Insurance is an essential tool for mitigating risk in tax credit transactions. As the tax credit market has evolved and matured, so too has the use of tax credit insurance to address transaction risk.

Crux explored trends in tax credit insurance in The State of Clean Energy Finance: 2025 Mid-Year Market Intelligence Report, including pricing and insurance use across different clean energy technology types.

Go deeper: Download A Guide to the Tax Credit Insurance Market

Tax credit insurance protects the buyers of transferable tax credits from potential financial losses if the Internal Revenue Service (IRS) challenges, reduces, or disallows the credit. Policy terms vary, but insurance generally covers the buyer for any financial losses resulting from both disallowed and reduced credits as well as penalties, interest, and legal defense costs. Insurance is typically procured and paid for by the tax credit seller to make a deal more attractive.

Crux’s research found that insurance costs were higher in the first half of 2025. Carrier-quoted premiums that were $150,000–350,000 per policy in 2024 ranged to $450,000 or more in 1H2025. Underwriting premiums also rose, with fees that ranged from $50,000–90,000 in 2024 trending closer to $100,000 and up in 1H2025. Higher premiums drive up the cost of insurance as a percentage of a transferable tax credit deal, which is especially consequential for smaller deals (less than $10 million) where insurance costs are a larger percentage of the deal’s total value.

As the insurance market tightened, insurers capped coverage for single policies at or around $800 million, limiting coverage availability for ultra-large tax credit deals. Standards for step-up coverage also tightened. Insurers generally imposed retentions for step-up values in excess of 25%.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

The first half of 2025 saw buyers in the tax credit transfer market willing to reward deals that mitigate counterparty risk. Crux observed that deals from investment-grade sellers and deals that included insurance coverage commanded about a $0.03 pricing premium over other deals. Investment-grade (IG) deals — those from sellers with a sufficiently robust balance sheet to provide an indemnity without insurance — saw higher absolute pricing than deals with insurance as buyers demonstrated a flight to the most credit-worthy counterparties.

If a seller is not investment grade, insurance can lower the perceived risk of the transaction, making it more attractive to buyers.

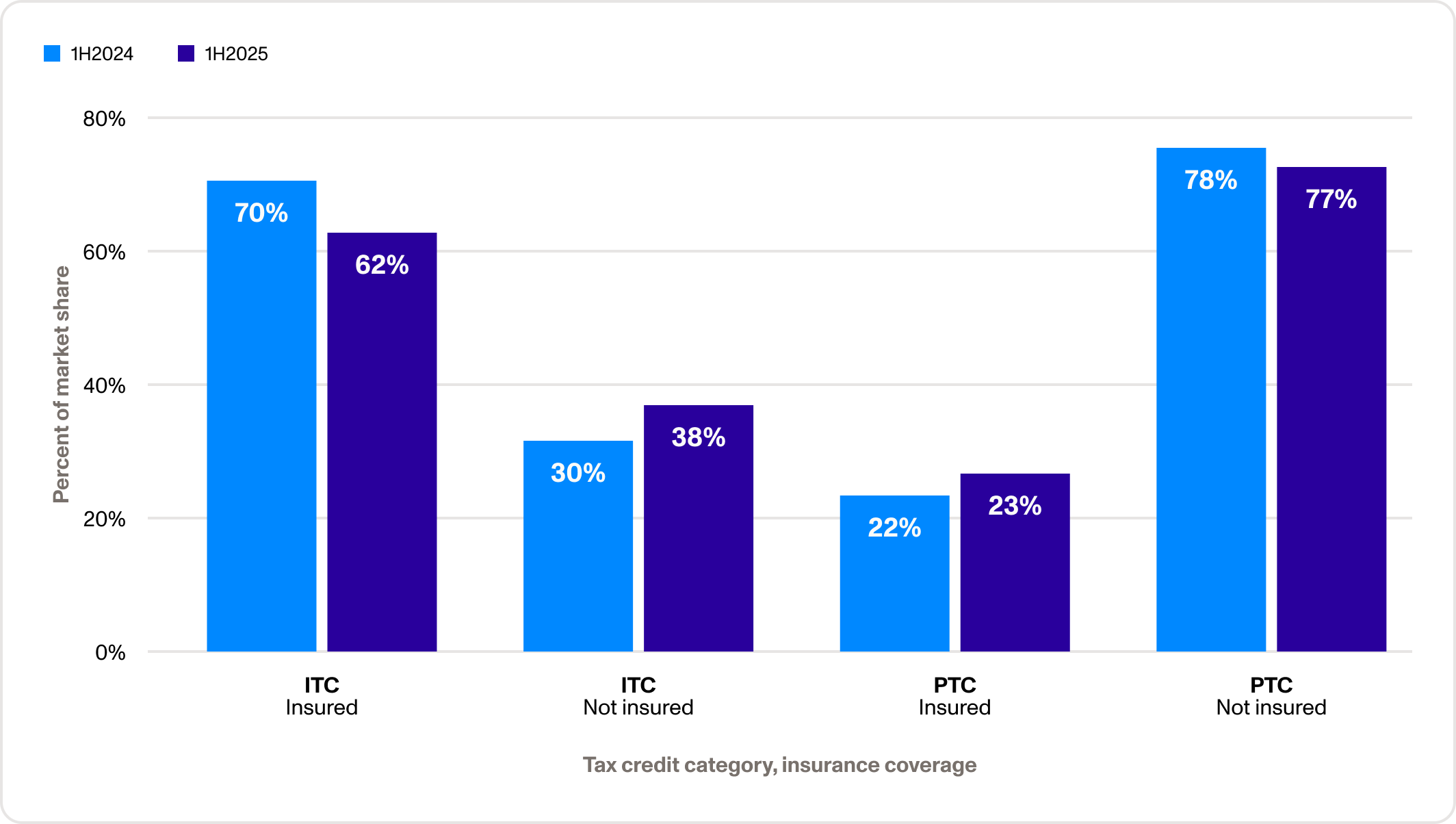

In aggregate, the prevalence of insurance coverage actually declined slightly from the first half of 2024 — 62% of investment tax credit (ITC) deals included insurance coverage, versus 70% in 1H2024. Prevalence rose very slightly for production tax credits (PTCs), from 22% in 1H2024 to 23% in 1H2025.

Share of insured and uninsured and seller-indemnified deals, 1H2025 and 1H2024

Insurance coverage is less common for PTC deals because PTCs are only generated when a project is producing electricity or a component has already been manufactured. PTCs cannot be recaptured by the IRS. No wind projects generating PTCs included tax credit insurance.

On the ITC side, insurance coverage varied widely across credit types.

Insurance prevalence declined substantially for large, utility-scale, investment-grade solar deals. Crux’s data showed that 25.5% of utility-scale solar deals in 1H2025 were insured, versus 40.0% in 1H2024, reflecting the ability of IG sellers to offer parent company indemnities.

On the other hand, the share of residential solar deals with insurance rose; 91% of residential solar ITC deals included insurance in 1H2025, compared to about 75% in 1H2024. Insurance was seen as increasingly necessary to de-risk deals given the elevated uncertainty around the residential solar market.

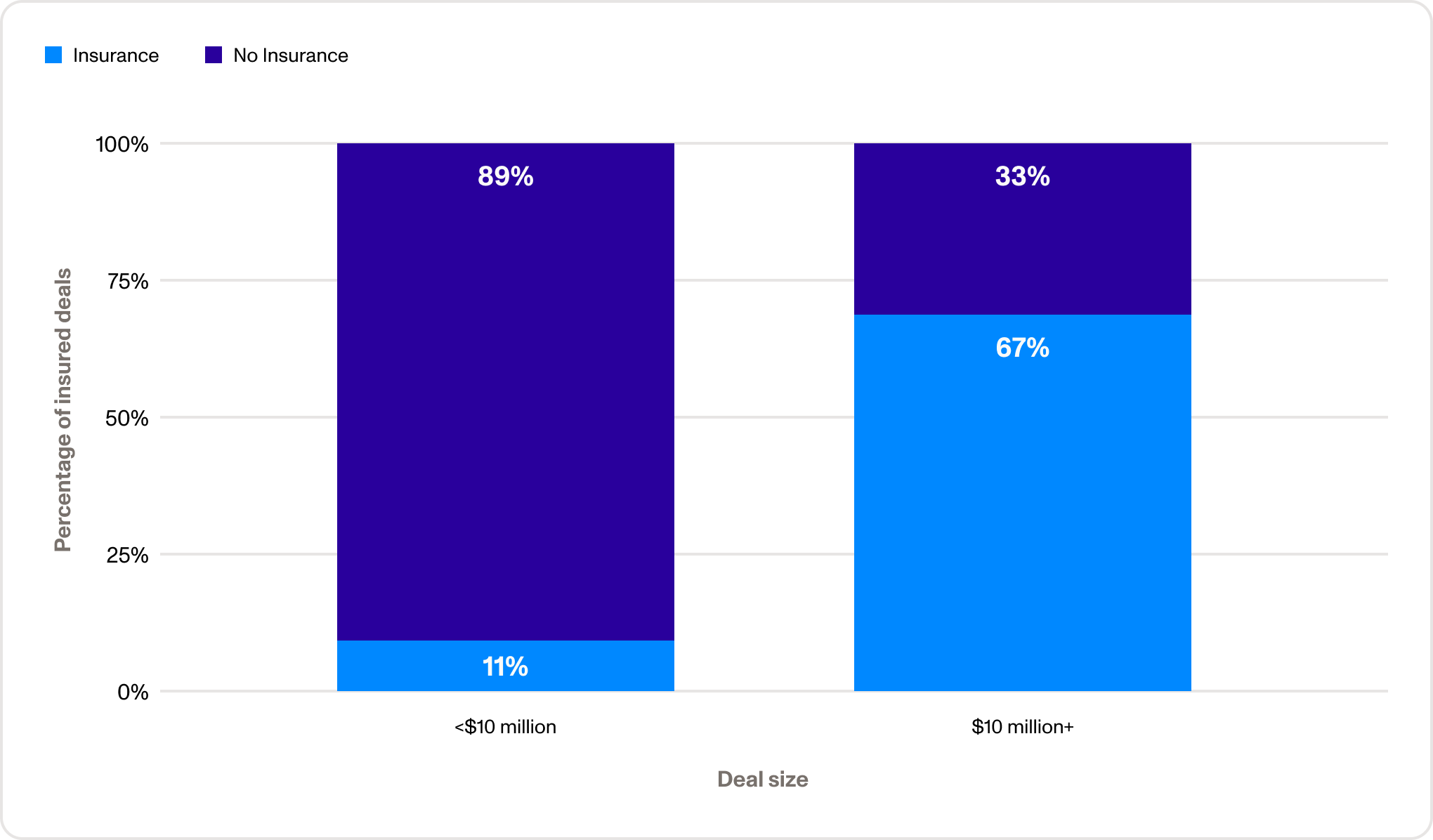

While 25% of community / commercial and industrial (C&I) deals reported insurance, prevalence varied by deal size. Only 11% of deals under $10 million had insurance — the result of the high cost of insurance as a percentage of the total deal cost and a lack of policy availability for this deal size. Because insurance was more economical and available the larger the deal size, 67% of deals $10 million and over had insurance.

Prevalence of insurance for C&I / community solar ITCs

Insurance is an important tool to de-risk battery and energy storage and solar + storage projects. Crux found that 80% of reported storage deals in 1H2025 used insurance, including 50% of deals with investment-grade sponsors. A larger share of storage projects have merchant revenue models, so insurance serves as a critical de-risking mechanism and supports market liquidity for these deals.

Insurance can be an important tool to increase buyer comfort with tax credits from newer tax credit categories. New §45Z clean fuel PTCs began to enter the market in the first half of 2025, for instance, and typically included insurance coverage.

The prevalence of insurance coverage in §45X advanced manufacturing deals has fallen as buyers grow more comfortable with the tax credit category. The incidence of coverage for these deals stabilized at around 40% of deals in 1H2025.

Prevalence of insurance for advanced manufacturing PTC deals, by deal count

Section 45U nuclear PTCs are an exception to this trend; nuclear PTCs typically do not have insurance and price at the higher end of the market because nuclear is seen as low risk. Plants are operated by profitable companies with strong balance sheets and predictable production.

Insurance coverage is an essential tool to create a more liquid market for tax credits from non-IG sponsors or emerging technologies. Crux works closely with leading insurance brokers and law firms to understand how the tax credit insurance market is evolving and set new market standards for diligence in tax credit transactions. Read more about insurance standards — including a sample insurance policy walkthrough — in A Guide to the Tax Credit Insurance Market: Version 1.0.