Tax equity bridge loans (TEBLs) are one of the most important financing tools available to clean energy project developers. They let projects fund construction before a tax equity investor's capital contribution arrives — and they sit inside a bridge lending market that, according to Crux's 2025 Market Intelligence Report, grew 8.9% year over year in 2025, outpacing construction lending and debt financing.

This guide focuses specifically on tax equity bridge loans (TEBLs): their structure, cost, capital providers, and how the One Big Beautiful Bill (OBBB) has changed the landscape.

A TEBL is a short-term, project-level loan that funds construction costs before a tax equity investor's capital contribution. It is repaid when a tax equity investor funds at construction completion milestones.

Tax equity investors generally do not fund until a project reaches mechanical or substantial completion milestones, qualifies for the investment tax credit (ITC) or production tax credit (PTC), and meets the other conditions in the equity capital contribution agreement. Developers, however, need cash much earlier to pay contractors, equipment suppliers, and grid interconnection costs as construction progresses. A TEBL fills that gap by providing funds up front, during construction at or post-NTP.

TEBLs are historically common and used when a project raises traditional tax equity. The loan is repaid by the tax equity investor's capital contribution, and the lender's underwriting focuses on whether that investor will fund as committed.

Tax credit bridge loans emerged with the introduction of tax credit transferability. They're used when a project monetizes its tax credits through transferability rather than tax equity. The loan is repaid from the cash proceeds of a tax credit sale, and the lender's underwriting focuses on the buyer, the sale price, and the project's tax credit qualification.

Get our latest insights and favorite reads on the transferable tax credit market in your inbox.

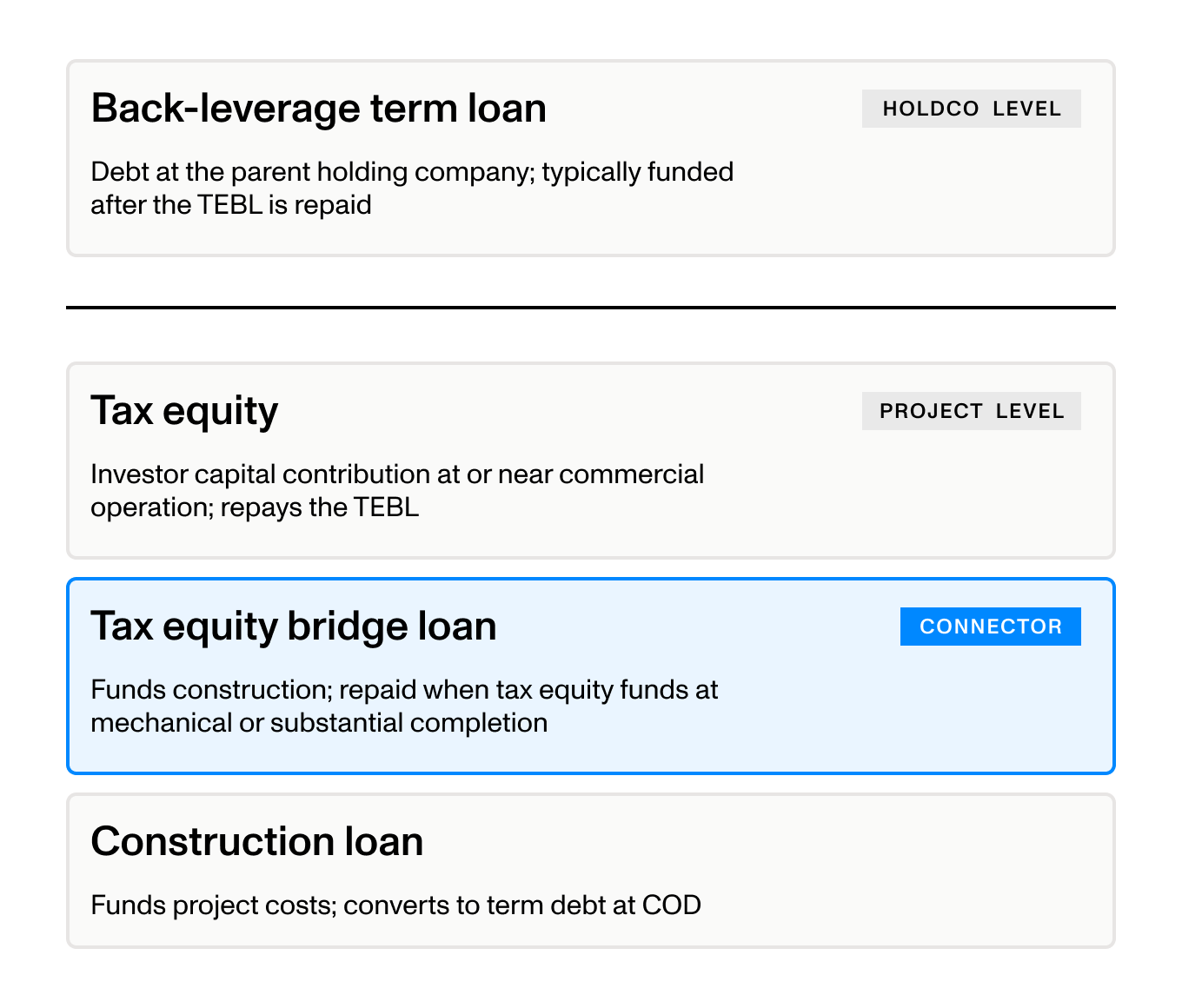

A typical utility-scale project that uses tax equity has four layers of capital active during or shortly after construction:

The TEBL connects all the layers. It funds the project during construction, gets repaid when tax equity funds, and clears the way for back-leverage debt at the holdco level.

The construction loan and TEBL are often documented in the same credit agreement in two parts: the construction piece funds project costs and converts to term debt, while the TEBL is paid off in full when the tax equity investor funds.

At its core, a tax equity bridge loan is a loan against a tax equity investor's commitment to fund. That commitment exists because the investor is paying for the value of the project's tax credits, which is why tax credit qualification is part of the underlying logic of the loan.

TEBLs are short-dated by design — commonly 12 to 24 months, sized to construction with a buffer for the placed-in-service date. The maturity date is fixed: it triggers repayment whether or not tax equity has funded.

On a committed TEBL — where an investment-grade tax equity investor is bound by an executed contribution agreement — pricing has been stable. Crux's 2025 Market Intelligence Report found that pricing for committed structures with high-quality buyers and experienced sellers ranged from 150 to 225 basis points above the SOFR in 2025, with advance rates up to 98%. Pricing within that range depends largely on the credit quality of the tax equity investor: a BBB-rated investor will draw a wider spread than an A- rated investor, since the lender is essentially lending against the investor's credit, not the project's standalone economics.

Uncommitted bridge loans, generally only available to well-established project sponsors, became very limited in 2025. Where available, uncommitted structures typically saw advance rates of around 70–75%, based on assumed tax credit sale prices of approximately $0.90 (an assumed credit price must be implied as there is no tax equity quantum established).

Bridge terms also vary by technology. According to Crux's 2025 Market Intelligence Report, emerging technologies with limited operating histories typically face lower advance rates, wider spreads, and greater lender selectivity than mature solar or wind.

A TEBL is secured by the pledged equity interests in the project company and assignment of the tax equity funding obligation. If the tax equity investor's funding doesn't cover the full bridge balance when it’s due, the sponsor backstops the shortfall (typically through an indemnity); timing gaps from project delay are usually handled through extension mechanics.

Underwriting focuses on three questions: will the project qualify for the tax credits, will the tax equity investor fund as committed, and can the sponsor cover any shortfall?

Tax credit qualification flows directly into the credit agreement: reps and warranties on credit eligibility, covenants to maintain qualification (covering prevailing wage and apprenticeship compliance, domestic content, beginning-of-construction safe harbors, and other applicable requirements), conditions precedent tied to tax counsel's opinion, and, increasingly, tax credit insurance. Following the OBBB, lenders are noticeably more rigorous on prohibited foreign entity (PFE) supply-chain documentation than they were a year ago. Because the loan is sized off expected credit value and timing, any deterioration in qualification flows directly into the lender's recovery.

Lenders look at counterparty diligence on the investor as well as execution diligence on the project, because the investor’s funding is contingent on the project being built. Lenders review the executed tax equity term sheet or capital contribution agreement, diligence the investor’s investment-grade rating and track record as a tax equity participant, and pressure-test the engineering, procurement, and construction (EPC) contract and the construction schedule, because the investor won’t fund until mechanical completion. Know-your-customer (KYC) diligence on the investor or transferee is standard.

If the tax equity investor's funding doesn't cover the full bridge balance at maturity — most often when the project's tax credit qualification falls short or construction costs run over — the sponsor backstops the difference, typically through an indemnity or parent company guarantee. Lenders diligence the sponsor's balance sheet, liquidity, and other project commitments to confirm the backstop is more than a piece of paper.

A TEBL is repaid from the proceeds of the tax equity takeout. The tax equity investor funds at mechanical and substantial completion milestones, near commercial operation under the equity capital contribution agreement, and the TEBL is repaid in full from that funding.

A project's underlying tax equity structure can be traditional (one investor) or hybrid (an investor combined with a tax credit transferee). The structure determines what flows in to fund the takeout, but the takeout itself (and the TEBL's repayment) works the same way in both cases.

The TEBL market is dominated by large commercial and investment banks with established tax equity practices. Active arrangers include MUFG, KeyBanc, Wells Fargo, JPMorgan, Bank of America, and Santander, alongside other major commercial and investment banks active in clean energy project finance. Specialty platforms such as Apterra and HASI participate too, and dedicated debt funds like Crayhill Capital Management have entered the market in response to compressed timelines from the OBBB. Private credit funds have also adapted to offer developers unitranche solutions, wrapping TEBLs into construction to term debt.

TEBLs are well-established products, but they have specific risks worth understanding before signing a term sheet.

If the tax equity investor delays funding, the TEBL maturity does not move. Sponsors typically backstop this risk with shortfall indemnities, extension mechanics, and contingent equity.

The recapture period for investment tax credits is five years. If something disqualifying happens in that window, the Internal Revenue Service (IRS) can recapture up to 100% of the tax credit in year one; the recapture amount declines 20% each year after. Foreclosure on a TEBL during that period disqualifies the tax credit. Counsel typically addresses this by structuring the borrower as a special-purpose entity, so a foreclosure doesn't directly affect the asset producing the tax credit. According to Crux's 2025 Market Intelligence Report, lenders also use mitigation tools like tax credit insurance and interparty agreements to manage recapture risk.

Projects that begin construction after December 31, 2025, can be disqualified from claiming tax credits if their supply chain or ownership has ties to a PFE. Lenders are reviewing PFE compliance carefully, and TEBL term sheets increasingly include ongoing PFE representations and covenants.

For more on PFE rules and how they apply to clean energy projects, see our prohibited foreign entity cheat sheet.

To qualify for tax credits under the OBBB, wind and solar projects must be placed in service by December 31, 2027 or begin construction by July 4, 2026 to safe harbor their tax credit eligibility. A TEBL whose takeout depends on tax credit qualification can't survive a missed deadline.

A project planning to add back-leverage debt at the holdco level after the TEBL is repaid needs the two lender groups' rights to be coordinated upfront. Misalignment delays term conversion and traps cash.

For a deeper look at tax credit bridge loans, see Understanding tax credit bridge loans in clean energy capital markets.

To go deeper on the tax equity market that ultimately takes out a TEBL, download our 2025 tax equity market factsheet.

For Crux's broader view on the 2026 debt capital markets, see our roundtable with Crux's lending experts.