Understanding how recapture risk could affect the value and validity of an acquired clean energy tax credit is essential for any buyer or investor building a disciplined approach to tax credit transactions.

This installment of Crux’s series on underwriting risks discusses recapture risk: what it is, how and when it can be triggered, and how tax credit buyers and investors can apply standardized due diligence to mitigate risk and transact with confidence.

Key takeaways

Investment tax credits (ITCs), including both legacy credits under §48 and tech-neutral credits under §48E, are subject to a five-year recapture period if the facility earning the ITC ceases to be “investment credit property”. If, within five years of being placed in service, the underlying property ceases to be used for its qualifying purpose (such as generating electricity), the Internal Revenue Service (IRS) can “recapture” a portion of the credit. In the context of a tax credit transfer, the IRS claws the tax credit value back from the taxpayer who claimed it — in this case, the tax credit buyer or investor — by increasing their taxes to offset the claimed tax credit.

To trigger recapture, an ITC-eligible property must experience a disqualifying change during the five-year recapture period. Potential triggers include:

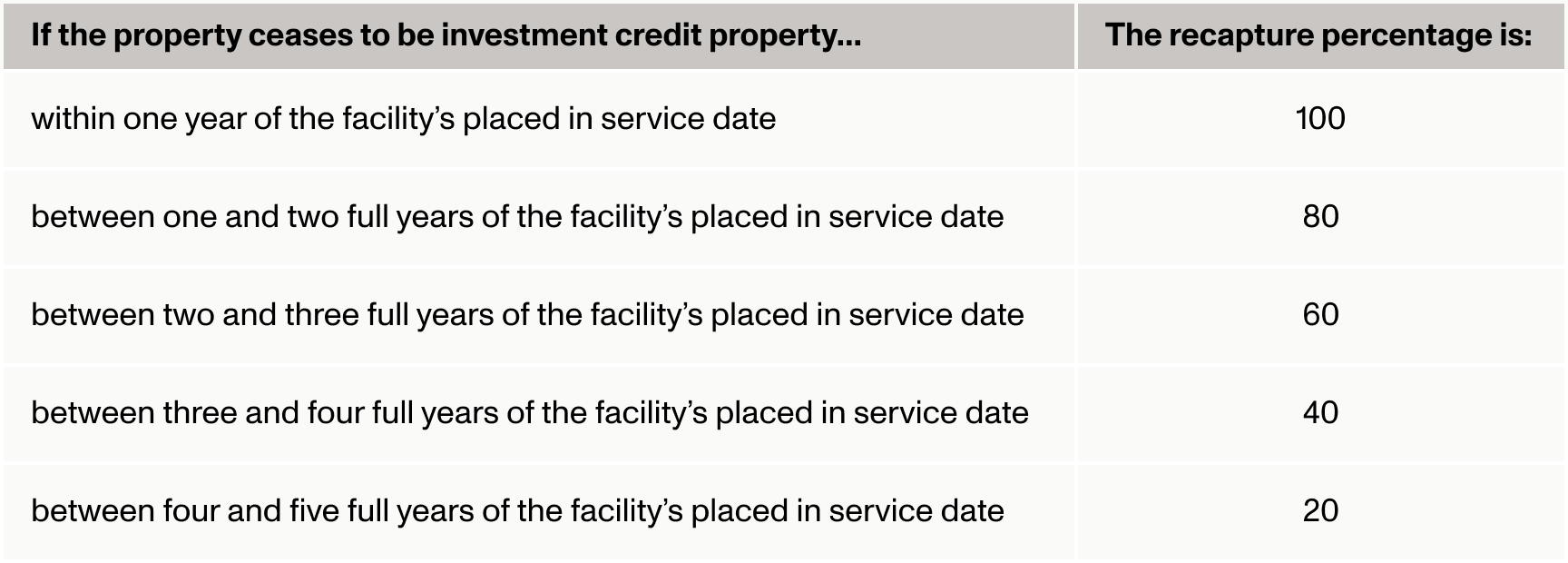

The amount of the original tax credit eligible for recapture declines by 20% each full year following the property’s placed-in-service date. If the eligible property experiences a disqualifying change between one full year and five full years following its placed in service date, the IRS could initiate a partial recapture of the tax credit based on the timeline shown in the table below.

Recapture percentage timeline

The One Big Beautiful Bill (OBBB) introduced additional recapture rules for the tech-neutral investment tax credits (§48E) if a project makes certain payments to companies deemed prohibited foreign entities (PFEs). For §48E ITCs claimed in tax years beginning after July 4, 2027 (i.e., 2028 for calendar-year taxpayers), the IRS may claw back 100% of the credit if the project makes effective control payments to a PFE within 10 years of being placed in service.

The IRS is expected to release further guidance detailing effective control payments and PFE definitions this year; clarity from this guidance will help market participants and insurers fully incorporate this risk into standard underwriting practices.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

Liability for recapture often sits with the taxpayer that claims the tax credit, regardless of whether they own or operate the credit generating facility. As an example, say that a buyer purchases a tax credit from a solar developer. A hail storm critically damages that developer’s solar project, stopping it from generating electricity. As a result, the solar project ceases to qualify as an investment credit property. In this scenario, the tax credit buyer, not the developer, bears the increased tax liability recapturing the tax credit. That’s why contractual protections such as indemnities and tax credit insurance are critical to mitigating recapture risk (more below).

There are exceptions to this rule. For example, in the context of a credit that has been transferred, if a partner in the seller entity sells or gives up their ownership stake during the recapture period, that departing partner bears the recapture liability, not the tax credit buyer.

Recapture is statistically rare. Crux research shows that recapture has occurred in just 0.5% of deals. Recapture events do not always constitute full recapture, some events may only constitute partial recapture — for instance, some equipment is damaged in a weather event but the facility is not destroyed entirely.

Despite its low incidence, recapture risk warrants a clear mitigation strategy. Buyers and investors typically address this risk through a combination of contractual mechanisms such as indemnities and insurance and thorough due diligence.

Before transacting, buyers and their advisors should evaluate factors that could affect the project's ability to remain in service through the recapture period. Key areas of focus include:

Buyers, investors, and their advisors should analyze the project's debt structure, lender covenants, and overall capitalization to assess the risk of a forced disposition. A loan default or foreclosure, for example, could result in a change of ownership that triggers recapture.

Notably, buyers, investors, and their advisors should identify whether forbearance agreements are in place that would prevent a lender from foreclosing directly on the energy property during the recapture period. In many transactions, buyers require the seller to negotiate agreements with their lenders not to pursue a foreclosure that would result in an ITC recapture, reducing recapture risk significantly. Credits sourced from projects financed through tax equity flip structures often already have these protections in place, as tax equity investors often negotiate lender forbearance agreements to protect their credit allocation.

Buyers, investors, and their advisors should also review the terms of the project's property and casualty insurance to ensure that it is sufficient to cover appropriate losses, including a potential recapture of the ITC stemming from exposure to severe weather events such as hurricanes, wildfires, flooding, or seismic activity. As noted in Crux’s whitepaper on risk mitigation, recapture events have been triggered by weather damage.

Buyers and their advisors should consider the financial health, operating history, and creditworthiness of the project operator and sponsor. A well-capitalized sponsor with a track record of operating similar projects may be less likely to voluntarily dispose of or abandon the asset during the recapture period, and a creditworthy seller is more likely to be able to fulfill indemnity obligations if a recapture event does occur.

Once a buyer or investor has assessed the project's risk profile, they have several contractual and insurance mechanisms available to mitigate recapture risk exposure:

Buyers, investors, and their respective advisors should negotiate for clear indemnity provisions covering recapture events. In direct transfers, buyers often require sellers to fully indemnify them for any recapture liability, including associated penalties and interest, regardless of fault. Where the seller is a project-level entity with limited creditworthiness, buyers may also require a parent guarantee from the project sponsor.

Tax equity investors should similarly ensure that the partnership agreement includes indemnification from the developer or sponsor for recapture events, particularly those arising from voluntary dispositions or changes in use that the investor did not consent to.

Many buyers and investors procure tax credit insurance policies that cover recapture risk under certain circumstances. Insurance provides a backstop if a seller's indemnity proves insufficient.

Tax equity investors typically benefit from built-in governance mechanisms, including consent rights over asset sales and change-of-control provisions, that reduce the likelihood of a surprise recapture event. Direct transfer buyers should negotiate ongoing reporting covenants that require the seller to notify them of material events during the recapture period, including any change in ownership, use, or physical condition of the property.

Regardless of structure, both buyers and investors benefit from clear post-execution communication channels that surface potential recapture triggers as they arise.

Taken together, thorough due diligence and adequate risk management mechanisms ensure that even in the unlikely event of a recapture trigger, buyers and investors have clear paths to recover their economic position.

Recapture risk is inherent in every ITC transaction, but the market has developed well-established tools — including robust indemnity provisions, tax credit insurance, and structured reporting covenants — to help buyers and investors manage it effectively.

Crux's team of finance, tax, and energy experts guides buyers and investors through the diligence process, helping them understand what is standard for the market in terms of risk and pricing and connecting them with trusted legal, accounting, and insurance advisors when needed. Our platform features a curated selection of pre-vetted credits from leading developers and manufacturers, supported by industry-specific diligence workflows validated by 40+ top-tier legal and accounting firms.

Contact us to learn more about how Crux can help you find and execute a tax credit transaction that meets your tax-planning objectives.