By Stephanie Deterding, Managing Director, Tax Investor Coverage at Crux

Crux recently published its 2025 Market Intelligence Report. It serves as a comprehensive look at the state of clean energy project finance, covering pricing, deal flow, lending trends, tax equity, and the transferable tax credit market in granular detail.

It's a resource I'd encourage every tax and finance team to read in full, but I want to highlight a few insights that matter most for corporate tax credit buyers heading into 2026. Here is what stood out to me:

Key takeaways:

The transferable tax credit market was tested in 2025. The passage of the One Big Beautiful Bill (OBBB) in July reduced corporate tax liabilities by an estimated 20–30% and introduced regulatory uncertainty around credit disqualification resulting from prohibited foreign entity (PFE) designation. Consequently, many buyers chose to pause and recalibrate their appetite for tax credits.

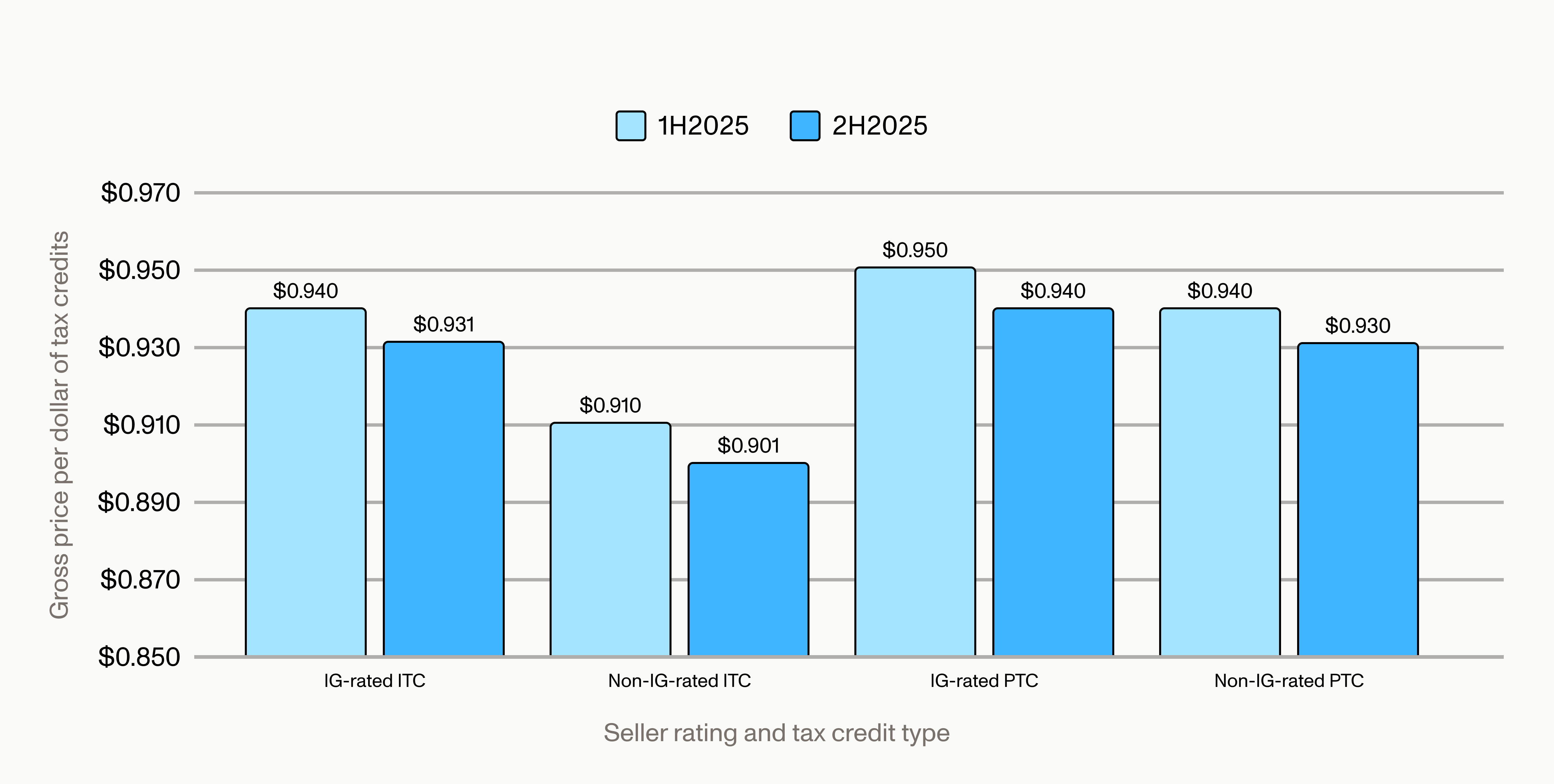

As a result of this softening demand, pricing shifted. Average prices for investment tax credits (ITCs) from investment-grade sellers dropped from $0.940 in the first half of the year to $0.931 in the second half, and production tax credits (PTCs) from investment-grade sellers dipped from $0.950 to $0.940.

Investment-grade versus non-investment-grade ITC and PTC pricing

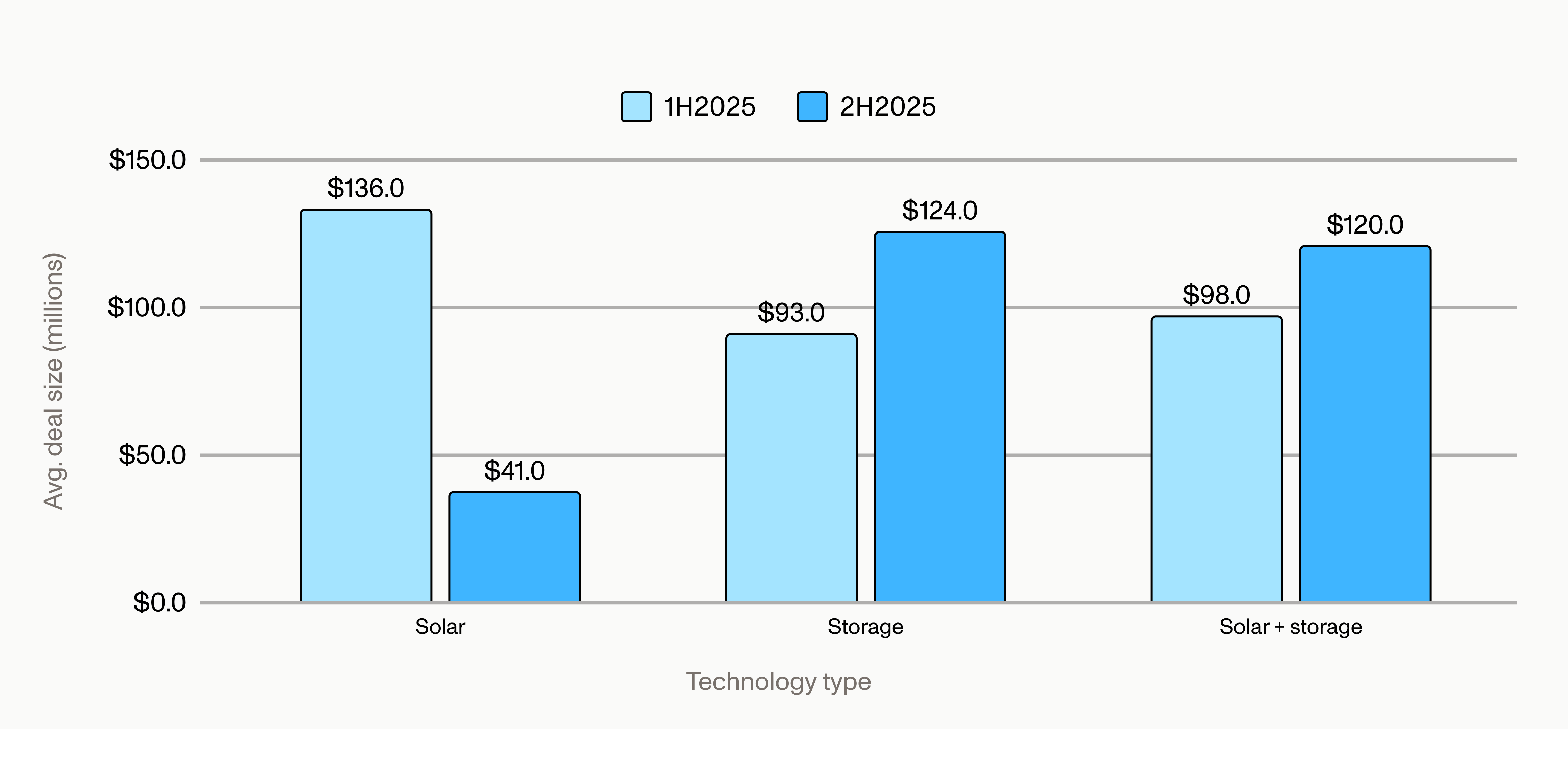

First-half volume exceeded the second half by nearly 1.5x. This slowdown was driven by a decrease in deal size — deal count remained stable across both halves of the year, but average deal size declined substantially as parties deferred larger transactions into 2026. Transactions with notional values between $25 and $100 million emerged as the most liquid and dynamic segment in the second half.

Average deal size, by half year, 2025

Despite these headwinds, the market remained resilient and continued to expand. Total annual tax credit monetization across tax equity, preferred equity, and transfers grew to $63 billion. The transferable tax credit market alone grew from $32 billion in 2024 to $42 billion in 2025 — a 48% year-over-year increase.

Buyers broadened their tax buying strategies amid uncertainty around 2025 tax liabilities — nearly half of tax credits purchased in 2025 were for other tax years, including nearly $9 billion in long-term PTC strips. Buyers also expanded the technologies they purchased — §45Z clean fuels credits, which entered the market in 2025, accounted for nearly 6.8% of total market volume in the second of half of 2025 and roughly $825 million in transactions across the full year. This adaptability served buyers well in 2025 and will be even more important in 2026 as competition for available credits intensifies.

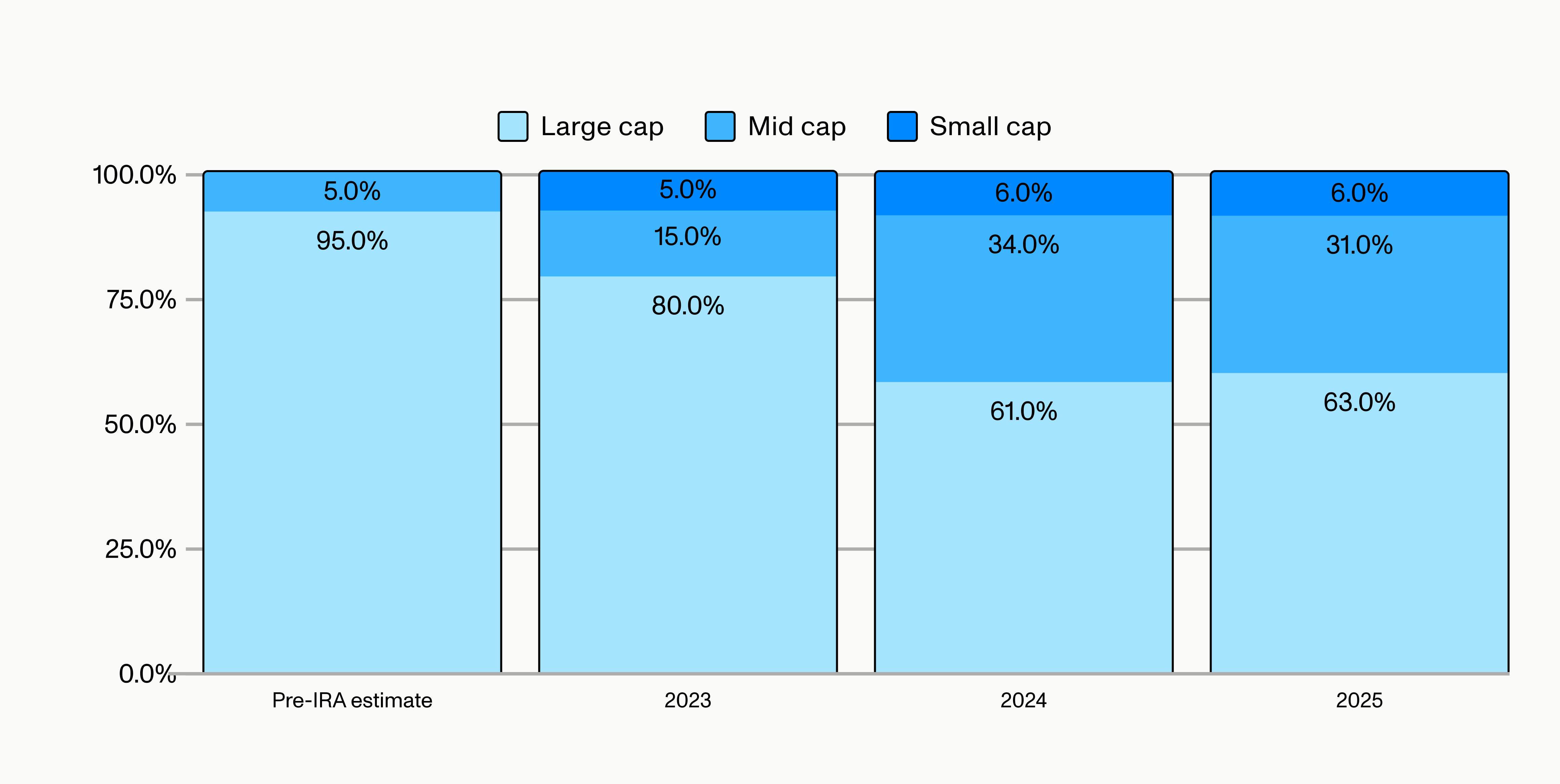

Buyer participation in the transferable tax credit market broadened substantially in 2025. Crux estimates that approximately 243 Fortune 1000 companies — nearly one-quarter of the index — were active tax credit investors through Q3 2025, representing a nearly 60% year-over-year increase from 2024.

While large-cap companies saw the greatest year-over-year increase in participation (up 12 percentage points to 30%), mid-cap (24%) and small-cap (15%) corporates were not far behind. Crux will be publishing full-year 2025 participation data in the coming weeks, and we expect these numbers will grow further.

This shift underscores one of the central structural impacts of transferability: lower barriers to entry enable transactions that meet the needs of multiple market capitalization tax profiles.

Active companies in the tax credit market by size, year over year

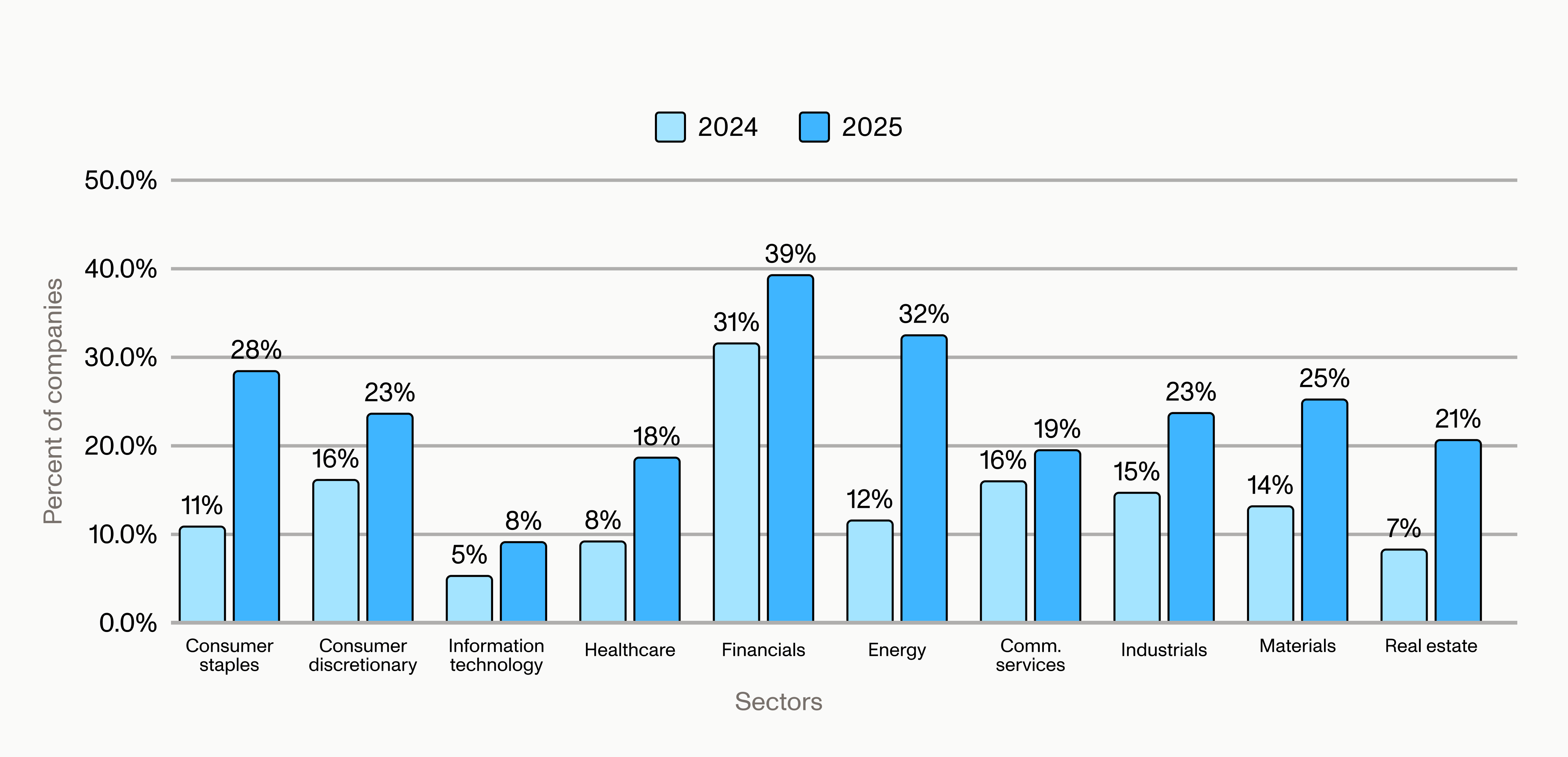

Across industries, financials and energy companies continue to lead participation — 39% and 32% of Fortune 1000 companies within those sectors participate, respectively. But consumer staples, industrials, materials, healthcare, and real estate saw notable year-over-year growth, underscoring that transferable tax credits are emerging as a mainstream tax-planning tool, not a niche financial strategy for specific industries.

Percentage of F1000 companies active in the tax credit market by sector, year over year

The economics justify the effort: buyers reported effective tax rates approximately three percentage points lower than comparable non-buyers in 2025, translating to roughly $11–12 million in annual cash savings for a company with $100 million in federal income tax liability.

Early indicators suggest a more confident and competitive market heading into 2026 as tax credit buyers digest the effects of the One Big Beautiful Bill. Crux's survey data shows that 60% of buyers had clarity on their 2025 tax liabilities by year-end, and another 25% expect that clarity by the end of Q1 2026. Market activity for prior-year credits is picking up materially as corporate tax teams finalize their positions and re-engage.

As buyers return, two important dynamics are shaping the year ahead for 2025 tax credits:

First, some prospective buyers have substantial unmet 2025 demand. While smaller buyers were proportionately more active in later 2025, larger corporates are increasingly active following the recent release of corporate alternative minimum tax (CAMT) guidance and are looking to take down larger tranches of 2025 credits. Some of these buyers are preserving their risk-mitigating preferences, such as seeking PTCs, and may be hoping for the lower pricing that characterized the second half of 2025. In many cases, however, the price and availability of remaining 2025 credits may not correspond to those preferences.

Second, tax credit sellers have premium price expectations for their 2025 credits. Many of the credits that transacted in the second half of 2025 — especially those that moved at lower prices — did so because the seller had near-term liquidity requirements. Sellers that didn't need the liquidity waited. Now, these well-capitalized sellers are coming to market with higher price expectations. Crux forecasts a rebound in tax credit pricing for 2025-vintage credits, especially for solar ITCs and §45X advanced manufacturing credits, possibly reaching or exceeding first-half 2025 pricing levels.

This recovery in pricing would be driven by competition among buyers, particularly for the finite pool of remaining 2025 tax credits. Crux estimates that $8–10 billion in 2025-vintage tax credits remained available at the end of the year, spanning multiple tax credit categories:

Beyond the remaining 2025-vintage supply, 2026 is shaping up to be a significant year for new credit generation. Crux forecasts total tax credit monetization of $64.0–69.5 billion in 2026, up from $63.0 billion in 2025. Capital investment in clean energy is expected to rise 7.5% year over year to $125 billion in Crux's base case projection, with a high case exceeding $150 billion. Energy storage installations alone are on track to double, rising to 88.6 GW of installed capacity from 43.3 GW at the end of 2025.

That growing supply will meet a structurally larger buyer base. Crux expects mid-cap and smaller buyers — who participated in the market in force in 2025 — to remain active, with repeat participation and portfolio-style purchasing increasingly common. This, coupled with an expected increase in large-cap buyers returning to the market as a result of greater visibility into their tax liability, may create a more crowded buyer environment.

The data points to a clear conclusion: corporate taxpayers shouldn’t wait to engage the market. Even though 2025-vintage credits remain available today, the sellers holding those credits are expecting premium prices, and buyer competition is increasing. Additionally, because buyers typically want as few transactions as possible to offset their liability, large-ticket-size deals will be especially competitive.

Locking in relationships now positions buyers to secure favorable terms before the market tightens. At Crux, this is exactly the kind of environment our team is built for. We provide buyers with the expert advisory and professional services to connect them with the right credits to meet their tax -planning needs, the market insights to evaluate them, and the execution support to move efficiently through the transaction and beyond.

Contact us to learn more about how Crux can support your tax investment strategy.