Transferable tax credits have significantly broadened access to clean energy finance. By allowing tax credits to be bought and sold for cash, rather than monetized solely through complex tax equity partnerships, transferable tax credits open the door to a broader range of corporate tax credit buyers and introduce greater liquidity and flexibility to project financing.

While transferable tax credit deals are less complex than tax equity partnerships, they do carry transaction risks. To ensure smooth transactions, corporate tax teams need a clear understanding of the diligence required to keep deals on track and the mechanisms available to protect their investments.

More than 70% of legal, tax, and financial advisors and insurers believe buyer education is the most important driver of a smooth tax credit transaction, reinforcing the need for internal preparedness. The more corporate tax teams understand the risk landscape, the faster they can close transactions.

This guide outlines the most common tax credit transaction risks buyers face and the practical steps used to mitigate them.

In the early days of the transferable tax credit market, buyer diligence focused primarily on project eligibility and price. But as the market has matured and participation has broadened, corporate tax teams are applying more structured diligence to ensure transactions close smoothly and stand up over time.

Several trends are shaping how buyers approach tax credit transactions today:

Leading corporate tax teams have responded to these trends by treating risk management as a core competency rather than a transactional hurdle. By standardizing their approach to diligence — across documentation, compliance review, and counterparty vetting — they’re able to move through internal approvals faster, reduce last-minute issues, and transact with greater confidence.

Read more: Benchmarking corporate taxpayer participation in tax credits

While sellers are responsible for ensuring project compliance and documentation, buyers face financial risk if the credit is disallowed, recaptured, or adjusted. Without thorough diligence, buyers may overlook issues that later surface during an Internal Revenue Service (IRS) review or audit.

Fortunately, buyers have a range of tools, such as contractual indemnities and tax credit insurance, to help mitigate risk. And they don’t need to navigate this process alone. Legal counsel typically leads much of the diligence work, while partners such as Crux provide further support by underwriting and pricing risk more efficiently.

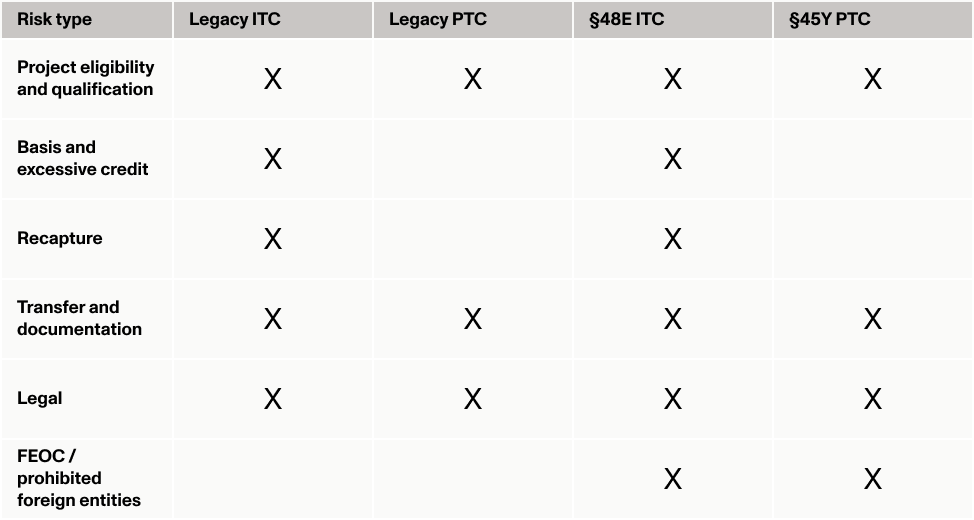

Below are the most common tax credit transaction risks and the strategies buyers use to manage them effectively. Keep in mind that the applicability of these risks can vary depending on credit type and whether a credit falls under the legacy or tech-neutral regime.

Overview of risk types and applicability to credit types

Tax credits are only valid if a project meets strict IRS requirements:

The IRS can disallow credits that do not meet these qualifications. Sellers typically provide representations and warranties to prove eligibility, but buyers often request independent verification of eligibility.

ITCs must be valued properly. If the tax basis is overstated, the IRS may reduce the credit amount. This leads to excessive credit transfer risk, where the buyer has purchased more credits than the project actually earned.

If an ITC-generating project is sold or destroyed without being rebuilt within five years of being placed in service, the IRS can "recapture" a portion of the credit. However, this is statistically very rare. Crux research shows that recapture has occurred in just 0.5% of deals. It's also worth noting that, under the ITC recapture schedule, the amount subject to recapture declines by 20% for each full year the project remains in service, fully phasing out after five years.

Even when a project is fully qualified, the buyer can still lose the benefit of the credit if the seller doesn’t execute the transfer in full compliance with IRS requirements.

The validity of a tax credit transfer depends on the seller’s clear ownership of the underlying energy property and their legal ability to transfer the credit. Ownership disputes or hidden liens can impact the validity of a credit transfer.

The One Big Beautiful Bill (OBBBA), passed in July 2025, introduced FEOC requirements that apply to tech-neutral credits (§48E and §45Y). Projects claiming these active credits are subject to three key FEOC requirements:

Understanding risk is only part of the equation. The most successful buyers also manage diligence efficiently by working closely with legal counsel and specialized advisors, using proven frameworks to guide each transaction. That way buyer teams can stay informed and assist in setting strategy and end goals without getting bogged down in every detail.

Top-performing teams consistently:

Rather than reinventing the wheel for every transaction, leading buyers utilize standardized workflows that help internal teams align quickly. For example, using market standard transfer agreements (like those available on Crux) helps parties align on risk mitigation terms without protracted negotiations.

Top-performing buyers proactively negotiate indemnities that clearly allocate responsibility for recapture, basis disputes, or disallowed credits. In turn, tax credit insurance has become a staple of the market. It enables buyers to transfer over specific risks and move quickly on promising opportunities.

Read more: A Guide to the Tax Credit Insurance Market

The most successful teams begin diligence early. Early alignment between buyer and seller regarding documentation quality, prevailing wage and apprenticeship (PWA) compliance, and cost substantiation creates shared expectations and minimizes review cycles.

Buyers are not expected to be engineers. Confidence in the transferable credit market requires traceability, but the heavy lifting of technical verification can be delegated to specialized advisors.

With full-service, end-to-end transaction guidance, Crux helps buyers move from diligence to closing with ease.

Buyers on Crux benefit from a curated selection of pre-vetted credits from top-tier developers and manufacturers, along with expert guidance from a team that brings vast experience across finance, tax, and project development. We work closely with leading legal and insurance partners to help ensure that every transaction is properly structured and de-risked.

Using deep market knowledge paired with standardized documentation, industry-specific diligence workflows, and data-backed insights drawn from more than $55 billion in credit transactions, Crux equips buyers and their advisors with the tools to assess and close deals efficiently and with minimal risk.

Learn more about how Crux can support your approach to the tax credit market.