Buying transferable tax credits does not meaningfully increase a company’s risk of Internal Revenue Service (IRS) audit. New research from Crux shows that 90% of surveyed buyers report no IRS contact on their transferable tax credit positions — of those that did, no respondent reported a full disallowance of the credit.

___

As the transferable tax credit market has scaled, companies want to ensure they understand the risks that come with purchasing tax credits — including whether buying tax credits could expose them to an IRS audit.

With multiple filing seasons complete, the market is getting a clearer signal of how the IRS is engaging with tax credit transactions. The overall picture is encouraging. Audits have been very rare, and buyer protections are commonplace. Early IRS attention on §6418, the section of the Internal Revenue Code that authorizes the transfer of clean energy tax credits, has focused on addressing fraud, not auditing legitimate transactions.

Tax credit buyers who understand how the IRS approaches the market — how it selects returns, what it examines, and what a well-prepared buyer looks like — are well-positioned to transact with confidence.This post covers the key details buyers and investors should know to transact with confidence.

Download the executive summary: Managing tax credit loss and audit risk

Key takeaways:

For §6418 transactions, the IRS's early monitoring infrastructure was built primarily to detect fraud, not examine well-structured, legitimate tax credit transfers. According to subject-matter experts interviewed during the development of Crux’s recent whitepaper on audit and recapture risk, the IRS had not finalized filters for systematic audit selection of these transactions as of early 2025. Staffing reductions have further slowed that development.

Near-term attention is likely to focus on:

Buyers should expect the examination environment to evolve as the IRS builds more experience and scales its audit-flagging tools.

Crux’s research revealed two common areas of IRS scrutiny in transferable tax credit transactions: property valuation and eligible basis calculation, and base credit-rate compliance.

For investment tax credits (ITCs), the tax credit value is calculated as a percentage of the project’s eligible basis, making the methodology used to establish fair market value at placed-in-service an examination target. When the IRS does engage on this issue, it tends to focus on the credibility of the basis step-up and whether it is supported by a clear, documented rationale.

Buyers and investors should ensure their valuation methodology is well-organized, defensible, and grounded in factors such as third-party appraisals, construction costs, integration complexity, or buyer expertise.

A second common focus area is base credit rate compliance — specifically, whether the project satisfied the conditions required to claim the credit rate it reported. For projects above one megawatt that do not qualify for an applicable exemption, failure to meet PWA requirements significantly reduces the applicable credit rate. Treasury has explicitly flagged PWA enforcement as a priority, and the IRS introduced Form 7220 in 2025 to standardize PWA reporting — a development that also gives examiners cleaner, more structured data to review.

When an examination begins, the IRS starts from what it already has: the seller's pre-filing registration, the buyer's Form 3800, and information reports that allow it to compare what the seller reported transferring against what the buyer claimed. The buyer's documentation burden is real, but it begins from a baseline the IRS has already established. A well-organized diligence file serves two functions in this context — it provides substantive support for the credit position itself, and it establishes the record of reasonable care that matters if the IRS challenges the position.

Crux's buyer survey found that 90% of respondents reported no IRS contact on their transferable tax credit positions. Of those who did receive contact, three received formal audit notices, only one of which was specifically focused on the tax credit transfer agreement. Two of the three resolved with no reported credit disallowance; one settled on undisclosed terms. No respondent reported a full disallowance of transferred tax credits.

When an examination does occur, the buyer holds statutory liability and typically controls the proceeding. In 84% of observed deals, the buyer controls the conduct of the examination, while the seller is required to cooperate and provide documentation. In approximately 81% of observed deals, the seller retains consent rights over buyer-initiated settlements.

That structure works well when parties are aligned — and, in most examinations, they will be. The dynamic becomes more complicated at the moment a settlement decision needs to be made, particularly when an insurance policy is also in place. The buyer, the seller, and the insurer may each have their own rights and interests at that stage. The tax credit transfer agreement and the insurance policy govern how those rights and interests interact.

Buyers should understand those dynamics before they arise, not after. The legal provisions governing audit governance — who controls the proceeding, when settlement is permissible, what opinion standards apply — are worth reviewing carefully at the time of negotiation.

The buyers best positioned to navigate an IRS examination are those who treat audit preparedness as part of the transaction itself. Tax credit buyers and investors should consider these tips to stay audit-ready:

The diligence file is the IRS's starting point in any examination. Pre-filing registration documentation, Form 3800, basis support, PWA records, and independent engineering reports all serve double duty — they substantiate the credit position on the merits, and they demonstrate reasonable care in a way that matters if the credit is challenged. Buyers who treat documentation as a checklist at execution and then set it aside are not getting the full value of what they assembled.

“Prepare your documents as if an audit begins tomorrow.” – Pilar Puerto, Partner, Dinsmore & Shohl

The recapture window is the period during which an investment tax credit can be recaptured by the IRS if the underlying property ceases to be used for its qualifying purpose. Buyers, investors, and their advisors benefit from maintaining an active line of communication with sellers throughout that window — requesting periodic compliance certifications that confirm continued qualified use, operational status, and the absence of any ownership changes.

In Crux's deal terms data, 93% of observed deals include a notice-of-potential-recapture-event covenant requiring the seller to proactively notify the buyer of any triggering event. A subset of deals (approximately 15–20%) go further, requiring the seller to deliver annual certifications of compliance, not just notice only when a problem arises.

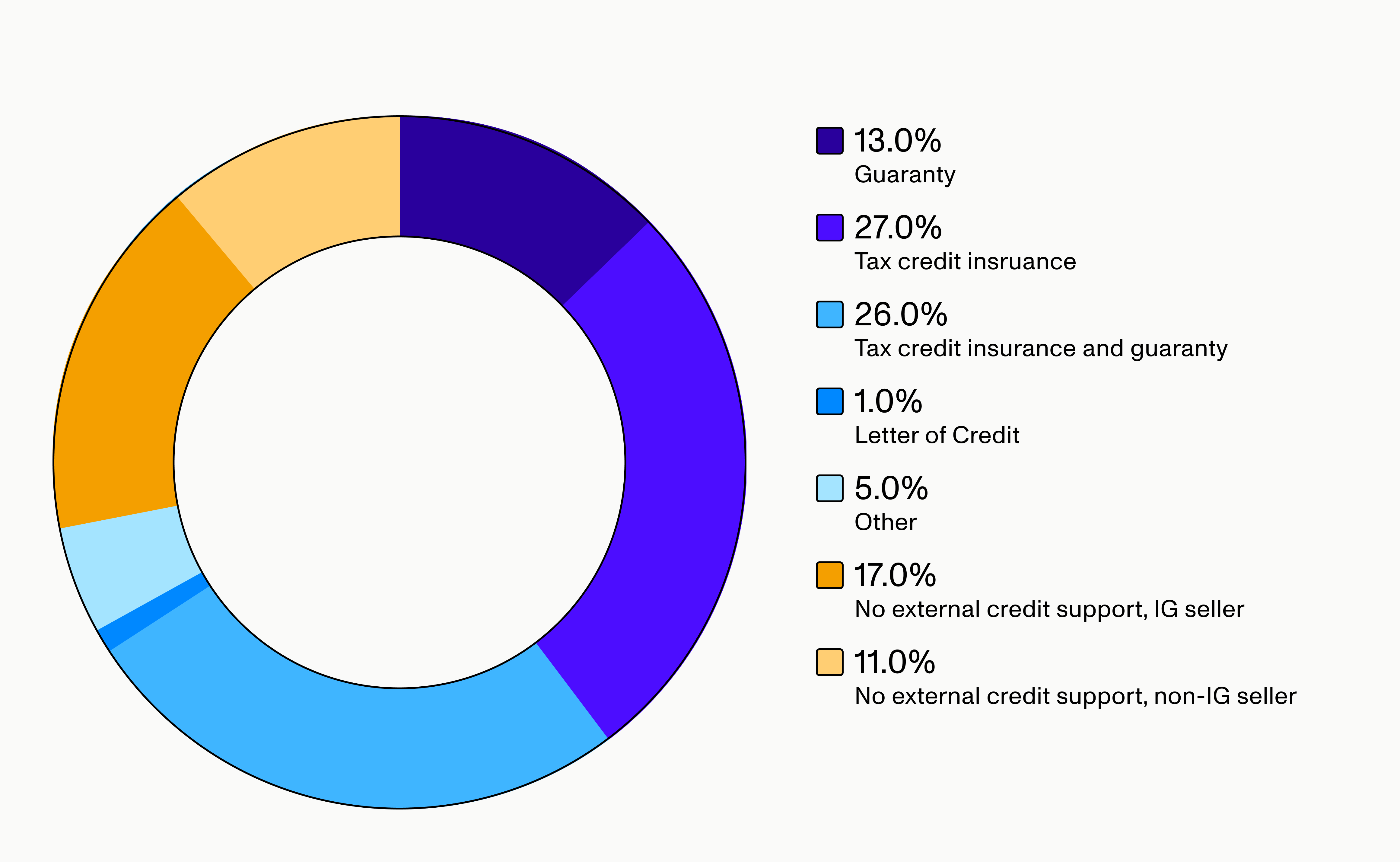

In 89% of observed deals, some form of credit support is in place — through tax credit insurance, a seller guaranty, or a well-capitalized seller signing the transfer agreement directly. That prevalence reflects a market that has developed meaningful buyer protections in a short time.

Breakdown of external credit support

What varies significantly is how that coverage is structured. The interaction between a tax credit insurance policy and the indemnity provisions in the transfer agreement — coverage amounts, policy terms, which scenarios each instrument addresses — affects what a buyer actually recovers in a loss scenario. A 100% indemnity cap and an insurance policy in place do not automatically produce full economic recovery if the two instruments are not coordinated. Treating credit support as a substantive item in negotiation is worth the attention.

For buyers involved in large or complex transactions, proactive IRS engagement tools — including pre-filing agreements (PFAs), which provide binding pre-filing certainty for up to five years — can be beneficial. A PFA functions as a targeted review of specific issues the buyer designates, conducted before the return is filed. The user fee is approximately $181,500, which may be cost-effective relative to a contested examination for a large transaction.

The IRS is still building its approach to §6418 transactions — audit selection methodology is not finalized, and staffing constraints have slowed that development. That will change as the IRS develops subject-matter expertise, finalizes selection methodology, and scales its AI-assisted audit-flagging tools.

Buyers who treat audit preparedness as part of the transaction itself — maintaining a well-organized diligence file, staying engaged with the seller through the recapture window, and understanding the governance provisions in their transfer agreement — are well-positioned regardless of how the examination environment evolves.

For a closer look at how audit and recapture risk is managed in practice, check out the executive summary of Crux’s research. The full whitepaper, which includes deal terms data on indemnity caps, contest provisions, survival periods, and credit support, is available exclusively to Crux clients.

Dive deeper into eligible basis risk in transferable tax credit transactions.

Understand recapture periods for ITCs and how to mitigate recapture risk.

Find answers to your questions about purchasing tax credits in our guide for tax credit buyers.