer deals can generally be received much sooner than a refund, which comes following a company’s annual tax filing.

Many manufacturers and miners are choosing to sell their tax credits to a private buyer instead of waiting for the IRS to process their filings. The discounts Crux has observed on all §45X advanced manufacturing production tax credit deals generate comparable or better economic returns to the seller.

The critical minerals PTC is available for critical minerals produced through 2033, although the credit value steps down gradually starting after 2030:

The credit is scheduled to be eliminated for critical minerals produced in 2034 and later.

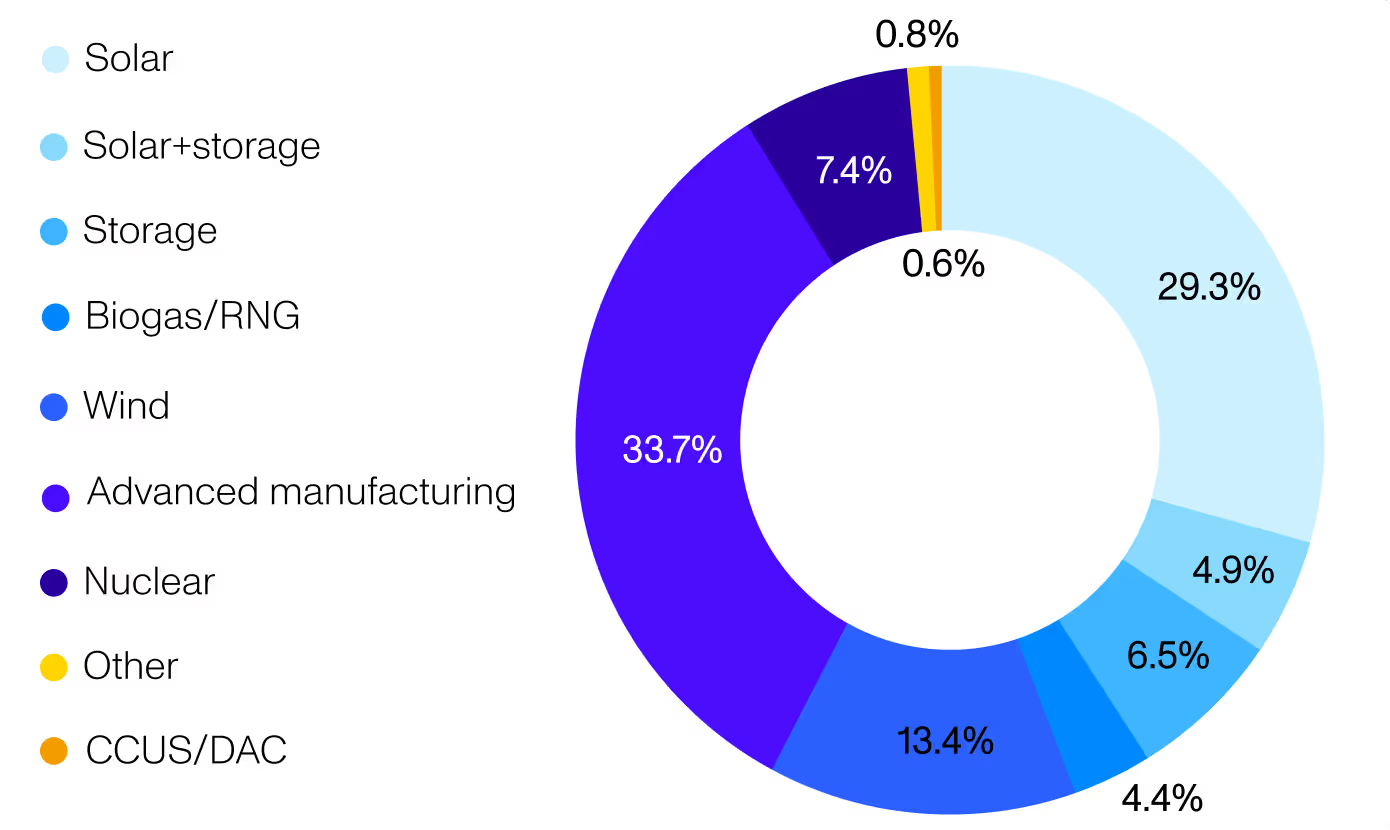

Advanced manufacturing PTCs, including critical minerals tax credits, began transacting in 2023, and the IRS finalized eligibility and calculation guidance in October 2024. Already, demand for §45X advanced manufacturing production tax credits is robust. According to the 2024 Transferable Tax Credit Market Intelligence Report, advanced manufacturing credits — including critical minerals tax credits — made up the single largest share of the tax credit market, at 33.7%.

Market composition, 2024 full year (by dollar value, 2024 tax credits)

Deals were most commonly transacted as spot or short-term strip purchases (usually two to three years), and transactions ranged in value from approximately $20 million to more than $1 billion.

Why are these credits so popular? They have several benefits from the tax credit buyer perspective:

Demand for advanced manufacturing PTCs rose throughout 2024 and has remained strong in early 2025. About 35% of commercial bids placed on Crux in the first quarter of 2025 were for advanced manufacturing tax credits. Crux has observed that demand consistently outstrips supply for these credits.

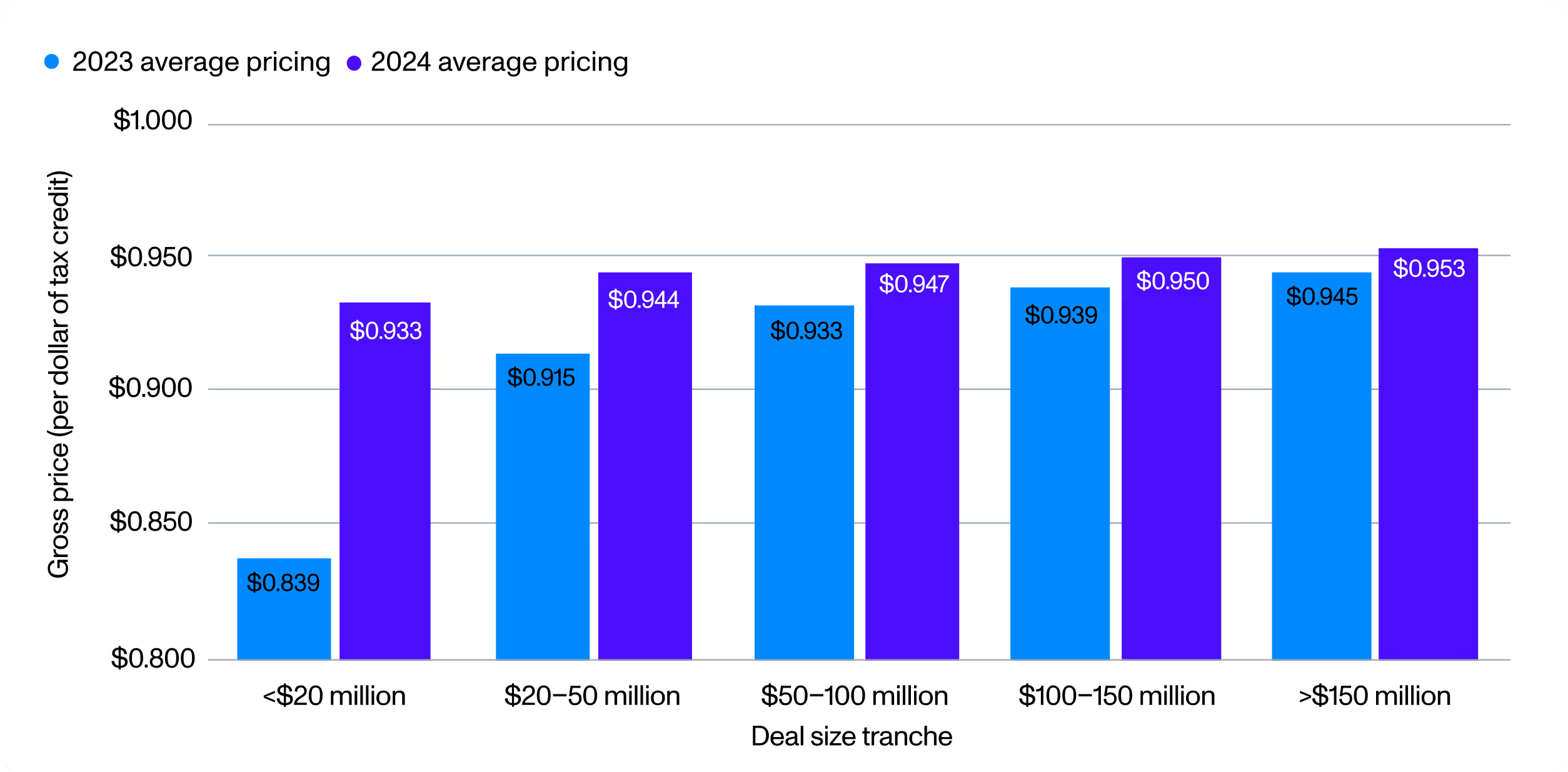

Pricing for these credits is consistently in the range of $0.92–0.96 at the highest end of the deal curve.

Advanced manufacturing PTC pricing by deal size tranche, year over year

According to our 2024 Market Intelligence Report, insurance is generally available for all §45X advanced manufacturing PTC deals, though the prevalence of insurance coverage generally declined over the course of 2024. About 23% of advanced manufacturing production tax credits sold in 2024 included insurance coverage; the remaining 77% of tax credit deals were indemnified by the seller parent company.

Larger deals are generally more likely to include parent indemnification, as a larger entity may have sufficient balance sheet capital to assure a buyer that it can provide a reliable indemnity. Buyers have become increasingly comfortable with accepting parent indemnities for these deals. In 2023, approximately 45% of §45X advanced manufacturing production tax credit sales included insurance coverage and 55% were covered by a parent indemnification with no insurance.

The amount of insurance coverage is typically reported as a percentage of the notional deal value — coverage over 100% reflects a gross up, typically covering penalties, interest, and taxes. Coverage below 100% can provide credit support for the seller’s parent indemnities. Typical coverage levels for §45X advanced manufacturing PTC transactions were around 120%.

Crux expects demand for all §45X credits, including critical minerals credits, to remain high in 2025. Tax credit buyers who act earlier in the year could take advantage of less competition and possible pricing discounts.

Get in touch with us to learn more about buying tax credits on the Crux platform.